A dispatch from the number crunchers – Yield curve rolldown

Since Keith So joined us earlier this year as a quantitative analyst, I’ve been throwing all manner of questions at him and his python notebooks. The most recent was; “Is there an optimum place to invest on the yield curve to maximise the benefits of rolldown?”

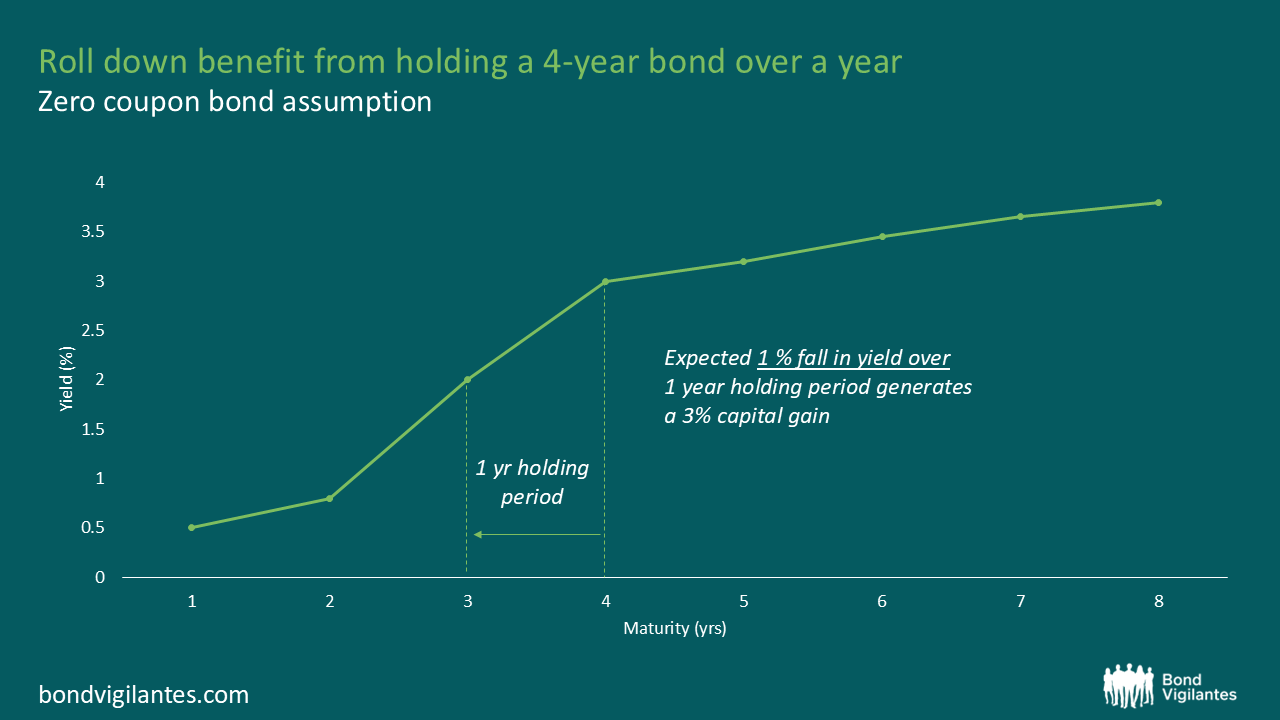

Rolldown is the capital gain an investor captures as a bond’s maturity shortens and it moves to a lower-yielding point on the yield curve. Clearly this assumes an upwardly sloping yield curve, and the steeper the curve, the more rolldown one captures.

Graphic used for illustrative purposes only and it is not based on a particular security

To investigate this Keith pulled in over 20 years of government bond data, sliced it into maturity buckets, and analysed which buckets produced the greatest returns from rolldown over those 20 years.

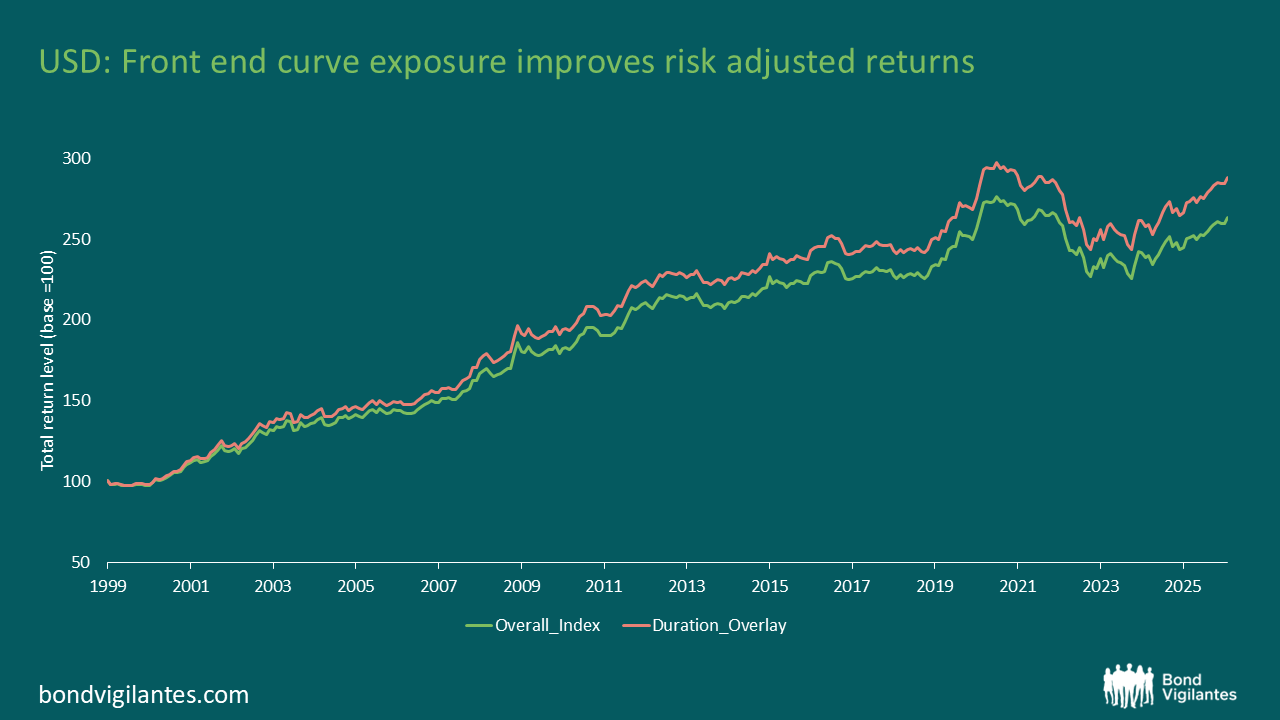

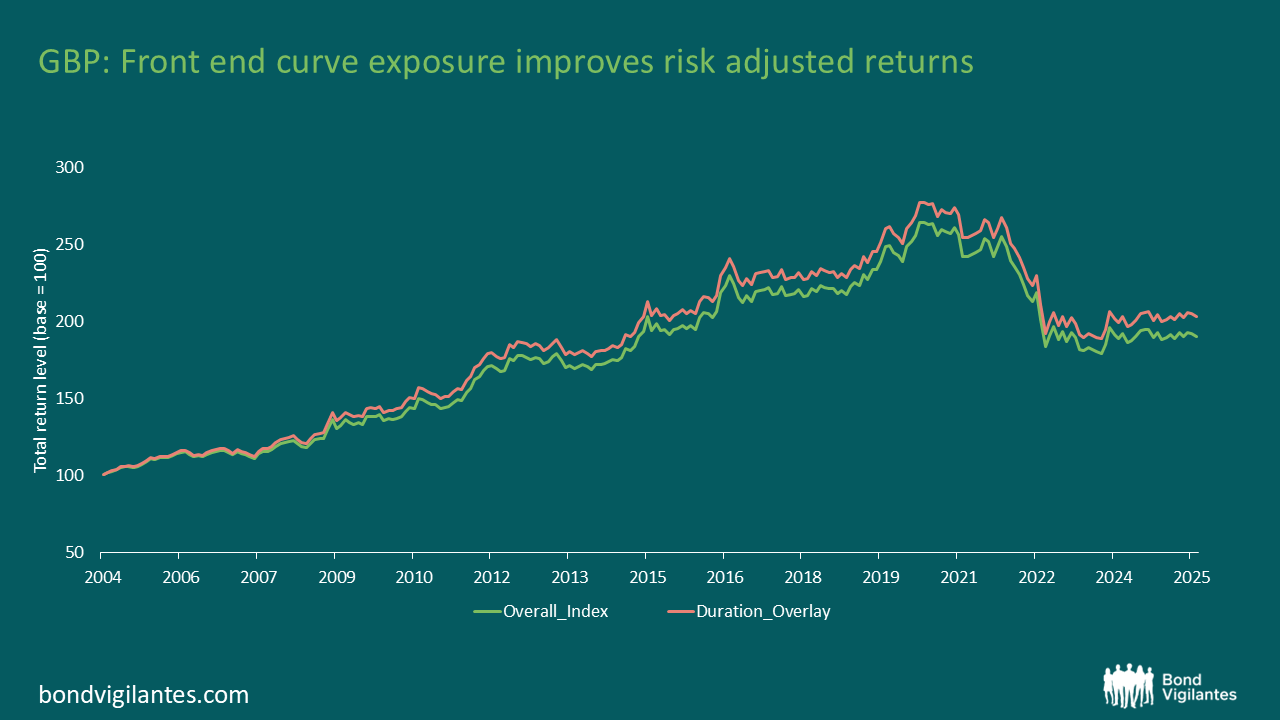

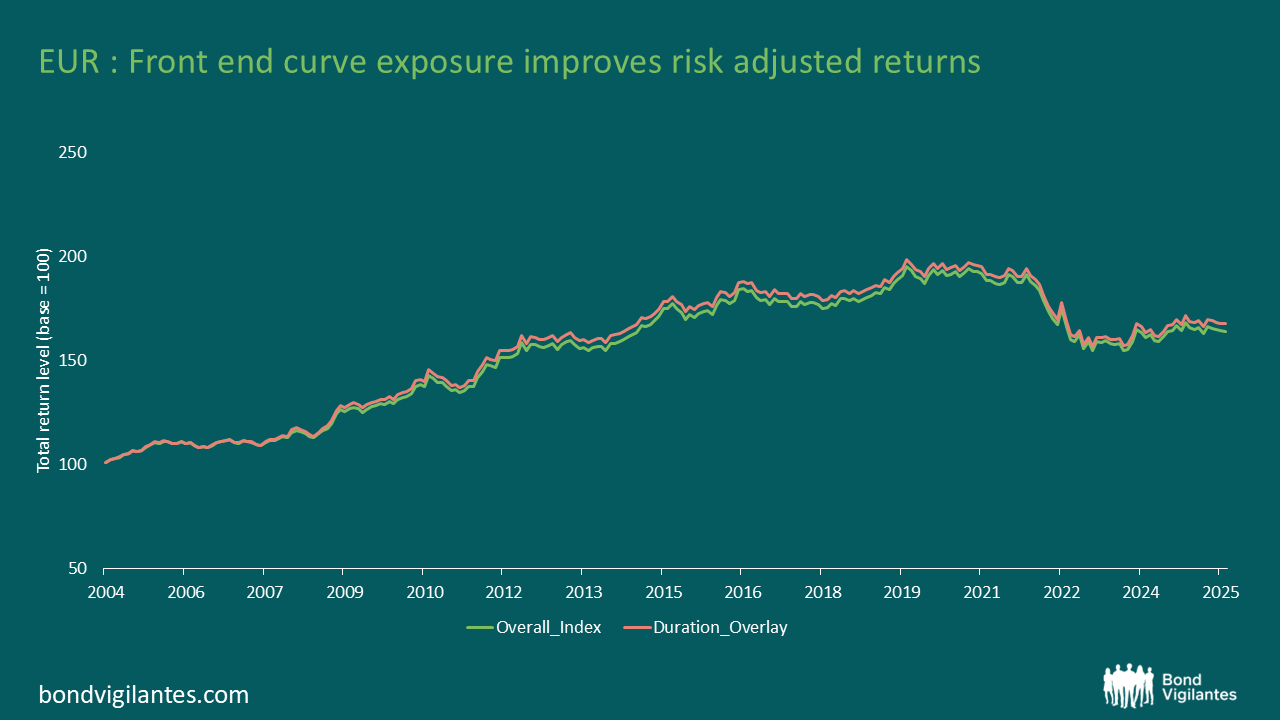

The best performing bucket in Gilts and Treasuries was the 3-4yr, while in Bunds the 4-5yr bucket performed best. Whilst these short end buckets may have benefited from the greatest rolldown, in a secular falling yield environment, they (unsurprisingly) delivered lower total returns than the broader index and their longer-dated peers, due to being shorter duration. So far so unsurprising, but when we looked at the risk adjusted returns, things start to look more interesting. As you can see in the table summarising the results, once the volatility of returns is considered, the short-dated buckets show their value to an investor. The historic Sharpe Ratios (the return per unit of volatility) of the lower duration buckets is meaningfully higher than the competition.

Source: Bloomberg, March 2026

So how can we, as bond investors, exploit these results?

Most obviously (especially coming from a short-dated corporate bond fund manager), we can buy more front end bonds to improve the risk-return characteristics of our portfolio. However, this would reduce the duration of our wider portfolio and leave us at risk of underperforming if yields were to fall over the next 20 years too.

What if we overweight the short-dated bucket and underweight the longer bucket, whilst maintaining a neutral duration across the portfolio? Well, that more or less matches (if not beats) the performance of the overall index and reduces the volatility meaningfully.

Source: M&G, Bloomberg, March 2026

Source: M&G, Bloomberg, March 2026

Source: M&G, Bloomberg, March 2026

The strength of outperformance clearly varies across £, € and $s, but in all cases having an overweight to the front end/steepest part of the yield curve generates better risk adjusted returns. Rolldown can contribute meaningfully to a bond investors performance, and harvesting this can assist in beating passive exposure to fixed income markets.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.