The Bond Vigilantes World Cup Model – Knockouts

Following on from the original blog.

1 July

With games coming thick and fast, another three teams going through, another three going home. France really do look unstoppable, whilst Mexico keep doing what needs to be done. Popcorn out for the latest episode of Haaland vs Gabriel at the weekend.

For today, we have commentary on two teams yet to be covered: Belgium vs Senegal.

All predicted scores and model results can be found on the summary slide at the bottom of the blog.

For Belgium, we have commentary from Anjulie Rusius, Macro Fixed Income Fund Manager

Birthplace of nostalgic relics Tintin and the Smurfs – can the Belgians bring home the metal, or will they be leaving the stadia feeling blue?

With Belgium finishing 3rd at the last World Cup – relegating England to 4th place in the third-spot playoff! – they may well have the sporting muscles to serve alongside their moules frites, but will the country’s squad prove as strong as its beer? Especially since the country’s credit rating has been watered down again this year.

In April, Moody’s lowered the sovereign rating one-notch to A1, while S&P cut its rating a week later to AA-, due to the difficulty Belgium faces with cutting one of the biggest budget deficits in Europe. Though the government is attempting to implement fiscal and structural reforms, rising interest rates, increased defence spending and domestic demographic expenditures, ultimately weigh heavily on the borrower. Despite these fiscal pressures however, the financial rating penalty didn’t bite with international investors, as recent primary issuance has been digested well: Belgium’s new €8 billion 5-year OLO launched in May at mid-swaps +19bps, attracting over €45 billion in orders; a healthy oversubscription.

To complete the rating agency picture, last month Fitch affirmed Belgium’s A+ rating (they’d already downgraded Belgium from AA- in June 2025), largely owing to its diversified economy with high income per capita and its implicit financial and institutional support as a member of the Eurozone.

As such, the key outstanding issues for Belgian bonds are the concerns around fiscal deterioration and any further rating pressure this may bring, but let’s hope their football squad just don’t give a Jean-Claude Van Damme.

Commentary for Senegal, it’s Purvi Harlalka, EM Sovereign Analyst:

Recent (albeit disputed) AFCON champions, Senegal is widely regarded as the strongest African side in the 2026 FIFA World Cup. The team has 20 players from the ‘big five’ European leagues (Premier League, Ligue 1, Bundesliga, La Liga and Serie A) – the joint most of any non-European nation, along with Argentina. But their economic prospects couldn’t be more different than their footballing ones. Indeed, Senegal is one of only two African countries likely to be forced to default on their sovereign debt in 2026. It has long been a low inflation (2% on average for the last 25 years) yet fast growing economy (5.3% on average in the last decade) on the back of an ambitious infrastructure programme, and more recently, the discovery of oil and gas. However, it turns out that Senegalese GDP wasn’t fuelled by investment alone, but also by billions of dollars in undisclosed borrowing! This “hidden debt” took debt ratios from 90% of GDP in 2020 to a whopping 133% of GDP at last count, and only came to light following elections in March 2024, when the new administration and the IMF uncovered major liabilities concealed by the previous government, one that had plenty of time to make mischief during a rule of two dozen years. It was a discovery that changed the country’s economic trajectory abruptly. Not unlike their football team, which refuses to concede a title it was stripped of for its actions off the pitch, powerful factions in the Senegalese political classes are reluctant to submit the nation to a debt restructuring, as this would be a serious blow to national pride. What Senegal desperately needs now is a stellar performance by that stellar line up of the Teranga lions. It would certainly go a long way towards restoring some of that wounded pride.

30 June

The model predictions started the knockout rounds strongly with three of four results correct. The prediction of a 1-1 draw between the Netherlands and Morocco, and the latter proceeding after penalties, came through. Though Paraguay’s win over Germany proved a step too far to predict…

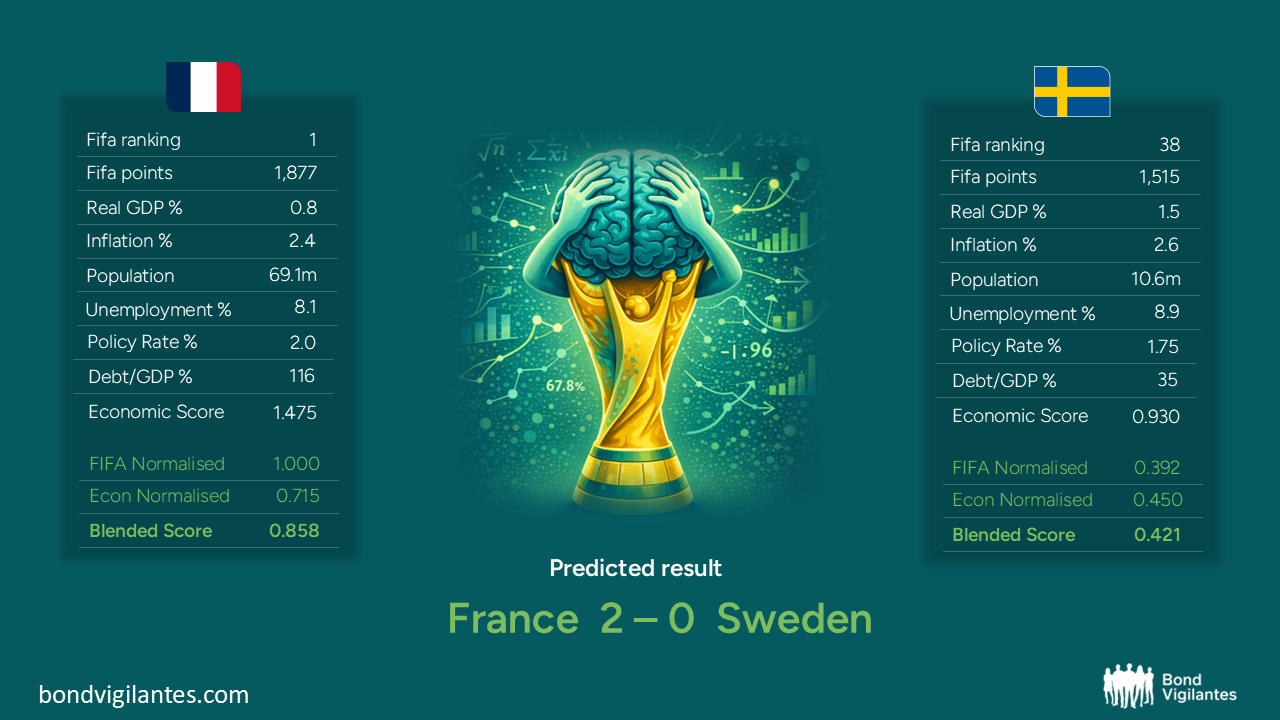

On to today’s games, where we cover both France and Norway.

With commentary on Norway, Rob Burrows, Global Macro Fund Manager:

Norway’s World Cup campaign has got off to a flying start with an impressive 4-1 victory over Iraq and qualification through a difficult group, leaving fans wondering whether this might finally be the tournament where Norway’s footballing pedigree starts to resemble its economic credentials.

When it comes to fiscal management, Norway sits firmly in the global premier league. With its vast oil wealth and sovereign wealth fund measured in the trillions, Norway is the closest thing the world has to fiscal royalty. In footballing terms, they boast two genuine superstars in Erling Haaland and Martin Ødegaard. In economics, they can call upon a sovereign wealth fund so large it might actually own the stadium they are playing in.

While Norway has spent decades dominating the fiscal league tables, its World Cup appearances have been rather more intermittent. Unlike their sovereign wealth fund, Norway’s tournament participation has historically been sparser than a politician’s spending cuts before an election. Expectations are higher this year. With Haaland spearheading the attack and Ødegaard orchestrating from midfield, reaching the knockout stage should be considered the baseline. Priced at around 30/1 going into the tournament, they are likely to be viewed as a dangerous outsider rather than a genuine contender. Norway, the archetypal long-term saver, combining low public debt with a sovereign wealth fund – an advantage that speaks more to economic resilience than footballing odds. The football outcome remains uncertain. But if the tournament were decided by debt sustainability, fiscal prudence and long-term planning, Norway would be lifting the trophy before kick-off.

And again from Rob Burrows, Global Macro Fund Manager, commentary for France:

France headed into this World Cup as one of the clear favourites, and so far there has been no evidence to suggest that those expectations were too optimistic. In fact, its chances of lifting the trophy are generally viewed as much stronger than its chances of delivering meaningful fiscal reform in the short term.

The country’s commitment to fiscal restraint has long been questioned. France has not run a budget surplus for several decades, and public debt continues to trend higher. Attempts to introduce reform have often met with resistance. Pension reform in particular, which is central to improving long term sustainability, has proven politically difficult to implement and has contributed to an ongoing fiscal drift.

These concerns are increasingly visible in markets, where the spread between French and German government bond yields has widened in recent years. Investors appear to be assigning a higher premium to French debt as the fiscal outlook has deteriorated.

At the European level, the reactivation of fiscal rules and the use of excessive deficit procedures point to growing pressure for adjustment, although enforcement has historically been uneven. At the same time, the domestic political backdrop remains uncertain ahead of the 2027 election, adding another layer of complexity to the policy outlook.

Fortunately for French supporters, football tournaments are not decided by debt ratios or fiscal trajectories. Off the pitch, the economic outlook looks somewhat more challenging. But on the pitch, France remains one of the strongest contenders for the trophy, with stars like Mbappe, Dembele, and Olise already shining on the world stage.

29 June

With the group stage complete, it is worthwhile taking stock of how the model has performed, and now we know the tournament bracket, how we expect things to play out from here.

- Outcome accuracy 48 / 72 (66.7%).

- Exact scorelines 8 / 72 (11.1%), which sits in the normal corridor for Poisson-style football forecasters (typically 8% to 14%).

- The model is good at picking clear winners: when it predicts a win, it is right about 69% of the time.

- The clear weak spot is draws. 20 matches finished level, the model only called 11, and only 6 of those came in.

- Goal volumes have so far been systematically under-predicted. Mean predicted total goals per match 2.47 versus actual 2.99, with 49% of matches under-predicted on total goals and only 32% over-predicted. The correlation between predicted and actual total goals is weak at 0.21, so the model is not really pricing how open a game will be.

- But, goal difference is where the model earns its keep with a correlation of 0.67 with actual goal difference. It has predicted relative team strength reasonably well.

Does the model outperform a reasonable benchmark?

A simple approach is to take the FIFA-ranked favourite to win every match, and score it on the same outcome basis as the model. Over the 72 fixtures, that benchmark got 44 results right, or 61.1%. A slightly fairer version allows for draws: whenever the two sides are within eight FIFA places of each other, the benchmark calls a draw; otherwise the higher-ranked team wins. That also landed on 44 out of 72.

To check that approach isn’t bias in the model’s favour, we varied the draw threshold between three and twenty ranking places. The benchmark’s outcome accuracy moves around in a narrow band between roughly 57% and 63%, and never closes the gap to the model’s 66.7%.

That said, with a sample of 72 the confidence interval on outcome accuracy is still wide. So, whilst not being statistically watertight, it at least points in the right direction. It is however probably too early to say that economics can actually predict football outcomes.

We will continue taking you through the round of 32 knock-out stage with commentary on countries we have yet to cover (starting below), along with predictions for every game. Check back each day for the latest.

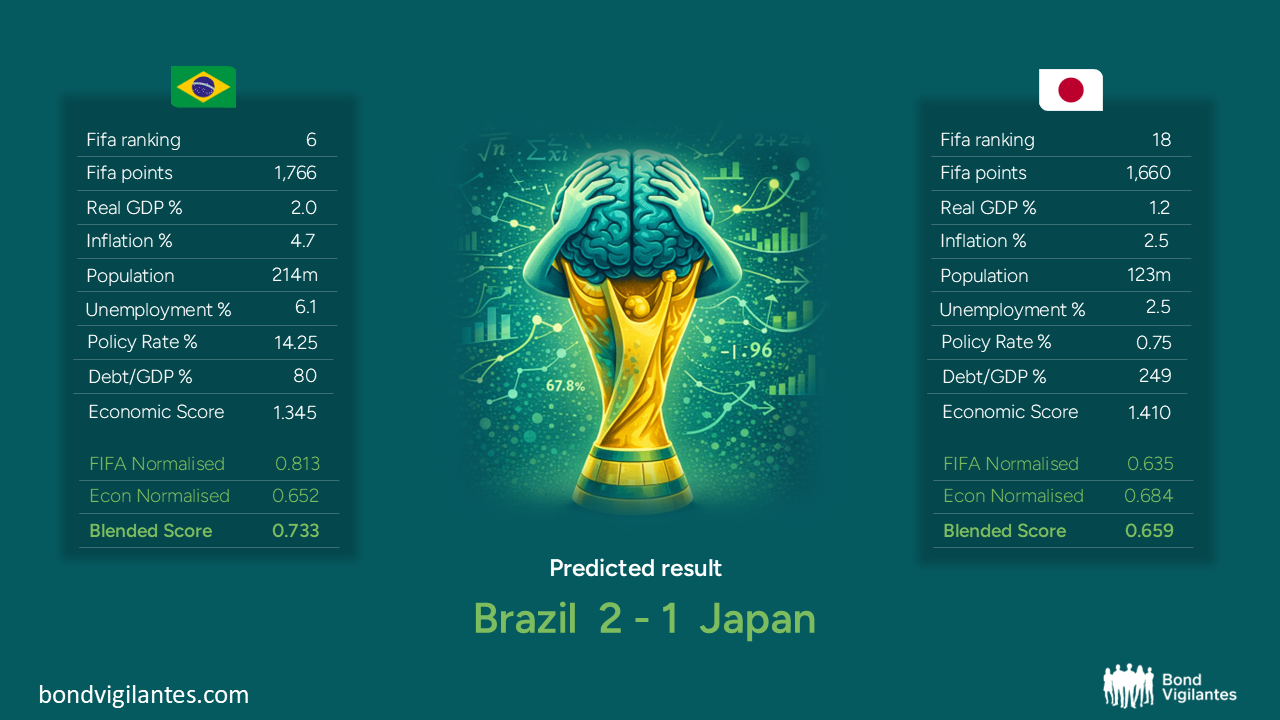

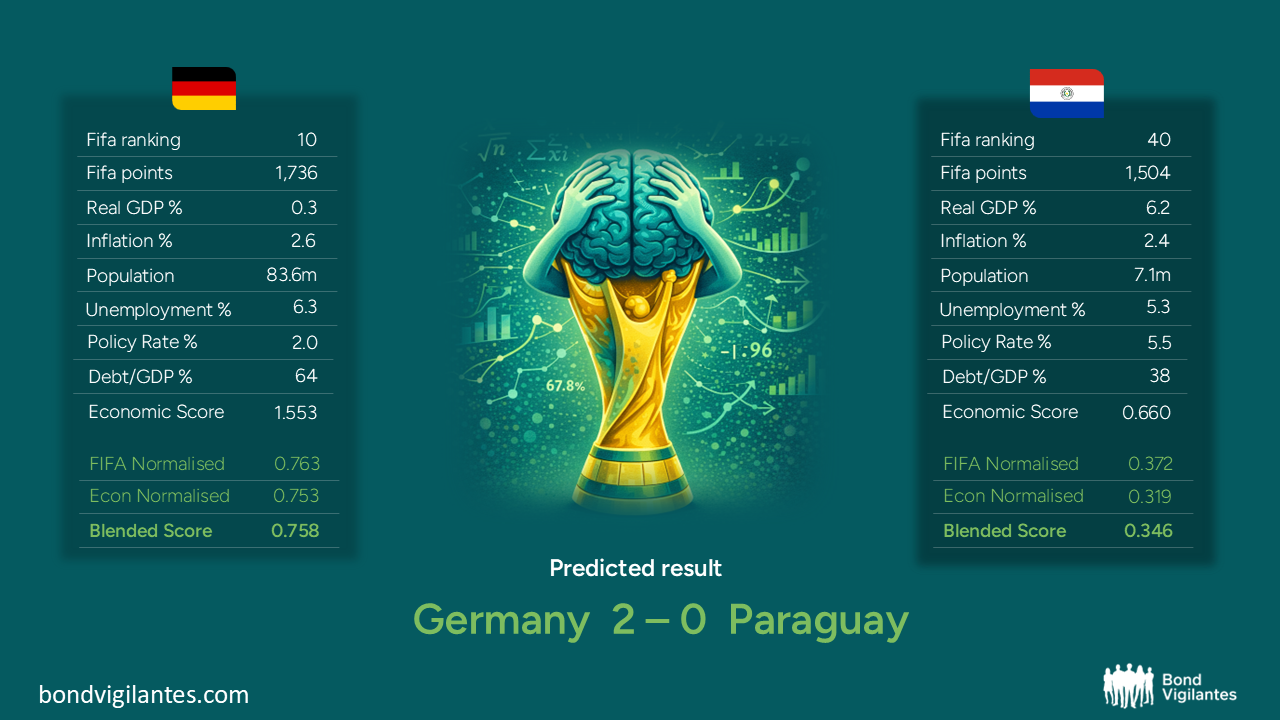

With Canada leaving it late against South Africa last night but ultimately going through (the model predicted 2-0), we proceed through the round of 32 with Brazil vs Japan, Germany vs Paraguay and Netherlands vs Morocco.

With commentary for Brazil, it’s Carlos Carranza, EMD Fund Manager:

Brazil: 5 world cups, 9% real rates. Brazil is the most successful team in the history of the world cup, which is a painful fact to acknowledge when this paragraph is written by an Argentinian. But our Southern Cone neighbours deserve full credit: they have won the world cups 5 times, which is the record. They have been the “only” team that has played every single world cup since 1930 (never failed to qualify), and they have reached 7 finals (winning 5 of them of course).

Yet, the most successful player in their team right now is Mr. Gabriel Galípolo, the Coach of the Central Bank. He certainly rivals Neymar’s talent, keeping real rates at a solid 9.5% (doubling the amount of world cups), which has helped keep the BRL well anchored, while offering strong carry opportunities as financial stability conditions remain well preserved. Fun fact: When the post-COVID inflation hit the global economy, Brazil had hiked almost 1,000bp before the Fed delivered their first hike. Which is indeed a signal of well managed policy making and “jogo bonito”.

Brazil faces 2 key challenges currently: First, while they have elite attackers such as Neymar, or Vinícius Jr., the team has heavy reliance on individual brilliance, and less of a fully cohesive system vs teams (like France). Second, their fiscal deficit is running at a 1% on a primary basis, and close to an 8% overall, which will require significant team-player efforts to reach medium-term debt sustainability.

With commentary for Germany, it’s Rob Burrows, Global Macro Fund Manager:

For decades, Germany has been Europe’s economic ballast: dependable, disciplined, and occasionally accused of making even prosperity seem slightly boring. Its public finances have long been the envy of developed nations, with debt levels that many of its neighbours can only dream of. Yet even Germany has not been immune to economic gravity. A slowing industrial sector, weak productivity growth and geopolitical headwinds have prompted Berlin to loosen the purse strings, with a significant increase in public spending expected over the coming years.

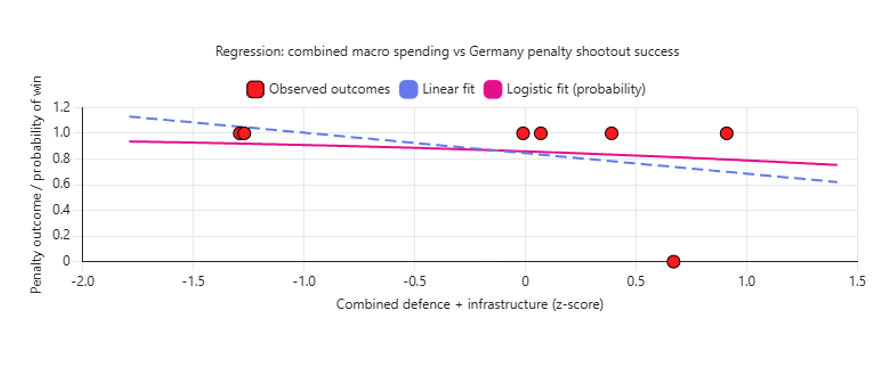

The obvious question for investors is whether fiscal stimulus can revive growth. The less obvious question is whether it can help Germany win the World Cup.

There is, admittedly, little academic literature linking defence expenditure, infrastructure investment and penalty shootout conversion rates but I have tried…

With an R^2 (coefficient of determination) of 0.1 and a negative correlation of 0.45, it’s pretty clear to all that any increased spending does not translate into positive outcomes. Nevertheless, confidence matters. If Germany can rediscover its economic swagger and rediscover the Jurgen Klinsman magic and ruthless efficiency that once made opponents fear every pass and corner kick, they may have a chance.

Sadly, Germany’s greatest predictive asset, boasting an enviable track record, Paul the Octopus, is no longer with us. His absence leaves a genuine analytical void and I am confident his predictions would have looked favourably on Germany and this current cohort of footballers. For what it’s worth, at the outset the less reliable bookies give the Germans a 16/1 chance of lifting silverware.

For now, investors and football fans alike will watch closely. Germany may be embarking on a fiscal expansion not seen in decades. Whether that translates into stronger GDP growth remains uncertain. Whether it translates into lifting the World Cup trophy is even more uncertain.

And again Rob Burrows, Global Macro Fund Manager, with commentary for the Netherlands:

The Netherlands arrive at another World Cup with the familiar label of football’s eternal bridesmaid. Three World Cup finals, three heartbreaks. Always the bridesmaid, never the bride.

The Netherlands is currently undertaking one of the biggest structural changes to its pension system in generations. Trillions of euros of pension assets are gradually moving from a defined-benefit style framework towards arrangements where outcomes are more directly linked to market performance. For bond investors, this isn’t merely an administrative exercise. Pension funds have long been among Europe’s most influential buyers of government bonds and interest-rate hedges. As portfolios adjust, the ripples are being felt across sovereign debt markets, yield curves and swap markets.

However, despite this structural change the Dutch football team’s presence at the world cup feels a lot more like the Netherland’s place in the Eurozone. Solid, reliable, balanced and unlikely to ruffle many feathers. Debt sits comfortably in the mid 40% of GDP range and have kept their heads down within a troubled currency bloc.

The team’s strong defensive capabilities anchored by Virgil van Dijk are as solid as the countries fiscal position but ultimately the team might lack what it takes to go all the way. That said, they are not to be written off as they will likely be in the conversation of the latter rounds.

I’m sure Dutch hopes are riding just as high as the atmosphere in an Amsterdam coffee shop.

Summary of all knockout game predictions (updated 1 July)

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.