Arxada and the limits of the LME fear trade

The market increasingly treats liability management exercise (LME) risk as synonymous with coercion and value transfer. Sponsors have a range of technologies: dropdowns, up-tierings, double dips as well as other non-pro-rata outcomes. In structures with weak protections that instinct is understandable, but increasingly incomplete. Some credits with high LME optionality are delivering negotiated, consensual outcomes that preserve value, and in some cases, unlock upside.

Documents matter but they are rarely the complete story

A read of Arxada’s bond documentation, for example, makes clear just how flexible certain capital structures can be: capacity for additional secured debt through super senior baskets, dropdowns given limited ability to transfer material intellectual property or other assets into an unrestricted subsidiary (absence of so called J Crew blocker), and limited protections against non‑pro-rata transactions. For example, the Intercreditor Agreement can be amended and notes subordinated in right of payment, liens or priority with majority consent (lack of Serta blocker) enabling an up-tiering, as we saw in Victoria Plc.

But documentation is only one variable. Actual outcomes depend on a host of factors including but not limited to sponsor intentions, stakeholder dynamics, directors’ duties, composition and agenda of creditor groups. The existence of loose documentation opens credible routes to coercion. That downside can be priced into bonds, without recognising that it can also act to secure a cleaner deal for all stakeholders.

The real risk is fragmentation

For unsecured creditors, the key issue is less whether a transaction is formally coercive and more whether the group is coordinated. Fragmentation creates vulnerability. A divided creditor base can be picked off, with some groups advantaged and others left behind.

By contrast, coordination changes that dynamic. Creditors may still face concessions, through extensions, coupon adjustments, or exchange economics but they negotiate collectively rather than pursing holdout strategies. Cooperation is not a moral stance, it becomes a rational response to weak documentation.

Why Arxada is skewing towards a negotiated outcome

Arxada espoused multiple implementation routes, and they may have ranged from consensual amend-and-extend to scheme or more aggressive LME depending on creditor support. The availability of these options matters, as the sponsor does not need to execute the most aggressive path for it to shape behaviour.

The threat of a coercive path can push creditors towards a faster, negotiated deal. Sponsors have optionality, secured lenders are better protected by position, whilst unsecureds face real risks from fragmentation.

This dynamic shifts incentives. Rather than reject the process outright, unsecureds may be better served organising early, signing a Co-operative agreement if necessary, and negotiating for continued participation and upside. That may well mean accepting some burden-sharing in exchange for time, liquidity support and a more stable structure.

What a constructive deal looks like

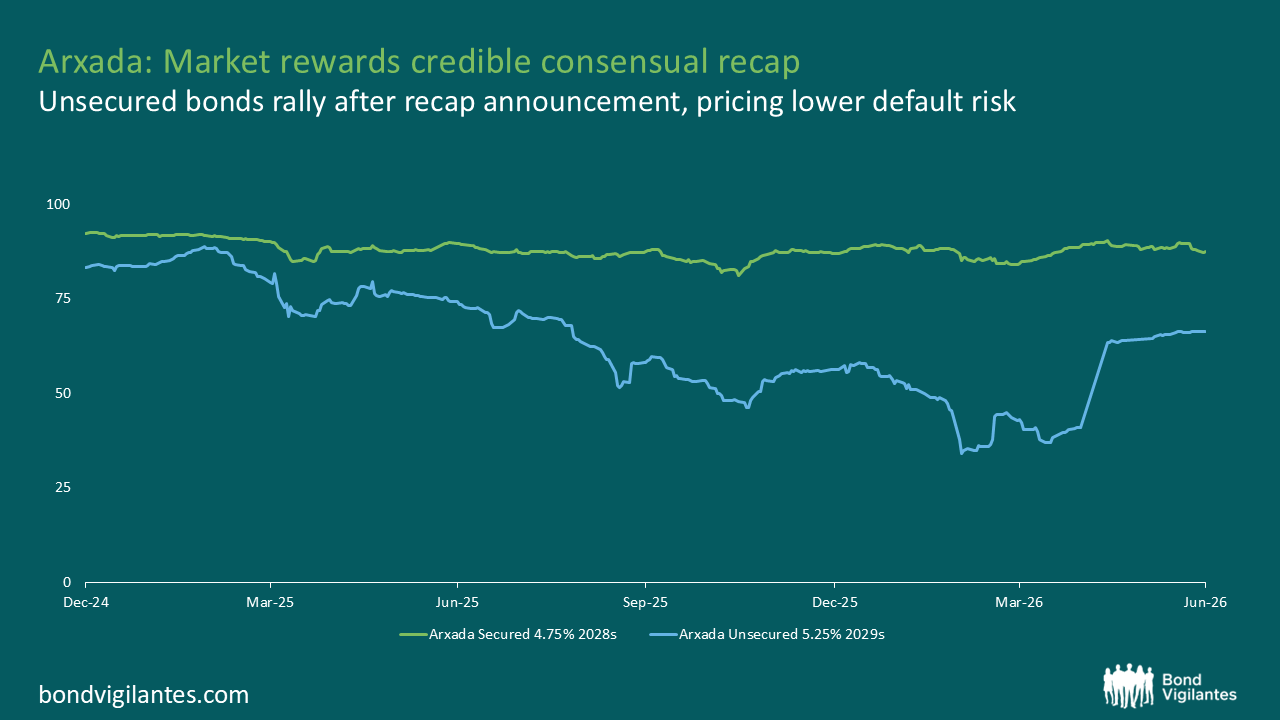

Arxada is delivering a constructive outcome, with both secured and unsecured debt extended at par. Fresh new money injection from Sponsors Bain and Cinven on a junior basis to secureds in order to support the transaction and provide liquidity. A covenant reset reduces future LME optionality in exchange for consent. Creditors gain a longer runway, continued exposure, and participation in any future recovery.

Source: Bloomberg, M&G

Why coercive is not always optimal

Aggressive LMEs are not costless. They introduce litigation risk, execution delay, reputational damage, and often result in more complex, harder to refinance capital structures. They may solve a near-term maturity wall but create longer-term constraints.

For a business like Arxada where recovery potential exists, preserving runway can outweigh winning a priority battle. Creditors including secureds ultimately need a functioning borrower and a financeable capital structure.

The investor implication: rethink LME risk pricing

LME risk is real, but markets continue to conflate legal optionality with likely outcomes. Many structures enable egregious actions; far fewer make them optimal.

The key question is not what issuers can do, but what they are incentivised to do. In cases like Arxada, the threat of coercion is often enough to drive a faster, more orderly outcome; importantly, without needing to execute it.

This is where LME risk is often mispriced. Investors focusing only on downside optionality miss the role it plays in shaping behaviour and securing consensual deals.

The more interesting opportunities today are not simply the ones with the weakest documentation, but situations where coordination can turn structural vulnerability into a negotiated reset, preserving value and upside.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.