Who’s the biggest winner if ECB buys corporates? The French

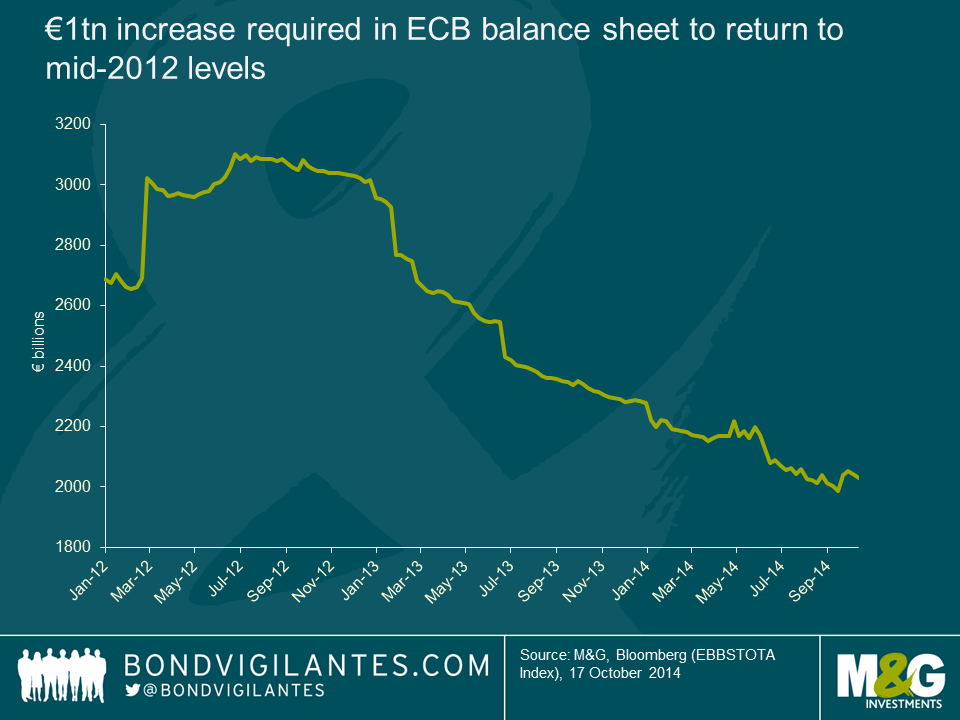

With the European Central Bank (ECB) purchasing €1.7bn of covered bonds last week, the Eurozone’s “QE-lite” programme has well and truly begun. Although the focus to date has been on covered and asset backed bonds, an article from Reuters last week spurred the market, due to a rumour that the ECB would soon be considering an extension to include secondary market corporate bond purchases. Although quickly dismissed by officials, considering that the ECB has previously stated that it wants to return its balance sheet to where it was in 2012 to boost demand (which in doing so would approximately equate to €1 trillion of asset purchases), many dispute that this can be achieved via covered bond and asset backed purchases alone. Given the notion that sovereign bond QE would essentially amount to central bank financing of governments, the next best alternative is likely to be corporate bonds i.e.“QE-plus”.

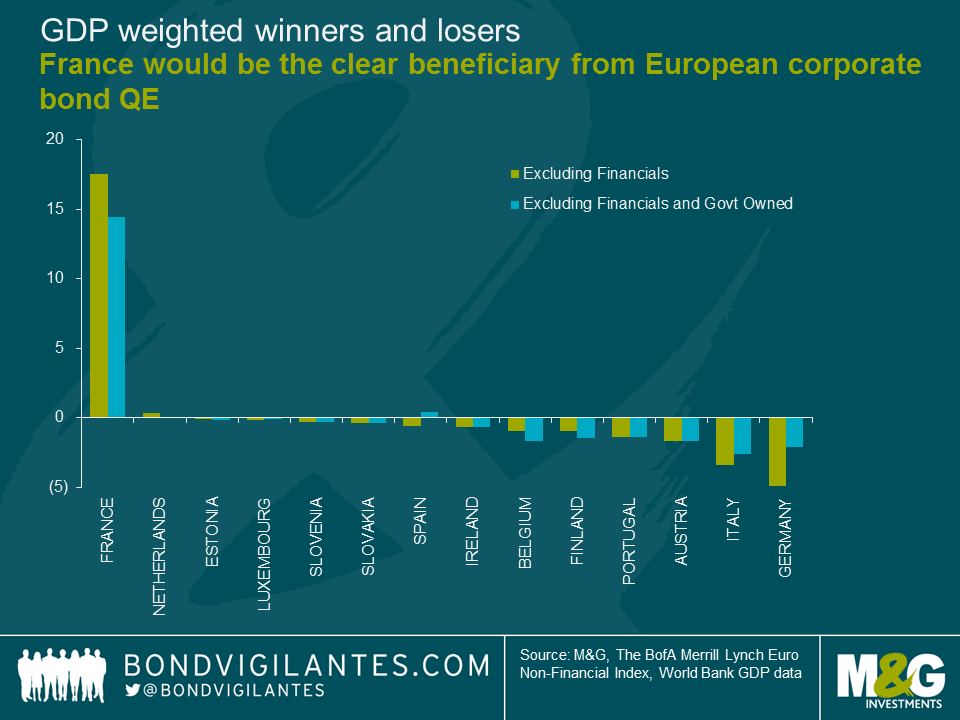

If QE-plus were to occur, which Eurozone countries would benefit the most? Assuming that the ECB will aim to purchase an equal spread of EUR denominated debt issued by Eurozone companies, I have filtered the Merrill Lynch Euro Non-Financial Index for these and reweighted to get a proxy for a theoretical ECB corporate bond buying universe. Next, I calculated a Eurozone GDP contribution for each individual country (note: Cyprus, Greece, Latvia and Malta have been excluded from the analysis as they were not included in the original index) and the difference between the two (i.e. the demand pick-up) has been measured in order to determine who could be the main winners and losers in a QE-plus world. Although this is a highly hypothetical approach, the results are nevertheless interesting. Constituting 21.7% of Eurozone GDP, but potentially representing 39% of all ECB corporate bond purchases, the 17.5% demand pick-up for France makes it the clear winner. The Netherlands is the only other country to witness a demand for its bonds in excess of its contribution to Eurozone GDP. All other member countries appear to suffer, especially Germany which represents over a quarter of Eurozone GDP, but ends up at the bottom of the table. For Estonia and Luxembourg the balance looks roughly correct. The periphery all witness less than proportional demand pick-ups, but Italy and Portugal look to suffer the most.

Adding a layer and assuming that the ECB would rule out the purchase of government owned entities – e.g. utility and industrial companies – in line with its opposing stance on central bank financing governments, gives us a further refined universe. Most countries continue to be benefit less than they’re due (owing to France’s gain) but on a smaller scale, excluding Belgium and Finland who are worse off. The main exception to this is Spain, which joins France and the Netherlands as a net beneficiary from ECB corporate bond purchases. The other key outlier is Estonia which previously was deemed just-right, but now loses out due to it no longer having any qualifying bonds in the new bond universe (its previous contribution to the index was via a government owned utility company).

Again I warn that this blog is highly theoretical in its approach, however the findings do provide food for thought. Though the ECB may aim for a uniform and decentralised approach, there will undoubtedly be political winners and losers (and this is not a clear-cut core versus periphery debate). This is especially true if the ECB continue to caveat their QE programme which acts only to reduce their potential investment universe. If the ECB are serious about overcoming the prospect of years of deflation, they should do away with QE-lite or even QE-plus and target the biggest, most liquid bond market via full-scale sovereign bond QE.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox