The Hawk That Cannot Fly

Kevin Warsh walked into his first Fed meeting needing to prove something. The result was predictably hawkish. Rates held steady for the fourth consecutive meeting, but the signal was anything but neutral. Nine policymakers flagged support for higher rates this year, a dramatic shift from March, when not a single member pencilled in a hike.

Markets bought the hawkish turn, with front-end rates moving higher, bringing about a stronger dollar. I’m less convinced it translates into actual rate hikes.

Warsh was appointed by a president who has spent years demanding rate cuts; he needed to signal and shout independence and price stability from the get-go.

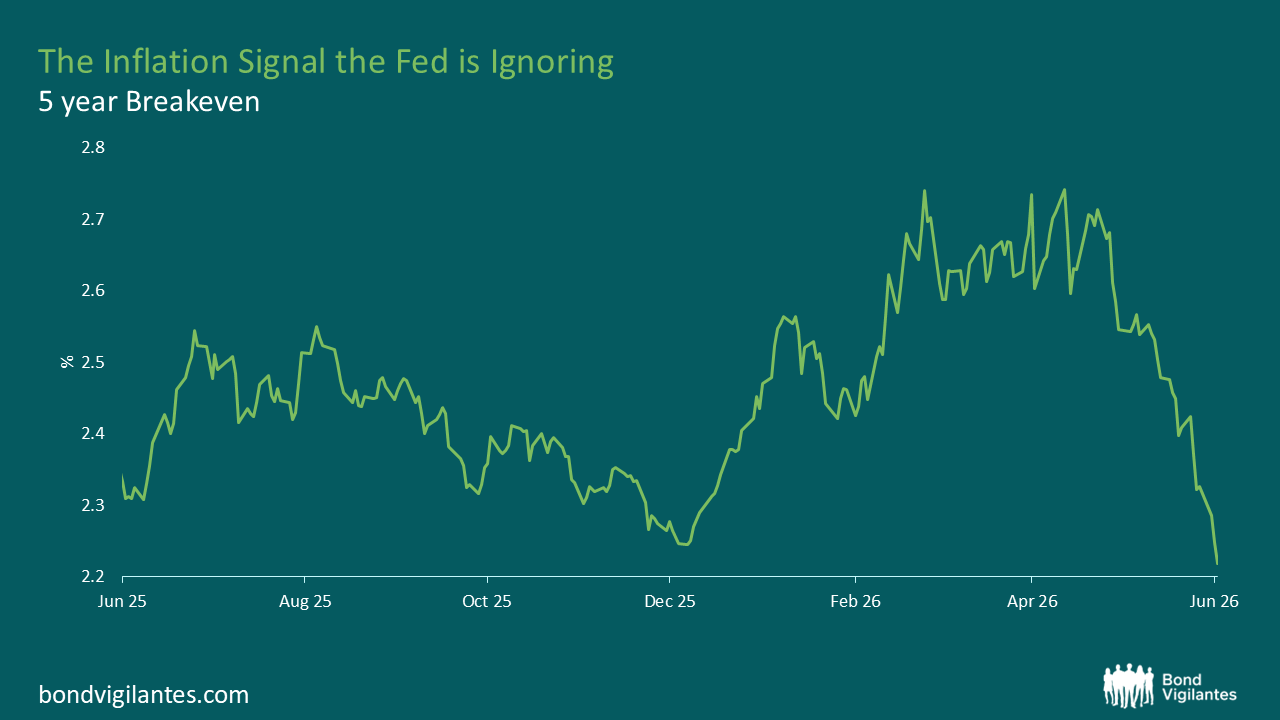

The inflation market is telling a different story

Here’s what’s odd about the hawkish pivot: the inflation market isn’t buying it. More importantly, it isn’t pricing the inflation that would justify it.

5-year breakevens have repriced meaningfully lower since the FOMC meeting, coinciding with a ‘potential’ resolution in the Middle East. They are now at levels that simply don’t signal an inflation problem. More striking still, they’re trading below where they were when the Iran conflict began, the very supply shock that supposedly justifies the Fed’s hawkish tilt. If the bond market genuinely believed that energy-driven inflation was becoming entrenched and broad-based, breakevens would be elevated and rising. They’re not.

Source: Bloomberg, June 2026

This matters because the Fed’s own framework requires evidence of inflation spreading well beyond the energy sector before hiking becomes appropriate. Officials acknowledged that for rate hikes to be warranted, price pressures would need to spread well beyond the energy market. So far that hasn’t been the case, with core inflation measures rising more modestly. Breakevens at current levels are the market’s verdict, suggesting this is a transitory energy shock, not a wage-price spiral. The dot plot is hawkish; the inflation market is not. One of them is wrong.

The implication is straightforward. If inflation expectations remain anchored at these levels, or fall further as the Iran situation stabilises, the Fed’s justification for hiking quietly evaporates. Warsh can maintain the rhetoric, but without a genuine inflation impulse to point to, the committee will find it very difficult to pull the trigger.

The fiscal arithmetic that makes hiking so hard

Even if inflation did re-accelerate, there’s a deeper reason to doubt a meaningful tightening cycle: the US cannot really afford one.

Deficits are expected to remain at circa 6% for the foreseeable future. Net interest costs are set to exceed $1 trillion annually, alongside a problematic rollover burden – all of which we have discussed at length.

This is fiscal dominance in action. When debt-servicing costs become this sensitive to interest rates, a central bank’s independence becomes conditional rather than absolute. Higher rates compound the deficit, which demands more issuance, which pushes yields higher. The feedback loop doesn’t need political interference to operate – it’s just arithmetic. An administration with no appetite for fiscal restraint heading into midterms isn’t going to break the cycle.

What this means for positioning

The front-end, particularly in real yields, has aggressively priced a hiking cycle that neither the inflation market nor fiscal reality supports. That makes real rates at close to 2% look genuinely attractive, as you’re being paid for a tightening scenario that probably won’t fully materialise – with breakevens already telling you inflation isn’t the problem the Fed is pretending it is.

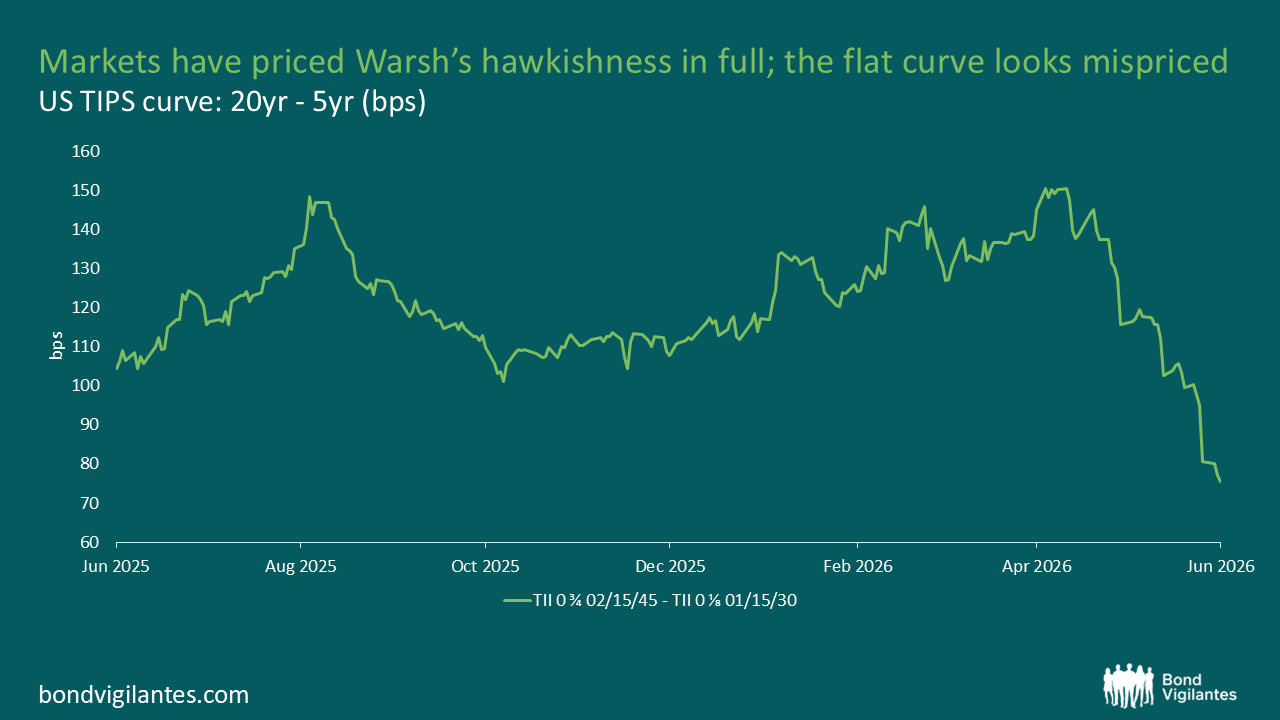

The curve is the other opportunity. The flattening since the FOMC meeting reflects the market pricing Warsh’s rhetoric at face value. But it ignores the structural problem at the long end: a deficit expected to reach nearly 7% of GDP, with risks skewed higher rather than lower.

Source : Bloomberg June 2026.

The steepener thesis is simple: either the Fed doesn’t hike, in which case the front-end rallies, or it does hike, compounding the fiscal trajectory and eventually forcing the long end to reprice on term premium grounds. Either way, the current flat curve looks wrong.

The breakeven market is quietly telling you the inflation emergency isn’t real. The fiscal numbers are quietly telling you term premium should be higher. Warsh’s hawkishness is loud and useful for credibility. But credibility and rate hikes are not the same thing, and right now, the market is pricing them as if they were.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.