Panoramic Weekly – EMs: How many one-offs to call it a crisis?

Global bond markets sank over the past five trading days, as what started being idiosyncratic problems in specific Emerging Markets (EMs) spread throughout the bond universe: only 14 of the 100 Fixed Income asset classes tracked by Panoramic Weekly posted positive total returns. The rest tumbled, mostly dragged down by the risk-off scenario (such as High Yield debt) or by exposure to rising rates (such as long-maturity US Treasuries). In general, European sovereigns performed best, led by Italian bonds, which reversed previous losses as tensions with the European Union over the country’s budget deficit waned. Safe-haven currencies such as the yen and the US dollar rose – the latter despite another week of falling inflation expectations: the US’s five-year forward breakeven inflation rate fell to 2.07%, the lowest since June. Some investors are questioning whether US assets are now overpriced, something which may hinder global demand for them – therefore reducing inflation and interest rate levels.

But, as per the past five trading days, a rising greenback hurt EMs even more: Argentina raised rates to 60%, from 45%, to defend its currency and also asked the International Monetary Fund to accelerate payments of the programme they had already signed; the Turkish lira continued its slump, despite the central bank’s signalling the possibility of a rate hike later this month; and South Africa’s economy entered recession in the second quarter, dragging its currency down to a 2-year low against the dollar. Even the Mexican peso, until now relatively unscathed, has lost almost 2% against the dollar only since Monday. The only positive news seemed to come from China, which signed another $60bn investment package with African countries. Oil and most industrial metals weakened.

Heading up:

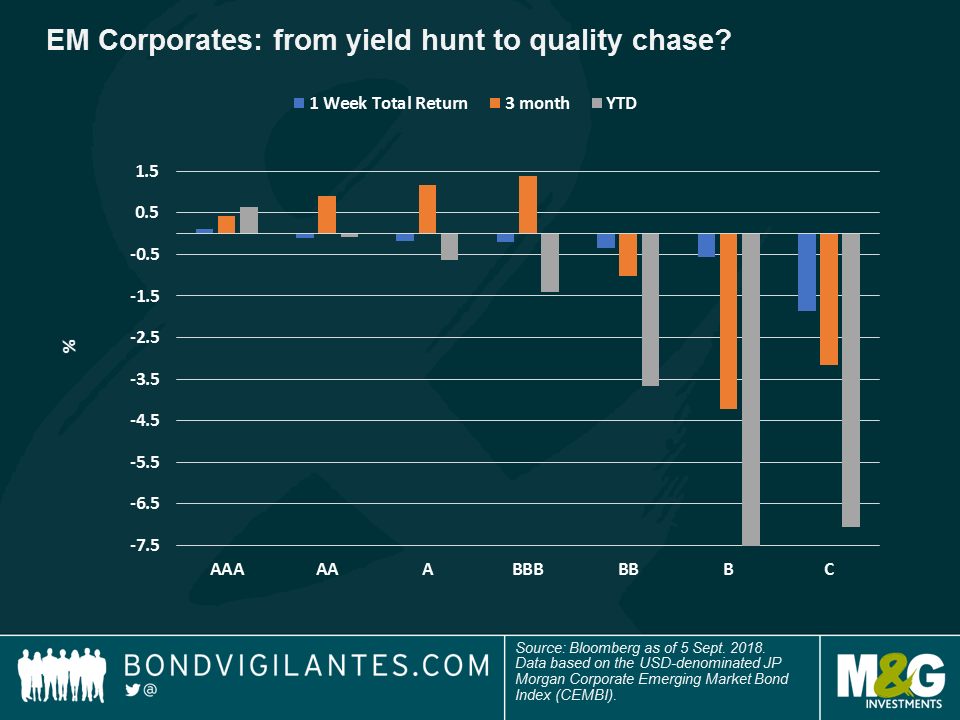

EM Corporates – top quality: After years going down the capital structure in order to pick up some yield, investors may now find what clothes shoppers have known all along: quality ultimately pays off. The highest-rated EM corporate debt is one of the very few survivors of the recent EM sell-off, posting positive returns over the past five trading days (0.1%), and 3-month (0.4%) and year-to-date (0.6%) periods. Within the US dollar-denominated JP Morgan Corporate EM Bond Index (CEMBI), top credit quality names are dominated by Asian companies, mostly South Korean utilities, Hong Kong transport giants and Chinese and UAE tech firms. In general, and so far this year, short-maturity bonds have performed better than long-term ones, as they are less exposed to rising rates, while the more predictable Transport and Industrial sectors have also fared better. By region, and also since the start of 2018, the Middle East offers overall positive returns, while European and Latin American corporate debt has fallen behind. By country, Ghana, El Salvador, Paraguay, Jordan and Iraq all offer a total return of at least 2% so far this year. For more insight on EM corporate debt, watch Mario Eisenegger’s video: “A tale from Chile and other off-radar EMs.”

European bonds – viva Italia: Italian sovereign bonds, known as BTPs, rallied 0.5% over the past five trading days, reducing their 1-month losses to 0.8%. The tensions between the government and the European Union over the country’s budget deficit eased after The League, which accounts for half of the ruling coalition government, started discussing a 2019 budget deficit below the European Union’s 3% of GDP limit, a level which would help the country reduce its whopping debt burden of 130% of GDP. Italian spreads over benchmark German bunds have come down to 250 basis points (bps) after reaching 289 bps last week, a level not seen since the European sovereign debt crisis in 2013.

Heading down:

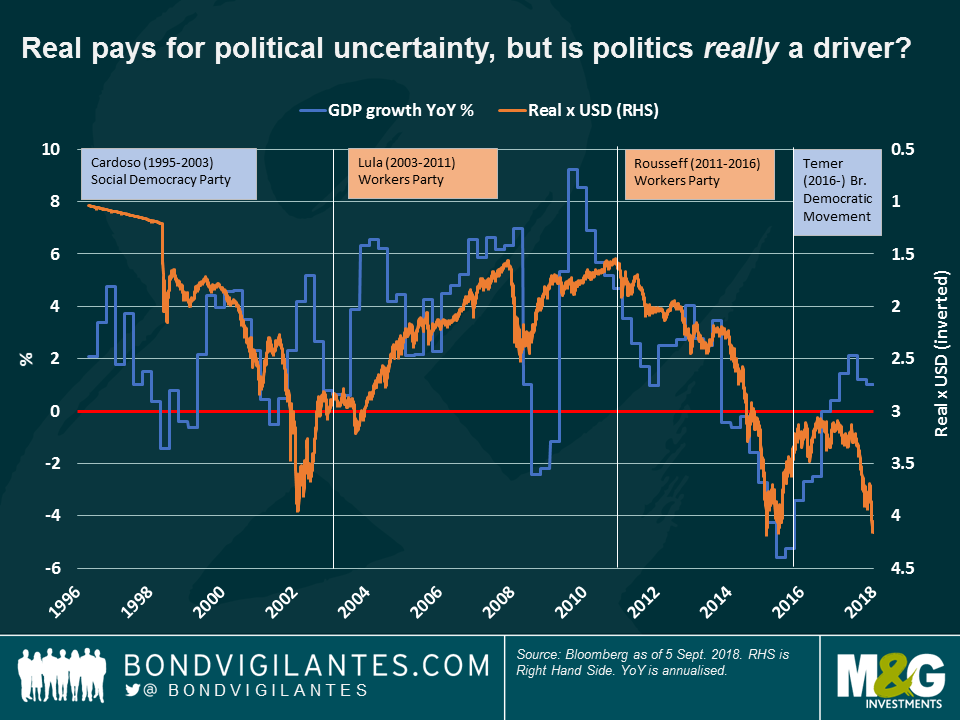

Brazil’s real – the price of uncertainty: The real continued its slump over the past 5 trading days, reaching on Wednesday its lowest level since 2015. It has lost 21% against the dollar only this year. Apart from the ongoing EM rout, the currency is also suffering from the uncertainty around October’s general election. Not even a court ruling that banned former president Lula, now in prison, from running again helped stem losses, as investors are still concerned that market-friendly candidate Alckmin is still behind other leaders in the polls. At present, right-wing candidate Bolsonaro is ahead, with 20% of the vote intention. Some experts, however, say that as candidates pass the first round to make it to the second and final one, leaders tend to tone down their sometimes extreme views as they need to capture a wide centre-voting electorate. Less polarised views may reduce uncertainty, albeit not the risk: Brazil’s current account balance sank into a US$4.4bn deficit in July, from a US$0.5bn surplus in June, while Industrial Production also dropped as companies held back on investments before the election. Despite the sharp pre-election moves, and as the chart below shows, both left and right-wing governments have ended up delivering a mixed growth and inflation picture. Much ado about nothing?

US High Yield (HY) size – taken over: The size of the US HY market, of about $1.2 trillion, has fallen behind that of US leverage loans, which rose to $1.3 trillion in June, according to Fitch Ratings. This happened as companies sought the cheaper financing offered by the loan market, as bank debt is typically less risky than bond instruments. Investors have also been lured into the loan market this year, attracted by the floating rate that some loans carry, and which rises as interest rates increase. However, the US Federal Reserve’s (Fed) recent dovish speech in Jackson Hole has raised questions about whether the central bank will stop rising rates next year, something which might reverse the HY-leverage loans trend again.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox