Emerging market debt: notes from my recent trip to the IMF Annual Meetings

Last week I attended the IMF’s Annual Meetings in Washington D.C, where I had a series of very interesting meetings with government officials and other world financial leaders. The underlying theme behind most of the discussions was that emerging market countries continue their adjustment into a new phase characterized by less abundant liquidity and lower commodity prices. This adjustment process has thus far held a reasonably steady course, as the asset class has posted respectable returns year to date, part of that driven by lower US yields and part driven by the tightening of spreads and carry. Currencies, which is one of the main channels of adjustment to this new environment have been depreciating, which is something I had highlighted earlier in the year.

Looking into 2015, concerns are shifting from US rates into more specific EM factors. A slowdown of growth in China and other countries was the main concern voiced through the meetings. This reflects an uneven global recovery, where the US is unable to fully offset the growth drag coming from the Eurozone and Japan. Additionally, geopolitical events and country specific structural issues have also contributed to the slowdown.

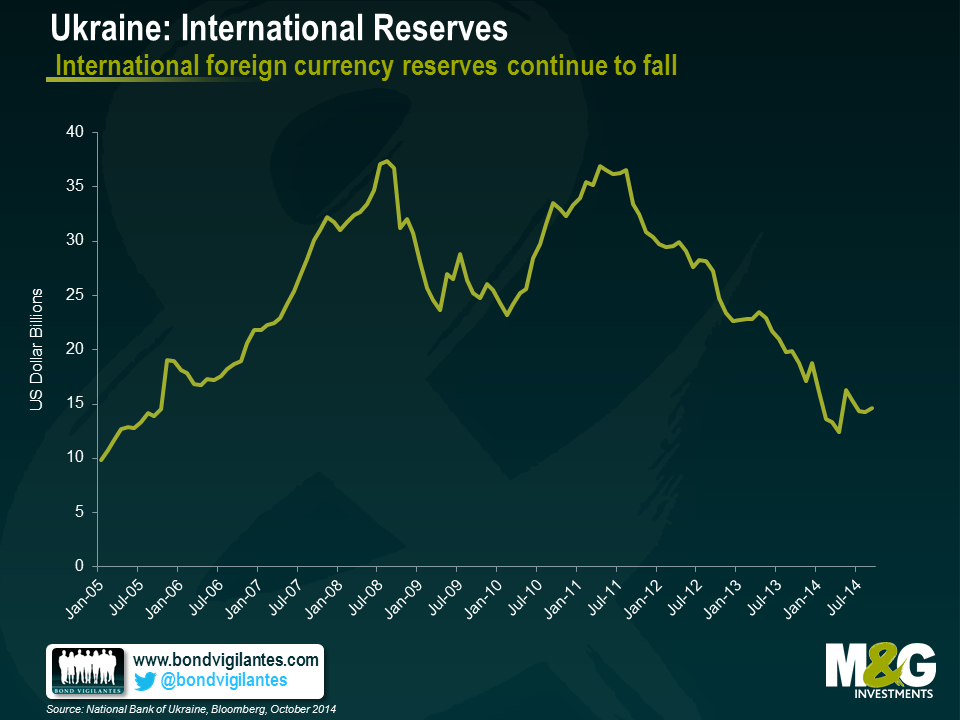

In Ukraine, expectations of a restructuring through a voluntary maturity extension seems widely expected, despite the supportive rhetoric coming from IMF officials, suggesting that additional funding may be provided given the higher financing required as a result of the country’s worse than expected conflict. Despite the supportive rhetoric, I remain cautious on the credit at these levels, with the view that there can be contagion arising from defaults of state owned banks in the years ahead as they will have access to Hryvnia liquidity from the Central Bank, but no preferential access to USD given Ukraine’s weak international reserve position.

Venezuela’s default expectations seem lower than implied by market prices. I believe the disconnect reflects the uncertain recovery value on the credit compared to prior emerging market restructurings. The amount and seniority of additional claims, such as dollar claims by importers, airlines, compensations for past nationalization of assets by the state and state arrears make the recovery exercise a difficult one.

Argentina will face a difficult year ahead given its stagflation and declining reserves, though it has a slight advantage versus the two other distressed credits in the sense that a new administration is likely to pursue more orthodox economic policies than the current administration. Still, the country’s legal dispute with the holdouts will extend well into next year and there is also the risk that a bond acceleration on the Defaulted Par bonds makes this situation even more complex.

Brazil’s upcoming second round elections on October 26 will be critical. Foreigners are more sceptical that the pro-market Aecio Neves could win. I see the elections a little less binary than the markets. Aecio’s ability to push reforms through Congress can disappoint, given Brazil’s fragmented party structure. At these levels, however, I see more upside in asset prices and particularly local rates should he win, than I see downside should Dilma be re-elected.

As for Russia, its ability to maintain its investment grade rating largely depends on how long with the conflict with Ukraine will last. Relations with the West, particularly with the US have hit bottom and are at the lowest point since the Cold War. US authorities remain quite relaxed in terms of maintaining their sanctions for a very long time if needed. I remain cautious on the credit, but believe that spreads already reflect the deterioration in capital flows, international reserves and the recent decline in oil prices. Credit risk between the sovereign and select state champions such as Gazprom or the larger state owned banks should continue.

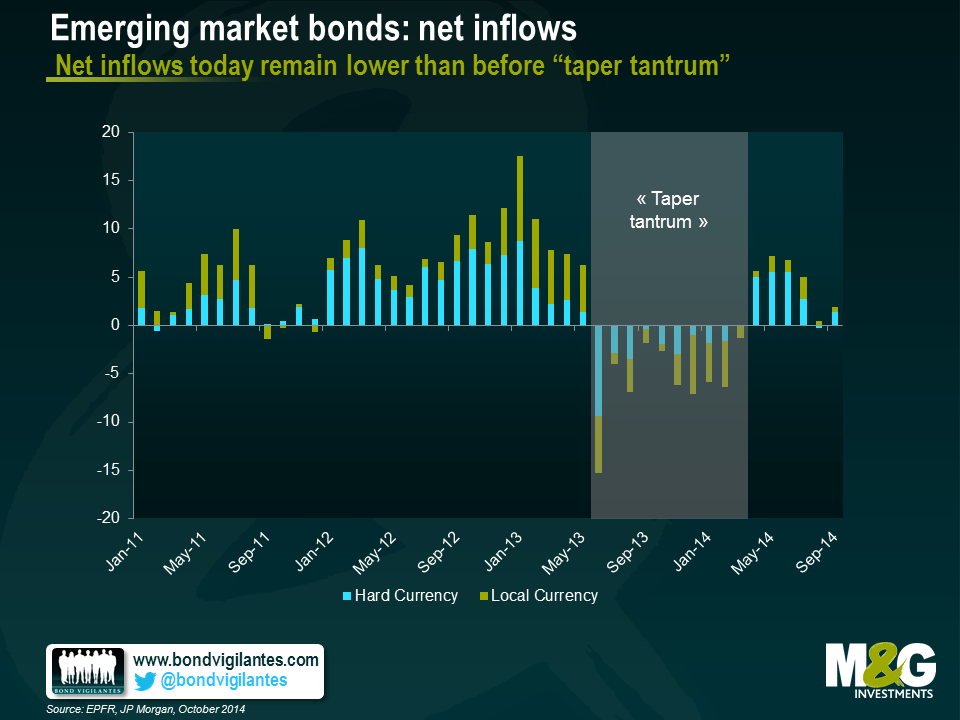

In terms of overall asset allocation, there is little consensus on what will outperform next year, whether it is external debt, local debt or corporates. More of a consensus, however, is the fact that return expectations are conservative, with low single digits expected. Reflecting this, inflows into the asset class are expected to remain positive, but materially below levels seen before 2013.

In local currency bonds, I believe the recent rally in US rates and fall in commodity prices warrants adding duration in some countries. Various EM Central Banks are willing to allow for additional currency weakening without the need to tighten monetary policy. They believe that any pressures on inflation will be perceived by economic agents to be temporary, particularly in countries such as Chile where an output gap exists, or in countries such as Colombia that have been tightening policy.

I expect returns to be more muted in hard currency next year and the gap between hard and local currency bond returns should not be as wide as this year’s. In addition, country selection remains key and we have already been witnessing this differentiation over the last few years.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

18 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox