The Bond Vigilantes World Cup Model

We are updating this blog daily with predictions, featured games, and market commentary from our bond experts.

Check back daily for the next instalment.

________

For the 2026 World Cup, the Bond Vigilantes team have designed a predictor model, combining economic fundamentals with official FIFA rankings to help forecast how the World Cup will play out.

Each day we will look at some of the most interesting games, and provide not only a predicted outcome from our model, but also some interesting (non-football-related) talking points from our usual bloggers, plus a few guests across the broader fixed income team.

Report back each day to see the latest predictions and country write-ups from our bond specialists.

The model

For those here for the model, below we have shared the formulae and rationale for the output.

The model is a 50/50 blend between a normalised FIFA points score, and a normalised economic metric score. Depending on the relative strength of the scores, an expected goals number is produced to predict the result of the game.

After several million runs of code, we have tweaked our economic model to produce the following output, based on population, real GDP growth, inflation, unemployment, policy rates, and finally, government debt-to-GDP ratios:

Econ Model: (LOG10(Pop)-6)^1.2 × (1+GDP/8) × 1/(1+Infl/8) × (1-Unemp) × 1/(1+Rate/20) × 1/(0.8+Debt÷GDP/5)

The rationale for the inclusion of the above metrics follows.

- Population is the bedrock of the model. Football is a numbers game: the more people you have, the more likely it is that a few of them can do something with a ball. We use a log scale because going from 5 million to 50 million matters enormously, but going from 500 million to 5 billion does not help you find a better left back.

- GDP growth captures momentum. A growing economy tends to mean investment in infrastructure, and with that comes football academies.

- Inflation is the instability penalty: when the price of a matchday pie is doubling every year, it is hard to maintain the kind of institutional stability that produces world class players.

- Unemployment is a proxy for development. Lower unemployment signals a functioning economy, disposable income for grassroots football, and parents who can afford to let their children train rather than study to work.

- The policy rate is a good signal for macroeconomic credibility. Countries with rates below 5% tend to be places where institutions work.

- Government debt to GDP is deliberately the weakest factor. Japan for example, at 255%, would otherwise be pushed too far down the rankings. We penalise heavy debt gently, like a yellow card rather than a red.

- Finally, we blend the economic score 50/50 with the FIFA world rankings (the official ones from 1 April) to stop the model producing results that are funny for thirty seconds and then become a credibility problem. Argentina finishing behind Curacao on pure economics is entertaining, but the rankings anchor reminds us that Scaloni’s squad is probably still quite good despite the peso.

Finally, we’ve sprinkled in a little bit of randomness as there is no shortage of variance in sporting events!

Joe Sullivan-Bissett, Investment Director

26 June

A dramatic result for Ecuador, beating Germany to avoid exiting the group stage. Japan and Sweden join them in the next round, while the Australia vs Paraguay draw guaranteed both qualification. Commiserations Tunisia and Turkey, whose World Cup journey comes to an end.

The final groups resolve over the weekend, with the first game in R32 kicking off on Sunday evening.

From those games, we focus below on Group K, where there is still plenty to play for with Colombia vs Portugal and DR Congo vs Uzbekistan.

For all predictions and a round up of results, scroll to the bottom of this blog.

Commentary on Colombia comes from Carlos Caranza, EMD Fund Manager:

Colombia’s local bond market is World Cup material already, delivering roughly a 20% return year‑to‑date, which is the top performer across EM local debt. If football mirrored fixed income… “la copa” would already be in their hands. On the pitch, the story is quite encouraging as well. Coach Néstor Lorenzo took office after the disappointment of missing the 2022 World Cup and has engineered a strong rebuild since then, with a very strong performance at Copa América 2024, where they lost the grand finale against Lionel Messi and 10 other less well-known players. Their qualification for the 2026 World Cup has been a walk in the park for them.

Tactically, the Colombia team lines up in a 4‑2‑3‑1, and that is exactly the trend that is needed for the primary fiscal deficit, which might be achievable given the incoming administration has signalled its intention to tighten fiscal dynamics. Coach Lorenzo is known for his strong tactical discipline. If this is the policy of the next administration, markets will notice that hips and fiscal dynamics don’t lie. Let’s make Shakira proud.

And for Portugal, it’s Ben Lord, Macro Credit Fund Manager:

Portugal came into the tournament ranked 14th on the Bond Vigilantes model, despite being 4th favourite to win. A solid second quartile football team on paper, in bond speak. In macroeconomic terms, though, this underplays the significant improvements seen in peripheral European countries versus their core EU peers since the sovereign debt crisis in 2011-12. But within the peripheral nations that found themselves in the crisis, only Spain can be mentioned in the same breath as Portugal in terms of the improvement both in the fiscal position and in terms of the football team heading to the World Cup. In the camp of the economic recovery being stellar, but football letting them down, we have Italy, Ireland and Greece.

Back then, though, mid crisis, whilst the economy was on its knees with debt to GDP of around 130%, the team had one of the two best footballers in the world playing at the very top of his game in Cristiano Ronaldo. Today, with debt to GDP back down to 85-90% and the economy humming along with real GDP of around 2%, Ronaldo is well past his best. Questions remain though over who was the best, Ronaldo or Messi. The answer very simply is Messi, and I think we have seen enough evidence in the last couple of weeks to support that. And for what it’s worth, Maradona is the only person in the debate with him. Not Ronaldo. Sorry Portugal fans.

The Portugal team are strong and have a team that can probably beat anyone on their day. But questions will be asked as to whether they can mount a sustained tournament challenge with the team’s top players like Ronaldo being 41 and Bruno Fernandes and Bernardo Silva being 31. Similarity can be drawn to the economy here though, with an ageing population in Portugal (as well as elsewhere) pressing down on growth and on the public finances. However, the future is bright as the engine room of the team look solid too, with Vitinha, Nuno Mendes and Joao Neves all in their primes. Unemployment is low, participation is rising, debt levels continue to improve, and the economy’s focus on services immunises the nation from any unpredictable and damaging tariff noise, wherever it may come from.

Portugal and Spain both arrive at this World Cup with strong economic recoveries post crisis, strong growth, and lower levels of debt. But for this great rivalry, Portugal come a distant second: capable of beating anyone on their day, but with too much reliance on an ageing population in the team to match Spain.

With commentary on DR Congo, it’s Purvi Harlalka, EM Sovereign Analyst

The DRC has only played in the World Cup once before – in 1974, when it was called Zaire. They lost all three group games without scoring, including 9-0 against Yugoslavia. In an interesting analysis of footballing success, the Economist notes that the best predictor of where a country ranks today is where it ranked decades ago. It posits that by its calculation of footballing quality, around 80% of the countries in the top quarter of the league table in 1976 are still there. Let’s hope that the DRC’s comeback gig looks more like the one the NY Knicks pulled off, rather than the outcome the model foresees.

DRC has already clocked one milestone in 2026 so far – that in the bond markets where it raised USD 1.25bn in a debut sovereign Eurobond issue in April. So enthusiastic are EM investors about their own asset class (or lacking in ideas, or both) that they were willing to be paid a mere 8.75% for 6yr USD paper when local banks were receiving 9% for 1.5yr lending in USD! Such generosity on the part of investors looks particularly curious when you consider the fact that DRC is currently not a nation in full control of its borders. “Rebel” Rwandan forces, the M23, currently administer the districts of North and South Kivu in Eastern DRC, sites that contain the majority of the world’s coltan in addition to vast deposits of the 3T’s (tin, tungsten and tantalum) vital to global automotive and tech production. Instability in these regions cost 0.4% of GDP in lost revenues in 2025, not to mention its burden on the fiscal via security related spending. It is the pursuit of these “critical minerals” that also explain the Trump administration’s recent embrace of DRC, as it attempts to get one up on China in the tech race. To that end the US has managed to secure preferential access rights to DRC’s vast mineral resources on generous terms, in return for very little actual investment or military support- another reason investors should be wary.

Eastern DRC is also the epicentre of the latest Ebola outbreak in the DRC, a fact that has made it harder to contain given it is a conflict zone with 250k individuals displaced from their homes and their movement across porous borders into neighbouring countries. For all its cosying up to the Congolese, the White House denied entry to the DRC football team unless it agreed to isolate for 21 days in Europe, en route to the US, which it duly did. As they arrived last Thursday, kitted out in tuxedos and leopard print sashes, the welcome the Leopards received at Houston airport was rather warmer. Given everything they’ve had to overcome just to get there, the fact of being at the World Cup at all probably feels more significant than anything that follows.

For their opponents, Uzbekistan, it’s Eldar Vakhitov, EM Sovereign Analyst:

Uzbekistan is competing in the World Cup for the first time in its history. Facing opponents from different continents – Europe, South America, and Africa – during the group stage is likely to raise global awareness of the country and highlight its impressive development trajectory. In fact, a booming tourism industry is already rapidly becoming a significant force in the economy. Getting valuable experience on the international stage has been important both for the football team and government authorities in recent years – and the market has noticed significant improvements both on the pitch and in the quality of economic policymaking.

While the team’s first two matches ended in defeats against Colombia and Portugal, there were never any expectations for Uzbekistan to contend for gold medals in this tournament. Notably, the country is already among the world’s leading gold producers, a factor that has provided resilience during periods of market volatility. In short, for Uzbekistan, participation in the World Cup already represents a significant achievement. Another achievement may come from a further increase in foreign participation in local currency bonds, as investors have been attracted by double-digit yields and exchange rate stability, alongside a consistent reform narrative and solid macroeconomic fundamentals.

All predictions are shared at the bottom of the blog.

Previous posts follow:

25 June

It is worth starting by saying that yesterday’s pause in posting was always planned, not in response to England failing to secure first place in their group with a win over Ghana.

Elsewhere, lots to celebrate for Mexico (winning their group), South Africa (qualifying for the knock-out stages for the first time in history), Switzerland (beating Canada to secure top spot), and both Brazil and Morocco, which secure qualification with 7 points apiece. A nervy wait for Scotland to see how the rest of the third place teams perform to see if they make it through, fingers crossed.

As we move into the final few days of the group stages, today our featured game is Japan vs Sweden.

For all predictions and a round up of results, scroll to the bottom of this blog.

For Japan, we have commentary from Eva Sun-Wai, Global Macro Fund Manager:

Japan arrives at the World Cup with a strategy that hopefully moves a little quicker than the Bank of Japan. While other central banks spent the past few years sprinting through tightening cycles, the BOJ approached rate hikes with the urgency of a team protecting a 0-0 draw in the group stage. After finally exiting negative rates and beginning the long journey towards policy normalisation, officials continue to remind markets that “gradual” remains the operative word. Inflation has spent years above levels that previous generations of Japanese policymakers could only dream of. Wages have been sticky, and yet each policy adjustment continues to be analysed with the intensity of a VAR review.

Japan’s World Cup record is similarly understated. Since 1998, they have qualified for every tournament and reached the knockout rounds on multiple occasions, but are still waiting for a first quarter-final appearance. The JGB curve has finally rediscovered the concept of steepness, and long-end yields have moved enough to remind investors that Japanese duration does contain risk. Much like Japan’s football team, the question is no longer whether it belongs on the big stage, but whether this is finally the year it goes a round further.

And for Sweden, it’s Tess Britton, Credit Research Analyst:

Sweden is returning to the World Cup with a reputation for discipline and consistency, but can that same stability translate into outperformance both on the field and in its financial markets?

Sweden continues to run one of the strongest fiscal frameworks in developed markets, with relatively low government debt and a long-standing commitment to budget balance. This provides a high degree of credibility and flexibility in navigating cycles.

On monetary policy, the Riksbank has already pivoted to easing ahead of peers. After hiking to ~4%, rates are now 1.75%, reflecting faster disinflation and a weak growth backdrop; the current stance is heavily data-dependent.

Growth is modest and volatile, with very high household debt (~180% of income) making consumption and housing extremely sensitive to rates, a key driver of both the slowdown and disinflation.

Sweden entered the tournament without a full-strength squad. Tottenham forward Dejan Kulusevski was ruled out after a long-term knee injury and multiple surgeries prevented him from recovering in time for the World Cup, making him one of the most notable absences. However, that absence did not show in the opening game as they brushed past Tunisia 5-1. But that one good result did not last five days before the numbers reversed, the 5 became a 1 and the 1 became a 5, losing by the same scoreline to the Netherlands.

Where policymakers are carefully managing a slowdown, the football team will hope that their own setbacks remain contained by avoiding further disruptions that could weigh on their tournament performance. Sweden may not always be the flashiest; their structure, discipline, and consistency mean they are rarely an easy opponent in global markets or at the World Cup.

23 June

Another win for Argentina, another brace from Messi.

Another win for France, another brace for Mbappé.

England and Harry Kane, over to you.

For all predictions and a round up of results, scroll to the bottom of this blog.

With commentary for Ghana, it’s Purvi Harlalka, EM Sovereign Analyst:

Of the 48 teams at this World Cup only Curacao, Haiti and New Zealand have a lower ranking than the Ghanian Black Stars, who sit down at 74th (as of 4 June). It wasn’t always so. Ghana reached six straight Afcon semi-finals from 2008-2017 and were one handball away from reaching the semi-finals in the 2010 World Cup. But the country, which has competed in 5 of the last 6 World Cups, gave manager Otto Addo the boot in April after failing to qualify for the AFCON last year, placing their faith in Portuguese veteran coach, Carlos Queiroz, to steer them through the 2026 tournament instead. He has had only 65 days to work his magic. Some magic would indubitably be required to extract gold from a squad missing its key winger, two key centre-backs (injured) and a star midfielder (refused a Canadian visa because his application lied about outstanding criminal charges).

Gold-extraction in its literal, physical form has however been far more successful, perhaps even a bit too successful in Ghana- Africa’s largest gold producer. In 2025, Ghana produced a record 6 million ounces, of which large scale mines contributed almost half. The rest came from “artisanal” mining – “panning” riverbeds with pickaxes, shovels and a sieve, at its most basic – an activity that has sky-rocketed alongside global gold prices. Artisanal mining has long been a licensed activity in Ghana but a surge in illegal mining, known locally as “galamsey” (gather and sell), became so prevalent and polluting of water resources that it began to degrade tracts of land used to grow crops like cocoa- another key export. It also led to large scale gold smuggling to Dubai, causing the state to forgo more than USD 11bn over 2019-2023 according to the non-profit Swissaid. Ghana has since enacted several key reforms in its gold sector that have gone a long way towards formalising it and capturing the FX flows it generates. This has in turn helped to stabilise the exchange rate, catapulting the Cedi to the position of the best performing currency globally in 2025! Ghana’s central bank has also been the world’s most enthusiastic buyer of gold for its own FX reserve kitty, which has consequently grown to an impressive USD 14bn (5 months of imports). It accumulated said gold by compelling large-scale miners to sell 30% of their production to it in local currency. At its peak gold was a whopping 40% of FX reserves, at which point the Bank of Ghana thought it wise to rebalance towards more prudent levels (20-25%).

It would be patently unfair to put down all of Ghana’s success to gold. The country has also really cleaned up its act overall, and not just in its gold industry. It is arguably the most successful of the recent frontier market restructuring stories, especially if measured in terms of the reduction in its debt burden. This is primarily because Ghana took the bulk of the pain upfront, rather than deferring it via State-Contingent Debt Instruments (SCDIs) that are all the rage these days in post-default debt stacks. The comparative debt metrics speak for themselves. Debt to GDP in Ghana was a mere 48% of GDP at end 2025 vs 86% in Zambia and over 100% in Sri Lanka. However, there is still work to be done to embed the sustainability of this marked performance and vigilance against slipping back into the old ways is required. The rallying cry for both the nation and its football team is one and the same – onward and upwards!

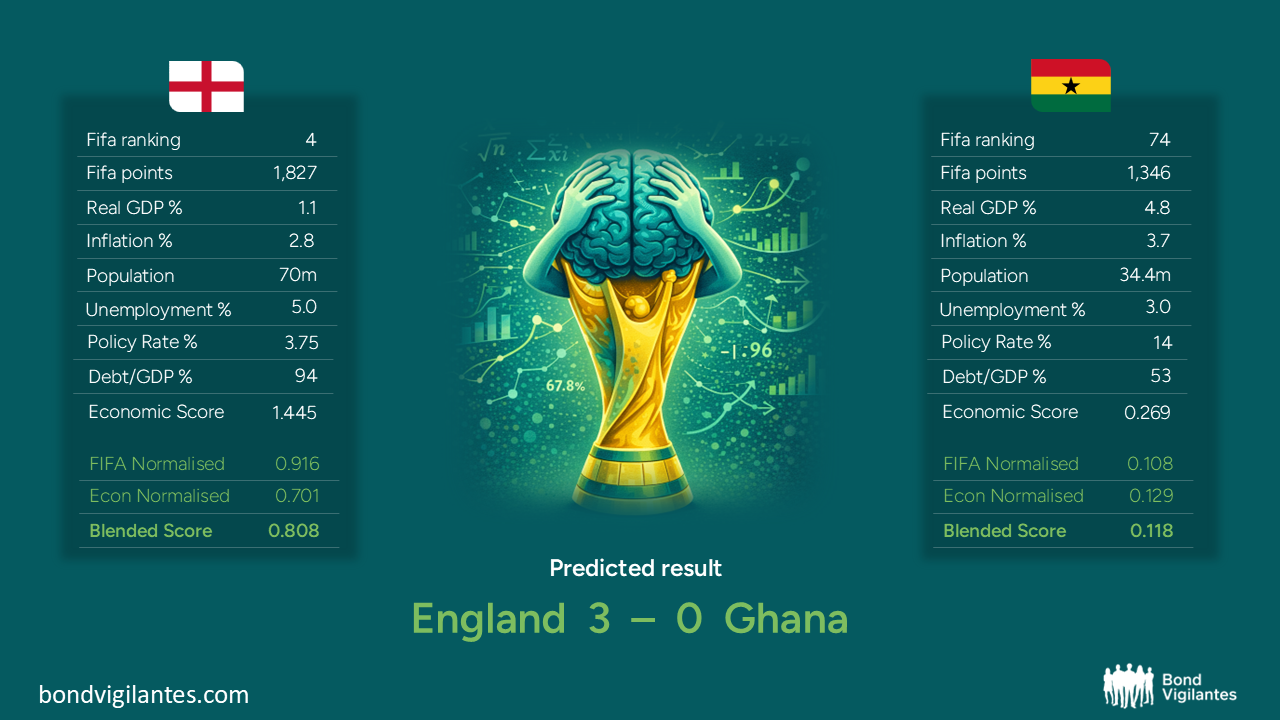

Having already covered England’s previous game (see write-up from 17 June below), here is a match summary taking into account the opening games and recent political events.

- England got off to a flying start against Croatia, playing attractive football going forward with the talisman Harry Kane playing anywhere from striker to sweeper. At the back they were less convincing, especially in the first half. Back at home, there has been a lot of news to digest since the opener. Andy Burnham outperformed expectations in a by election to become a Member of Parliament, and with a tweak of tactics from the Labour Party over the weekend, now appears to have a credible path towards becoming the next Prime Minister. England’s captain Harry Kane earned the nickname ‘King of the North’ from his time dominating North London Derbies – perhaps similarly nicknamed Burnham’s likely imminent coronation is the inspiration the England camp need to bring it home. Let’s start by seeing if the model gets this one right.

- Ghana got off to a great start, nudging past Panama with the only goal in the game in the 90+5. With the likes of Semenyo and Ayew (Jordan, with Andre being left off of the final roster), there is always a threat – something England will need to manage. At least England’s defenders, Stones, O’Reilly and Guehi (if he plays) should know how Semenyo thinks. Not that that means they’ll be able to stop him. Ghana hope to build on their three-point tally over the next two to make it through to the next round, although with a 14% interest rate dragging their normalised economic score downwards, the model isn’t assigning a high probability of that.

22 June

Another weekend packed with goals, drama, and surprises, including Ecuador drawing with Curacao and Uruguay being held to a draw by Cape Verde – who are quickly becoming the story of the tournament.

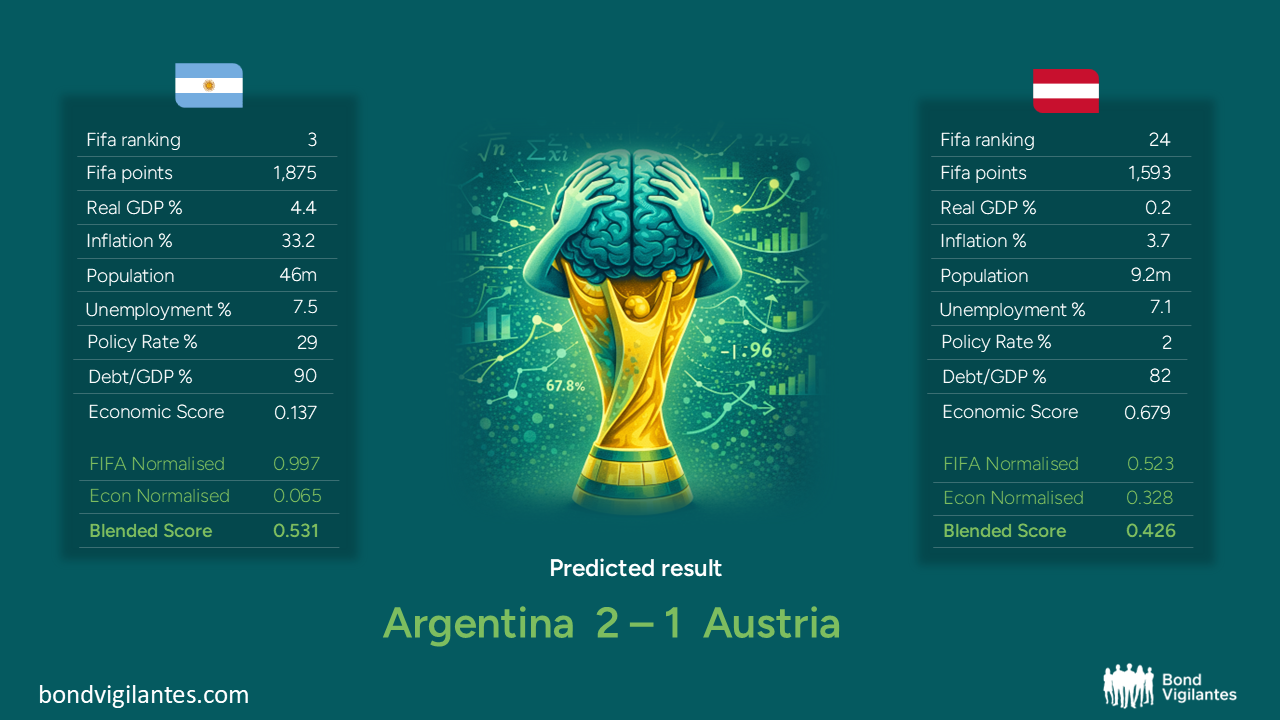

For all predictions and a round-up of results, scroll to the bottom of this blog. For this evening’s games, we focus on Argentina vs Austria.

Commentary for Austria comes from Nick Smallwood, EMD Fund Manager.

Austria will be hoping that 2026 marks a turning point in their footballing fortunes: qualification for the 2026 World Cup brings a long-awaited end to a dry spell dating back to 1998, when they were eliminated in the Group stages. While this young, energetic and high-pressing team will have their work cut out to match their forbears’ third- and fourth-place finishes in 1954 and 1934 respectively, they will fancy their chances of safely navigating a Group containing Argentina, Algeria and Jordan. Although the results since the mid-‘50s have been less stellar, Austria can still draw inspiration from some famous wins against Spain and West Germany in 1978, while the more superstitious fans will cling tightly to the fact that Austria’s last World Cup win came against the US (the current hosts) in 1990. Moreover, one sole defeat in qualifying shows that optimism around this team is justified. While the correlation between football and politics is famously low (Austria’s main footballing strength comes from players on the left wing, such as Laimer and Sabitzer), we are hopeful that it provides a closer resemblance to economic reality. The latest economic forecasts from the European Commission see Austria’s GDP growth improving from 0.6% to 0.9% over the next year, while inflation is set to fall from 3.0% to 2.5%, with the current account balance also set to improve from 0.7% to 1.3% over the period. A relatively high budget deficit of 4.1% remains little changed, with unemployment also sticky but trending downwards from 5.8% to 5.6%. The economic trend, then, remains positive if unexciting, with bonds priced accordingly (attractive vs Bunds but less interesting/liquid that the Italian and French curves). Austria clearly faces headwinds both economic (energy prices) and footballing (Argentina). If it can successfully navigate those, 2026 could well mark a positive inflection both on and off the pitch.

Having provided a write-up for Argentina already (see post from 16 June below), we have Carlos Carranza, EMD Fund Manager, with a match preview.

Consensus is overwhelmingly in favour of Argentina, which is always a headache for the favourites. As with inflation, pressure can often worsen the outcome. Still, we are in for a treat in the next game, with both teams making a strong start.

- In Argentina’s case, the Malbec producers dispatched Algeria 3–0, while its hard currency bonds have returned nearly 9% year to date. High carry, strong fiscal dynamics and a hat-trick from Messi have driven the solid results so far. The risk is that such strong performance appears concentrated in a one-man show: “Lionel… Milei”.

- Meanwhile, Austria beat Jordan 3–1. Romano Schmid opened the scoring with a superb long-range effort (well worth a watch on YouTube if you have not seen it), followed by an own goal from Jordan (cue “get to the chopper”…), and then a penalty. Austria’s 10-year benchmark has been range-bound, delivering a modest 1% year to date. Unsurprisingly, the football highlights have been far more exciting than the bond performance, which is typical of a steady, investment-grade, low-volatility market, especially compared with emerging markets.

But consensus is consensus for a reason. Austria may put up a good fight… but Argentina has the Terminator.

19 June

Thumping victories by both Canada and Switzerland, recovering strongly from their respective draws in the first round, whilst Mexico make it two wins for two in front of their home crowd – potentially a daunting round of 16 match-up for England should both teams make it.

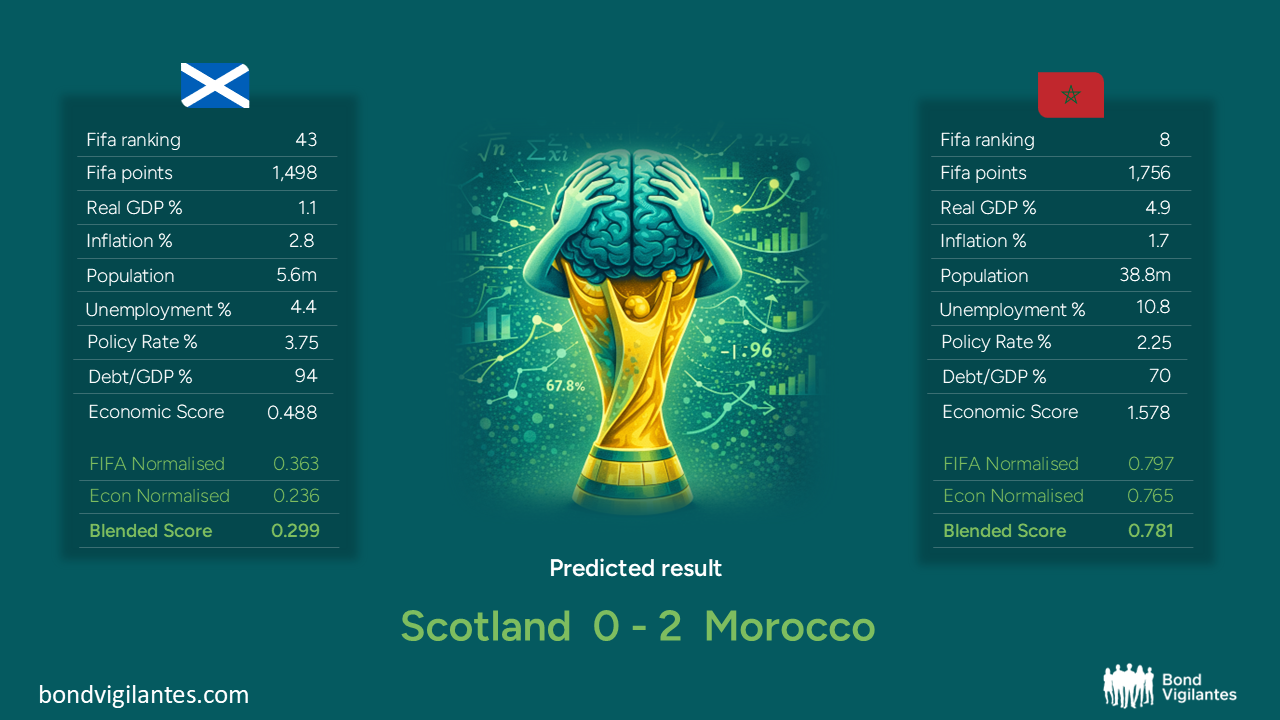

Onto the next set of games, and taking you through the weekend we start with Scotland vs Morocco – where the model predicts a disappointing evening following the opening week win for the former, and New Zealand vs Egypt – where the model again favours the chances of the African representatives.

For all predictions and a round-up of results, scroll to the bottom of this blog.

For Scotland, comments provided by David Walker, Head of Fixed Income Dealing and Ben Lord, Macro Credit Fund Manager, with the latter adding a touch of humour about the Sons of Scotland.

Scotland has returned to the world cup after a 28-year absence since 1998. Back then, the Scotland Act of 1998 was created that established the devolved Scottish Parliament and Scottish Government. This reshaped UK governance. Scotland’s growth has been slow, similar to the football teams success. Scotland is one of the most recognised countries globally with their traditional dress, as is Archie Gemills wonder goal (at least by Scots) against Netherlands in 1978 remembered for his poised prowess and spectacular vision.

Post devolution there has been discussion around Scotland issuing its own government bonds, ‘kilts’, and in some cases moving towards full independence. In government bond market terms, were Scotland independent today it would likely involve issuing its own bonds against a backdrop of a budget deficit in the low double digits as a share of GDP, compared with around 5% for the UK at present. That would be high by most developed market standards, even alongside the US. Natural resources, including oil, would form part of the picture, but as ever the outcome would depend on the policy framework, growth assumptions and the credibility of the overall fiscal path.

There have been highlights since 1998: everyone knows that Irn-Bru is made in Scotland from girders, this could be the stable ingredient that has kept the labour market highly resilient, the football team have also had victories against France & Spain. The rugby team dominates the Auld Enemy every 6 Nations campaign, but as yet can’t take that dominance into World Cups. Perhaps the football team this time can? There have been memorable lowlights too with Royal Bank of Scotland collapsing in 2008 as did the Tartan Army when they lost 3-0 to Kazakhstan in 2019.

Scotland is famous for its exports with Scott Mctominay’s move to Napoli raising his form and value to the national team, this export could be as important as Single Malts propping up the Scottish economy. McTominay’s overhead kick in the qualifiers, celebrated as one of the most iconic goals in Scottish football has even been celebrated with a limited edition Bank of Scotland £20 bank note joining Sir Walter Scott and the iconic Forth Road bridge. Other ‘Sons of Scotland’ include Alexander Graham Bell born in Edinburgh who we all know went on to invent the telephone, and David Walker, who runs the fixed income dealing desk at M&G.

One thing is for certain though: whether or not the football team can progress beyond the group stage this time round, the fans called the Tartan Army will be at the World Cup in serious numbers and in McMammoth voice! Scottish fans are amongst the best in any tournament they play in, and US, Canada and Mexico will see and hear their presence even longer than the team remain in the tournament. Were there a World Cup for fans, Scotland would be a regular top 4 team in the world. In 2024’s Euros, whilst the team failed to make in through the group stages, the noise ‘The Army’ made at all their games was remarkable on TV and in person at the grounds, and an astonishing 4% of the population of the nation travelled to support their team, placing them in the top echelons of fans by this measure.

During the world cup 1998 Scotland faced Brazil in the group stages losing 2-1, they have the chance to rewrite history as they play them again. Brazil may have Vinicius Junior & Raphinha however Scotland have McTominay & McGinn. Brazilian cuisine is vibrant similar to how Brazilians are expected to play football. Haggis, Neeps and Tatties, sheep’s heart, liver and lungs – heart is the essence of the Tartan army.

Versus opponents Morocco, with commentary from Eldar Vakhitov, EM Sovereign Analyst:

Morocco is making its seventh appearance at the World Cup. Its standout achievement came in 2022, when it became the first African nation to reach the semi-finals. Along the way, Morocco defeated its main trading partner, Spain, in the round of 16, and later overcame neighbouring Portugal in the quarterfinals. The Iberian Peninsula nations were evidently impressed, as they later joined Morocco in a joint bid to host the 2030 World Cup.

On the economic front, the government has steadily narrowed its budget deficit in recent years, while the central bank has maintained firm control over both the exchange rate and inflation. Much like its football success, it was a team effort that has led to a good result, delivering robust economic growth of around 4-5% per annum. And this was achieved with just 1% average inflation in the past couple of years – a feat that’s hard to beat. In fact, the football team is even harder to beat: getting a draw with Brazil in the first round meant that Morocco set the new record of longest undefeated run in international football – 38 games in a row!

However, to cement its status among the elite and gain full acknowledgement from the fan investor community, Morocco should try to replicate their previous success: both at the World Cup and by getting a second IG rating this year (they already have one from S&P). Perhaps Moody’s and Fitch should take a closer look – much like a VAR review – at the country’s credit profile sometime soon.

New Zealand commentary provided by Mark Ellis, Fundamental Fixed Income Fund Manager:

New Zealand is a small country with 5.3 million people and is known for winning rugby world cups, wine, and lots of sheep (23 million of them) not soccer. It is the lowest ranked team ranked team coached by an Englishman and have failed to win a game in the last two world cups. So I am not going to try and pull the wool over your eyes and say they can easily win this this one. The odds of winning or even just winning a game are low. Polymarket has the odds of winning any of the three group games at less than 20%. The market thinks there is only a 9% chance of winning against Belgium. So the odds are low, but not zero, and we all know the market can behave like a herd of sheep and misprice risk. Herds love the favourite and hate the underdog. New Zealand is an underdog, but upsets happen, things go wrong and black swan sheep events happen all the time. 9% chance is the wrong price, let’s not forget New Zealand drew all their games in 2010! Another example of the market getting it wrong is the current New Zealand government bond yr vs 10yr spread at 100bps, a significant pickup when compared to US, EU and even Australia at 35bps, 40bps and 37bps respectively. New Zealand 10yr government bonds looks cheap. So, rather sheepishly I have two recommendations: long New Zealand to win a game and long the 10yr government bond. If New Zealand don’t win, well then at least you have the roll down of the government bond…

Against Egypt, with commentary again from Eldar Vakhitov,EM Sovereign Analyst:

Egypt is participating in the World Cup for the fourth time, with previous appearances in 1934, 1990 and 2018. The team’s progress in recent years mirrors the country’s broader economic transition from a relatively closed, state-led system towards a more open, market-oriented model. Addressing macroeconomic imbalances – particularly on the fiscal and external fronts – has been a key priority for policymakers. As Egypt demonstrated in their opening match against Belgium (ending in a 1-1 draw against a very strong opponent), a more balanced approach with thought-out counterattacks can yield better results compared to spending the team’s resources on just defending. The central bank’s decision not to spend its international reserves on defending the exchange rate during recent episodes of market volatility have also been welcomed by foreign investors. Given that Egypt’s economic transformation relies significantly on key external funding sources – much like the national team heavily depends on its star players based abroad – it will be important to maintain the momentum and avoid complacency. The current year presents a meaningful opportunity for Egypt to take a further step forward, both economically and on the football pitch, where a first-ever play-off qualification is well within reach.

18 June

England got off to a flying start with a six-goal cracker, whilst Portugal can be added to the broad list of favourite teams held to a draw by resilient opponents.

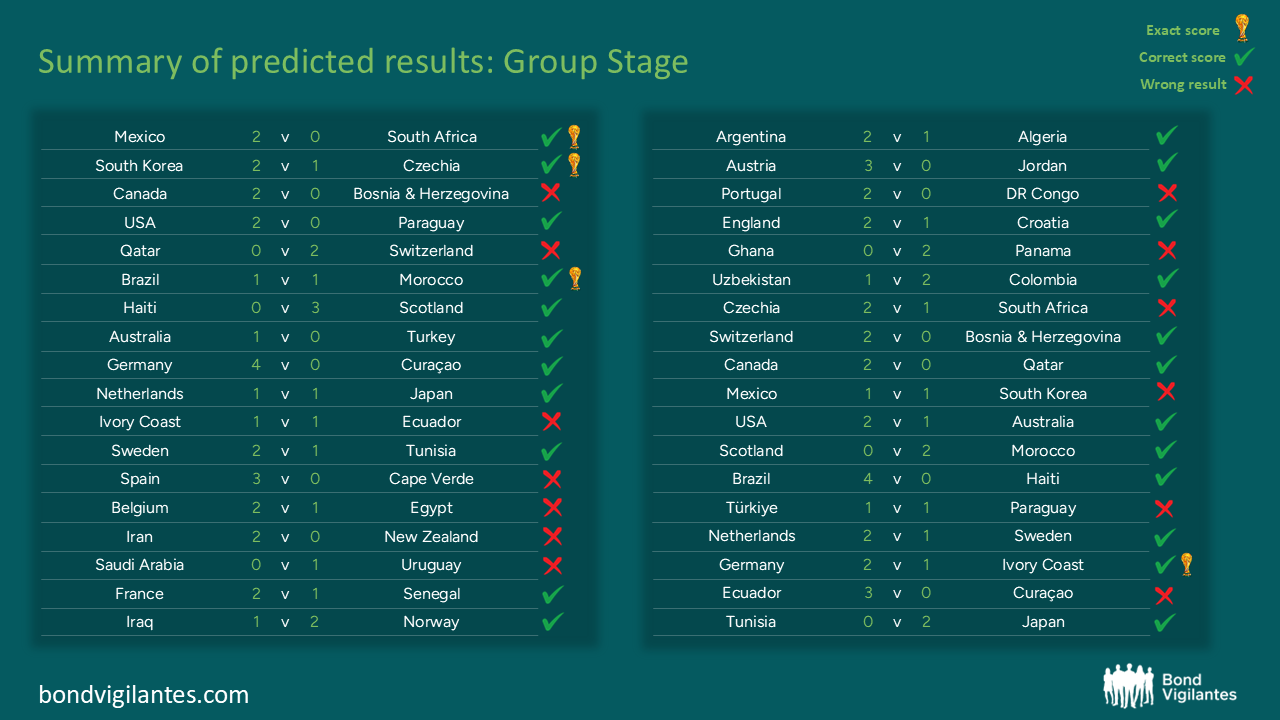

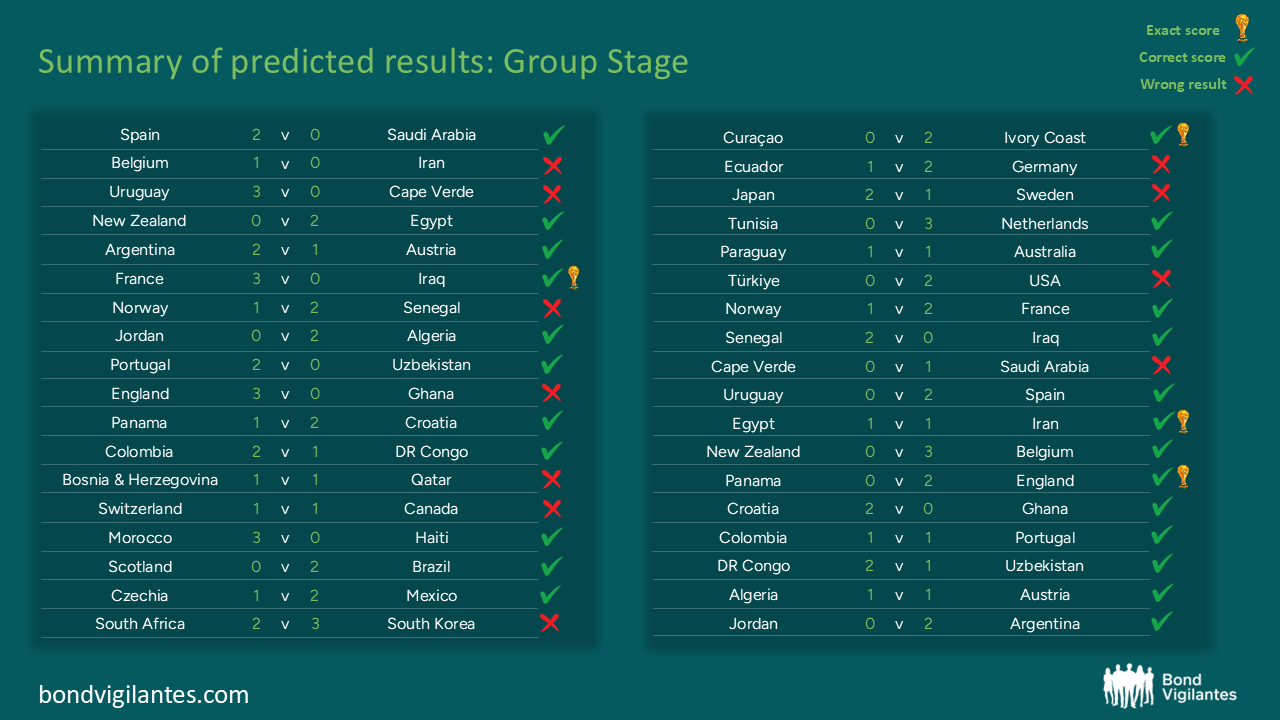

That’s the first set of 24 group games complete, with the model predicting 15 out of 24 games. Let’s see if that 62.5% hit rate continues through the next round of 24.

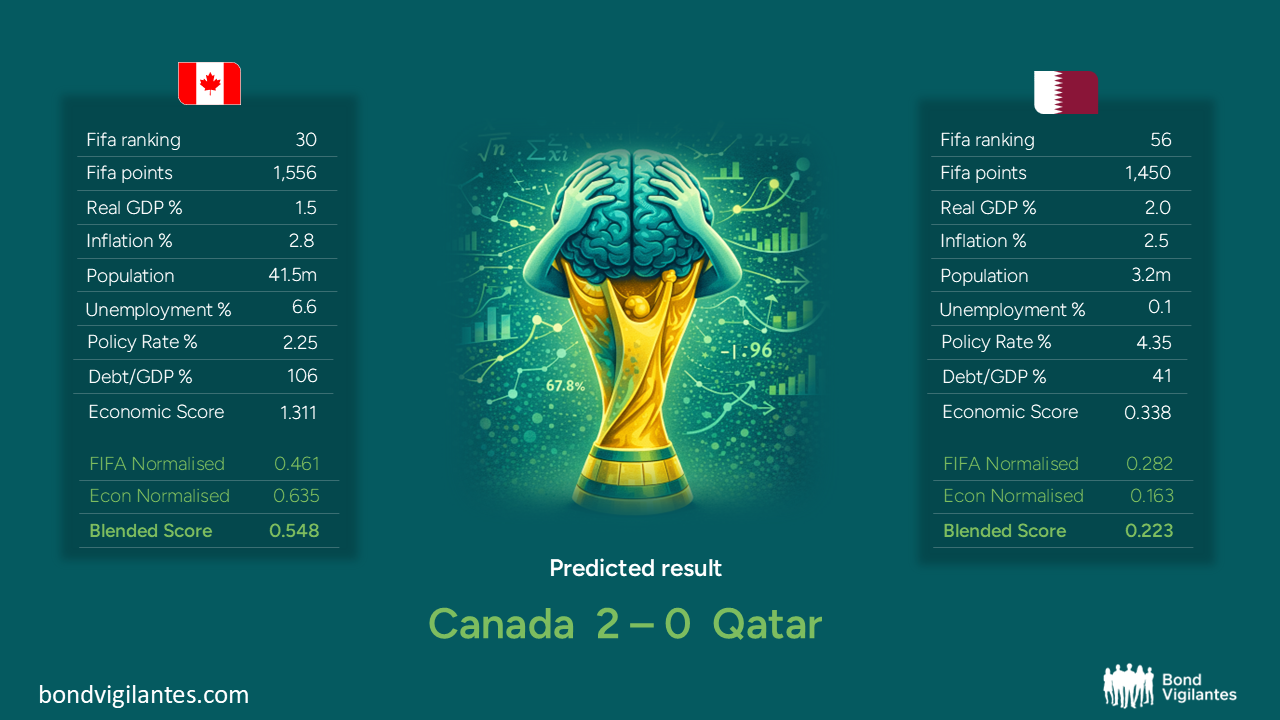

First up, it’s Canada vs Qatar.

Starting with Canada, its James Hathaway, Fixed Income Emerging Market Dealer:

Canada has made only 3 appearances at world cups: 1986, 2022 and this year as co-host. Can they add to their, arguably disappointing, opening points against Bosnia this evening, and make the case for their football team being as strong, stable and steady as their bond market?

Canada is rock solid. They have been the poster child for inflation targeting since bringing this in back in 1991. As a result inflation has tracked at roughly 2% since. The Bank of Canada have been balance and effective throughout many market crises. Although they do issue a whole yield curve in Canadian dollar, they do only really issue 5yr USD bonds. Canada is a net exporter, especially during times of energy shock. However, structurally weaker growth makes them US dependent. Therefore, oil shocks hurt consumption more than it helps exports. This has meant US policy can upset the relations significantly weakening exports in the face of US tariffs, for example. Canada is really levered on the US industrial and trade policy and therefore, although commodity linked, is at the mercy of the US.

All of this adds some intrigue to a potential meeting with the US in the round of 16, which could occur if Canada finish 2nd in Group B and the US finish 1st in Group D, and both teams win their knock-out round of 32 match. On the evidence from the opening round, maybe that is a plausible path.

Just like the domestic moose: strong, stable and steady, Canada is a lower growth, commodity-linked, developed market with strong fundamentals but clear structural constraints. How will this translate to the pitch?

Up against Qatar, with commentary from Purvi Harlalka, EM Sovereign Analyst and Nick Smallwood, EMD Fund Manager:

Qatar was the smallest country ever to host the FIFA World Cup (2022) and the first Arab one to do so. Although their debut 2022 campaign disappointed as they lost all their Group games and the country has now been badly hit by the Iran conflict, the Qatari economy went into the conflict on a strong footing and is likely to be a story of rebounds. Real GDP is projected to contract sharply in 2026, by 8.6 percent year-on-year, driven by a significant decline in hydrocarbon output and broader trade disruptions. But the rebound in 2027 is expected to be strong with >8% GDP growth driven by North Field LNG expansion. Similarly, the budget will also take a hit, with the deficit widening to 4% in 2026, from 1% in 2025 but return to surpluses by 2030 as LNG production increases (O&G is 80% of government revenues). Given their vast amounts of wealth (sovereign assets are an estimated 230% of GDP), they will simply pick themselves up and carry on building again when the dust settles. The football team will doubtless enter the tournament with the same mentality, as their Group containing fellow fiscal behemoths Switzerland and Canada as well as Bosnia-Herzegovina looks significantly less challenging than what they faced in 2022 (Netherlands, Senegal and Ecuador). As the nation rebuilds, its people will be hoping that their team can similarly bounce back from 2022 to record their first-ever World Cup win this time around.

17 June

A good recovery from the model, predicting the direction of all four games last night, bringing the running total to 13 correct out of 20.

Now, onto the big one…

Bringing you commentary for England, it’s Miles Tym, Sovereign Bond Fund Manager:

Optimistic forecasts as usual. Previous attempts have been more inflated than the underlying growth picture has justified. England will be hoping that new leadership will be able to translate success at club level into glory on the national stage. On paper, the England players should be able to yield more than most international comparators but winning a World Cup may prove to be much more of a challenge than pockets of regional success.

The previous manager introduced stringent training rules for success in penalty shoot-outs. Whilst this has been partially successful in helping England through some tight situations, something much bolder and more creative will be required for a true turnaround on this global stage.

England have an array of talented players, who have demonstrated an ability to develop and improve as a result of learning from overseas alliances. Whilst this is a durable base from which to build a truly world class team, its benefits are frequently overlooked by the wider fan base.

If the team succumb to further big tournament mishaps the fans will call for reform.

And for Croatia, it’s Stefen Isaacs, Co-Head of Macro Fixed Income

Croatia, a nation that emerged in the early 1990s with plenty to prove, has spent the past three decades punching above its weight – on both the pitch and the balance sheet. Its World Cup debut in 1998 saw them reach the semis, and rather than fading into folklore, that set a pattern: a final in 2018 and another semi-final in 2022. For a country of under four million, reaching the semi-finals in roughly half its appearances is nothing short of remarkable.

The same uneven-but-upward arc has played out economically. After a volatile post-independence period, Croatia has gradually converged towards Europe’s core, building credibility through institutional integration and fiscal discipline. It hasn’t been linear – much like their group-stage exits in the 2000s – but the direction of travel is clear: a small, constrained system learning to maximise efficiency under pressure. Croatia rarely dominates, either in macro or footballing terms; it endures, adapts, and tends to show its best when conditions tighten.

Heading into the current World Cup cycle, that identity remains intact. Croatia is once again the side no one relishes facing. Back in 2018, when Croatia beat England 2–1 in Moscow, the former was paying roughly 2.7% for 10-year money, over 100bps wider than the UK. Fast forward to today, and Croatia funds more than 100bps inside it. With the UK’s recent penchant for own goals, Croatian fans may be travelling to Dallas quietly confident.

16 June

A tough evening for the model, failing to call any of the four draws. Though we are confident that not many expected Cape Verde to hold on against the defending European champions for 90 minutes.

Let’s see what the next round of fixtures brings and in particular, Argentina vs Algeria, with commentary below.

As always, all predictions are shared at the bottom of the blog.

Check in tomorrow for our write-up on England vs Croatia.

Writing about the above match-up it’s Carlos Carranza, EMD Fund Manager:

ChatGPT, Co-pilot, and Jean “Claude” Van damme have all done a poor job at explaining a strong correlation between Argentina’s football results and fiscal dynamics. But correlation must be unequivocally above 100%, because bond pricestripled (3x!) since Argentina won its 3rd world cup (3x!). If we think about it, there is nothing easier than finding a strong correlation between Empanadas and Balance of payments: They are both amazing. Of course, the problem for Argentina is that inflation is running only 5-years below Messi. And while the best player in the world is aging at a pace of one year per year (no PhD in Physics required for that calculation), inflation remaining at a sticky 33% doesn’t sound equally glamorous. Finally, if Gemini fails to find a strong correlation between football and fiscal, then it’s time to try Sagittarius or Capricorn, because the stars are aligned.

Meanwhile, Algeria has nothing but upside from here. The Algerians are back at the world cup after 12-years without participating. They do face a tough group: Argentina (primary surplus..), Jordan (primary surplus..), and Austria (GDP recovery in 2026). Interestingly, Mohamed Amoura was the top scorer in African qualifying with 10 goals, which naturally implies one goal per percentage point in the Government’s fiscal deficit. And yes, that deficit is projected at a punchy 10% of GDP for 2026, according to data from the International Monetary Footballers (IMF). Just like with inflation, expectations need to be managed carefully in this game. For both central bankers and Coaches, an Argentina vs. Algeria surprise would be an even bigger headache than the post COVID inflation spike.

15 June

12 games, 9 correct results, 3 exact scores (see the detailed results at the bottom of the blog).

An impressive prediction of Brazil 1-1 Morocco, and a (surprise?) predicted win for Australia vs Turkey were the highlights over the weekend, with Bosnia and Qatar being more resilient than the model accounted for.

Onto this evening’s games, with our focus on Saudi Arabia vs Uruguay.

Writing about Saudi, we have Purvi Harlalka, EM Sovereign Analyst:

Pop Quiz: What do President Trump and Saudi Arabia have in common? Answer: They are both the winners of controversial FIFA prizes! In the case of Trump, FIFA created and then awarded him the inaugural FIFA peace award (who needs the Nobel?). Meanwhile, FIFA’s gift to Saudi was rather more football-centric – the ability to host the 2034 World Cup – yet one that also required considerable creativity to birth. Still, to be fair to the Saudis, the attempt to land the 2034 World Cup should be seen in the context of a broader diversification strategy (tourism) to move the economy away from its dependence on oil alone. They have been hard at work on this agenda called Vision 2030, an ambitious trillion-dollar initiative to transform its economy and society that has seen the share of Saudi’s non-oil economy grow from 45% to 55% in the last decade. Correspondingly, Saudi is on track to see non-oil revenues contribute the same amount as oil revenues to government coffers by 2030 vs. 33% in 2022. The improvement in business environment is also tangible. The 5x rise in foreign direct investment to USD35.5bn in 2025, relative to 2017, is testament to this. Social indicators also showed notable improvements. Homeownership climbed to 66.2%, compared with 47% in 2016, while women’s share in the labour market has risen to 35% from 21% over the same timeframe. At the same time, notwithstanding the flood of Saudi government and GRE issuance in 2025 (USD 38bn) and 2026 (USD 15.5bn in 1Q26), public debt is low (32% of GDP). Mindful of this rising dependence on capital markets, the Saudis have been re-calibrating the 2026-2030 stretch of their Vision 2030 strategy by allocating capital more selectively (Neom’s flagship development, “The Line”, has been suspended). To this end, they have also managed to get themselves included in the JP Morgan Local Currency EM bond index starting 2027, meaning that funds that are benchmarked to it will be forced financiers of the Vision starting next year. Over the last decade, if the Kingdom has proven one thing, it is that size matters, not just in terms of economic heft, but also quite literally, in geographic terms. The fact that its land area spans two seas has allowed it to divert oil flows from one to the other during the ongoing war with Iran. In this, it has come out a relative winner amongst its GCC peers. Whether the economic improvements can be migrated to the football pitch is an open question. Here, the stats are not in their favour. Outside of their stunning 2-1 win over Argentina at the 2022 World Cup – the Argentines’ only defeat in a tournament they would go on to win – there has been very little to shout about. In fact, the Green Falcons have lost 68% of their World Cup matches (13 of 19), the highest loss rate of any nation to have played 15 or more games at the tournament. They might need a little help from Lady Luck.

And for their opponents, Uruguay, it’s Carlos Carranza, EMD Fund Manager:

Uruguay: Exporter of high-quality beef, and some wilder beasts like Federico Valverde. The first FIFA World Cup was hosted by Uruguay in 1930, where Uruguay won the tournament, beating Argentina 4–2 in the final (Argentinians still resent that game even though there is probably no one still alive who remembers it). Their football and their macroeconomics share a strong parallelism: Small economy with very strong macro and football results. Their local football league is super small…just like their fiscal deficit. Their balance of payments is well balanced: They export billions of dollars’ worth of high-quality beef and some wilder beasts with pure talent, such as Luis Suárez, Edinson Cavani, and Federico Valverde. The first two are not playing in this cup as they retired from football after aging like a fine Tannat. Meanwhile, the latter is ready to take on some amazing games. Valverde is known as an elite stamina player, constantly moving between defence and attack. Just like the Central Bank, which is certainly an elite player in the EM inflationary world, especially when it comes to policy credibility and independence. Vamos La Celeste!

12 June

Well, perhaps we are on to something here with calling the first two games perfectly.

However, it’s early days and important to separate the signal from the noise. Let’s see how the model does over the weekend. Below are some more predictions alongside narrative from our bond specialists.

We have included a full set of predictions at the bottom of the blog.

First up, it’s the USA vs Paraguay this evening.

From Ben Lord, Macro Fixed Income Fund Manager:

The US is currently ranked as 3rd favourite to win the world cup in the Bond Vigilantes model, but this surely reflects the size of its population more than any footballing prowess. That being said, the US remains today the largest economy in the world, and the story of 2026 so far has been one of continued resilience and even possible reacceleration. Could economic dominance and momentum in 2026 carry over into football? It seems unlikely, based on history.

Were the US to finish 3rd, this would match its best ever result in the tournament, when it was beaten by Argentina in the semi-finals (there must have been different rules back then). This result though occurred almost 100 years ago, in 1930: if the US does well, alarm bells should start ringing about another Great Depression. The last time the US hosted the world cup was in 1994, and they performed well, making it into the last 16 where they were beaten 1-0 by the eventual winners, Brazil.

But whilst the US has been the largest economy in the world for well over 100 years, there are surely changes afoot today? In PPP terms, China has already overtaken the US as the largest economy, although in dollar terms China is expected to overtake the US in the 2030s. However, this will depend on USD/RMB. Talking solely of the USD, there are clear warning signs ahead. The US has long had the largest capital markets in the world, but it now also has the largest amount of government debt outstanding in the world (in USD terms) and by some margin. Furthermore, this margin is growing. The deficit is growing, and demographics clearly suggest that the deficit is going to start to grow even faster in the next decades, simply because spending is drastically outpacing revenues.

With the world’s reserve currency, and a steady, democratic and multilateral world order view, this growing deficit and debt pile has been manageable for many years. However, with new, unpredictable, unilateral, autocratic and volatile leadership, all of these post WW2 US economic traits are at risk of significant change. The US team comes into this world cup with a large population suggesting a strong team, and an economy with 5% or more nominal GDP growth that is the envy of most of the developed world. Whilst Gianni Infantino and FIFA may view Trump as a pacifying force on the world stage I bet even the US team are delighted to be playing this tournament at home; imagine the hostile reaction they would get anywhere else!

And their opponents Paraguay, with commentary from Carlos Carranza, EMD Fund Manager:

Disciplined fiscals… disciplined football. If this game were played on macro credibility rather than the pitch, Paraguay would come in looking exceptionally solid: on the field, they are defined by a structured, physical, and hard‑to‑break‑down system, conceding just 10 goals in 18 qualifying games, which is a pretty good score, and a reflection of patience and collective discipline. In macro…the story is strikingly similar, with consistently tight fiscal management delivering sovereign upgrades from S&P and Moody’s, a positive outlook from Fitch, and a clear trajectory toward Investment Grade in the near term. In both arenas, Paraguay plays a low‑volatility, high‑discipline game, so if they approach this match the same way they have managed their economy, they’ll put themselves in a strong position to win (world cup surprise?).

Then taking you through the weekend, we have selected the following three fixtures.

Qatar vs Switzerland

For Qatar, we have Purvi Harlalka, EM Sovereign Analyst and Nick Smallwood, EMD Fund Manager:

Qatar was the smallest country ever to host the FIFA World Cup (2022) and the first Arab one to do so. Although their debut 2022 campaign disappointed as they lost all their Group games and the country has now been badly hit by the Iran conflict, the Qatari economy went into the conflict on a strong footing and is likely to be a story of rebounds. Real GDP is projected to contract sharply in 2026, by 8.6 percent year-on-year, driven by a significant decline in hydrocarbon output and broader trade disruptions. But the rebound in 2027 is expected to be strong with >8% GDP growth driven by North Field LNG expansion. Similarly, the budget will also take a hit, with the deficit widening to 4% in 2026, from 1% in 2025 but return to surpluses by 2030 as LNG production increases (O&G is 80% of government revenues). Given their vast amounts of wealth (sovereign assets are an estimated 230% of GDP), they will simply pick themselves up and carry on building again when the dust settles. The football team will doubtless enter the tournament with the same mentality, as their Group containing fellow fiscal behemoths Switzerland and Canada as well as Bosnia-Herzegovina looks significantly less challenging than what they faced in 2022 (Netherlands, Senegal and Ecuador). As the nation rebuilds, its people will be hoping that their team can similarly bounce back from 2022 to record their first-ever World Cup win this time around.

And for Switzerland, it’s Anjulie Rusius, Macro Fixed Income Fund Manager:

If you’re looking for a footballing fun-do, Switzerland’s unlikely to cause a stir, but big cheeses they serve a-plenty. Swapping your Emmental for Embolo and raclette for Rodriguez – this may well be a team to watch; though sadly not possible on your Rolex, Omega or TAGs!

A smart-watch would instead be goalkeeper Kobel, as one of the best in Europe, he’s considered a safe pair of hands. Not unlike the nation’s currency, where the Swiss-Franc has long been regarded a “safe haven”. Indeed, in Q1 2026, CHF reached its strongest level in over a decade against both the EUR and USD, driven by investors seeking alternatives to the latter. Despite paring back a tad since, the ongoing geopolitical stress from the Iran war has continued to generate safe-haven inflows into the currency.

The fly in the fondue is potentially however the Swiss National Bank. Independent and cautious, this central bank is ready to move mountains. With President Schlegel asserting the SNB has “unrestricted room for manoeuvre” on both rates and FX interventions, the SNB stand ready to sell francs to cap appreciation. Goalkeeping at its finest.

Will the football squad prove as nimble as the bank? With rates held at zero for a year now and inflation running at the lower end of the 0-2% CPI target range (interestingly, Swiss inflation is the lowest of all competing nations), the SNB is cautiously doing its job – neither over or undershooting targets, unlike many of its peers. The Swiss continue to hit their goal. Solid, like its chocolate. Indeed, should Swiss football fail to impress, I for one will be comfort bingeing on its Lindt and Toblerone exports instead.

Australia vs Turkey

For Australia, we have Eva Sun-Wai, Global Macro Fund Manager:

Australia’s World Cup record mirrors its macro story: rarely among the pre-tournament favourites, but usually still around when things get interesting, having reached the round of 16 a handful of times (fun fact: that disguises a long absence, failing to qualify for 32 years between 1974 and 2006).

Markets have spent much of the past year debating whether restrictive monetary policy would finally bring the economy to heel, only to discover that a combination of resilient employment, sticky core inflation and commodity exports remains surprisingly difficult to tackle. Fundamentals remain strong: unemployment has held around 4%, Australia retains a AAA sovereign rating and government debt sits at roughly a half of GDP. Yet Australian government bonds yield more than US Treasuries (and this has widened as the RBA has been responsive to inflation and hiked 3 consecutive times) – feels a bit like a team that keeps qualifying but is priced like an outsider. Not as perplexing as them still being in Eurovision though (P.S. Delta Goodrem was excellent).

So they may not win the World Cup, but the bonds seem like a good place to park in an environment where fiscal deterioration could start to steepen curves again. And if all else fails, Australia retains one advantage that football teams rarely enjoy: it can always export more iron ore.

And for Turkey, a comment from Eldar Vakhitov, EM Sovereign Analyst

Turkey will play in the World Cup for the third time in its history – its first appearance dates all the way back to 1954. What truly stands out is the 2002 campaign, when the team came remarkably close to gold medals, losing only narrowly to eventual champions Brazil in the semi-final. Speaking of gold, it’s something the Turkish public has long held in high regard. Gold imports have remained consistently high over the years, and today the metal accounts for nearly two thirds of the central bank’s international reserves.

Back in 2002, Turkey ultimately secured the bronze medals, famously scoring the fastest goal in World Cup history – just 11 seconds into the third place match against South Korea. Investors could only wish Turkish inflation slowed at such speed, but unfortunately the process has been far more drawn out. Nevertheless, the country’s policy framework has improved notably in recent years, mirroring the national team’s own progress. While most macroeconomic indicators are weaker compared to its group rivals, this should not prevent the football squad from performing well in the group stage. Matching the spectacular 2002 campaign would be quite a challenge, but with several standout players in midfield and attack, qualifying into the play-offs at least seems well within reach.

Ivory Coast vs Ecuador

Ivory Coast commentary provided by Purvi Harlalka, EM Sovereign Analyst and Nick Smallwood, EMD Fund Manager

Fun Fact: Ivory Coast’s football team is nicknamed the Elephants due to the country’s long association with the animal. Back at a World Cup for the first time in 12 years, the Elephants are tipped to be dark horses. However, there is nothing dark about the country’s economic performance, which has been consistently impressive. Over the last decade (2016–2026), Ivory Coast (Côte d’Ivoire) has sustained one of the fastest and most resilient economic expansions in Sub-Saharan Africa, achieving an average annual real GDP growth rate of approximately 6.5% to 7.0%. This is in large part thanks to prudent policy making, a business-friendly regime, and a disciplined expansion of the supply side via investment in infrastructure that has kept inflation (2.5-3.5% in the last decade) and fiscal deficits contained. More recently, they have benefitted from the gold price rally that has lifted their current account from -7.7% of GDP in 2022 to -2.9% of GDP at end 2025. A few more years on this trajectory and Ivory Coast will be one of the few African sovereigns to join the Investment Grade club (it is currently two notches below). Their football team has a good chance of moving in the same direction. While they have never progressed past the Group stages in any of the three World Cups in which they participated (2006, 2010 and 2014), this can largely be ascribed to very tough groups and bad luck (a single goal against Portugal would have seen them move to the knockout stages in 2010). With an easier Group this time – they face Ecuador, Germany and Curacao – and a more generous path to the second round, Ivory Coast’s chances of improving their footballing record are as bright as their economic prospects.

And for Ecuador, Charles de Quinsonas, Head of EMD, says:

In 1999, Ecuador became the first country to default on its Brady bond. That took them away from American football into their first participation to the FIFA World Cup in 2002. Since then, they defaulted twice on their bonds. Once in 2008, the so-called “strategic” default when President Correa declared the bonds illegitimate and refused to pay despite having the ability to do so. The second default was in 2020 during COVID and a low oil price environment.

This year will mark the country’s fifth participation in the World Cup and their group-stage competitors Germany, Ivory Coast and Curacao should know that Ecuador have won at least one match in each World Cup they’ve played. The squad is known for its defensive quality with defenders playing for Paris Saint-Germain and Arsenal, and a midfielder from Chelsea. Will that be enough to advance past the group stage against almighty Germany and improving credit story Ivory Coast? After all, Ecuador’s President Noboa’s biggest fan in the US is Donald Trump and the past year’s taught bond investors that it paid off to bet on Ecuador. Fiscal consolidation, a performing economy, and a recent tailwind of oil revenues (helped by the cut of diesel subsidies) have led the country’s 10yr $ bonds to trade from >15% a year ago to now yielding just over 8%. That’s the Ecuador paradox: the country sits at a geographic zero-point but is a place where extremes define the narrative.

11 June

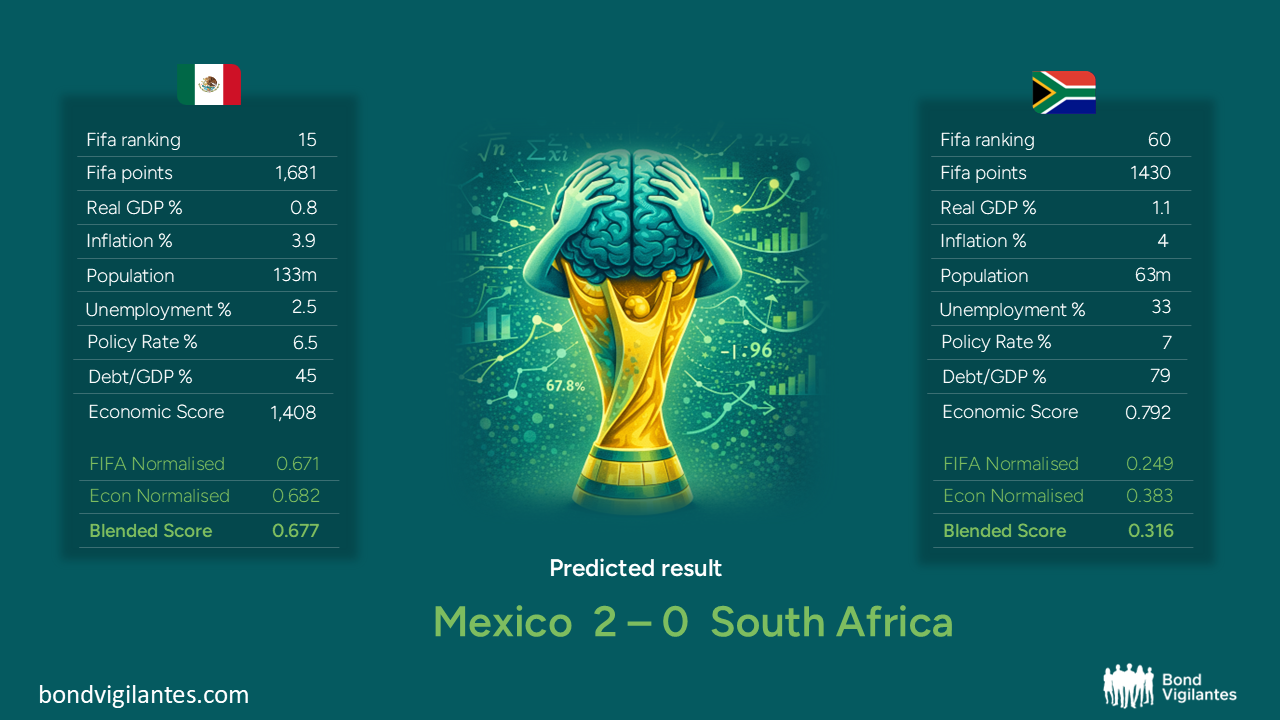

First up is the opening game, Mexico vs South Africa.

Carlos Carranza, Emerging Market Debt Portfolio Manager says:

Well…if South Africa manages to play the same way it has managed its fiscal dynamics, then Mexico should brace for impact, because that staggering narrowing in the deficit has been a goleada all along.

But make no mistake, Mexico is still a “futbol IG” and they are going to put up a great battle. El tricolor has very strong institutions: like Banxico or Guillermo Ochoa. Neither of them will ever drop the ball. Literally.

Both in politics and futbol….South Africa doesn’t do superstars. They’re more like a well-diversified portfolio, resilient and surprisingly effective when combined. Don’t forget the ANC lost its majority in 2024 and then entered into the ultimate football-finance strategy: GNU = “Goals Need Unity!!”

Our model predicts this one to come out as 2-0 to the hosts, though I think there is scope for a 1-1 here. Mexico will attack…but SA will tighten the spreads. I am inflating my expectations…because it’s not just a match…it’s an EM rally.

Following that, it’s South Korea vs Czechia.

Eva Sun-Wai, Global Macro Portfolio Manager says:

South Korea arrives at the World Cup with a profile familiar to investors: strong fundamentals, plenty of volatility and absolutely no consensus on the right narrative. Equity markets have swung between AI euphoria and sharp sell-offs, higher oil prices have nudged inflation forecasts higher, and the KRW continues to command more attention than most central banks would prefer. Yet semiconductor exports are growing at 169% YoY, total exports have recorded their strongest growth since 1984, and the Bank of Korea has upgraded its 2026 growth forecast to 2.6% from 2.0%.

The result is a reaction function that would give most football managers a headache. Inflation says one thing, growth says another, the KRW occasionally demands an emergency intervention, and then the AI supply chain turns up and changes the scoreline. It is perhaps telling that the BOK’s policy discussions increasingly span inflation, growth, financial stability and the exchange rate simultaneously.

Meanwhile, S Korea finds itself in familiar territory: good enough to compete for qualification, but still trying to prove it belongs among the elite. Korea Treasury Bonds are entering the FTSE World Government Bond Index, with estimates of roughly USD52bn of inflows, while the longer-running pursuit of developed-market status continues. Much like Korea’s famous 2002 run to the semi-finals, everyone agrees it was an impressive achievement; the debate is whether it was a stepping stone to something bigger or simply a very memorable tournament.

Eldar Vakhitov, Emerging Markets Sovereign Analyst with our commentary for Czechia.

Czechia is set to appear in the World Cup for only the second time as an independent nation, following the breakup of Czechoslovakia in 1992. Their previous appearance was in 2006, when the tournament was hosted by neighbouring Germany, their main trading partner. Even then, they failed to progress to the knockout stage. Meanwhile, Czechia’s GDP per capita has climbed to 71% of the euro area average in 2026, up from just 45% in 2006. Whether this impressive performance can be mirrored in a stronger showing at this World Cup remains to be seen. This improvement is one of the key reasons the IMF now classifies Czechia – along with group rival South Korea – as an advanced economy. The question is whether much better macroeconomic and institutional foundations will help them outperform the “true” emerging market countries in their group, Mexico and South Africa.

Czechia has long maintained prudent fiscal policies and keeps government debt relatively low, with almost all of it denominated in its own currency – this significantly limits its reliance on foreign financing. On the pitch, however, the national team will depend heavily on its star players based in foreign clubs to make an impact. Meanwhile, the Czech central bank is considered one of the most disciplined across emerging markets, fiercely guarding its inflation targeting credibility. Those same qualities – discipline, consistency, and cautious approach – may be exactly what the football team needs if it hopes to reach the knockout stage this time.

Summary of all predictions (updated 26 June)

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.