The Korea conundrum: when strong fundamentals meet weak market pricing

A market priced for stress, not strength. Korea is one of the clearer beneficiaries of the global AI investment cycle. Its equity market has reflected that. Its currency and government bond markets have not.

Few markets today present as striking a disconnect between macro fundamentals and market pricing as Korea. While the country has emerged as one of the biggest beneficiaries of the global AI boom, the Korean won (KRW) and Korean Treasury Bonds (KTBs) have been among the weakest performers globally.

Since the start of 2025, the KOSPI has surged 262%, making it the world’s best-performing equity market. By comparison, Taiwan has gained 106%, while the NASDAQ CTA AI Index has risen 86%1

This equity rally has coincided with a much stronger economic backdrop. Booming semiconductor exports drove Korea’s current account surplus to a record USD123 billion, or 6.5% of GDP in 2025, with another record surplus expected this year as global AI-driven chip demand remains robust.

Although the K-shaped divergence between technology and non-technology sectors persists, the strength of the semiconductor industry has more than offset weakness elsewhere. Rising household incomes and wealth effects are also expected to lift GDP growth to around 2.7% in 20262, above Korea’s long-term trend.

The stronger growth backdrop has also improved public finances. Higher tax revenues enabled the government to finance this year’s KRW26.2 trillion supplementary budget—targeted at easing household energy costs and strengthening supply chains—without issuing additional KTBs. The managed fiscal deficit is now projected to narrow from 3.9% of GDP in 2025 to 3.1% in 20263. The fiscal deficit is expected to narrow further in 2027, a meaningful improvement from the government’s earlier mid-term projection of around 4%.

And yet the market has priced a very different story.

Source: Bloomberg, M&G, June 2026; Tech sectors represented by South Korea’s Information and Communication Technology (ICT) sector, published by Ministry of Trade, Industry and Resources

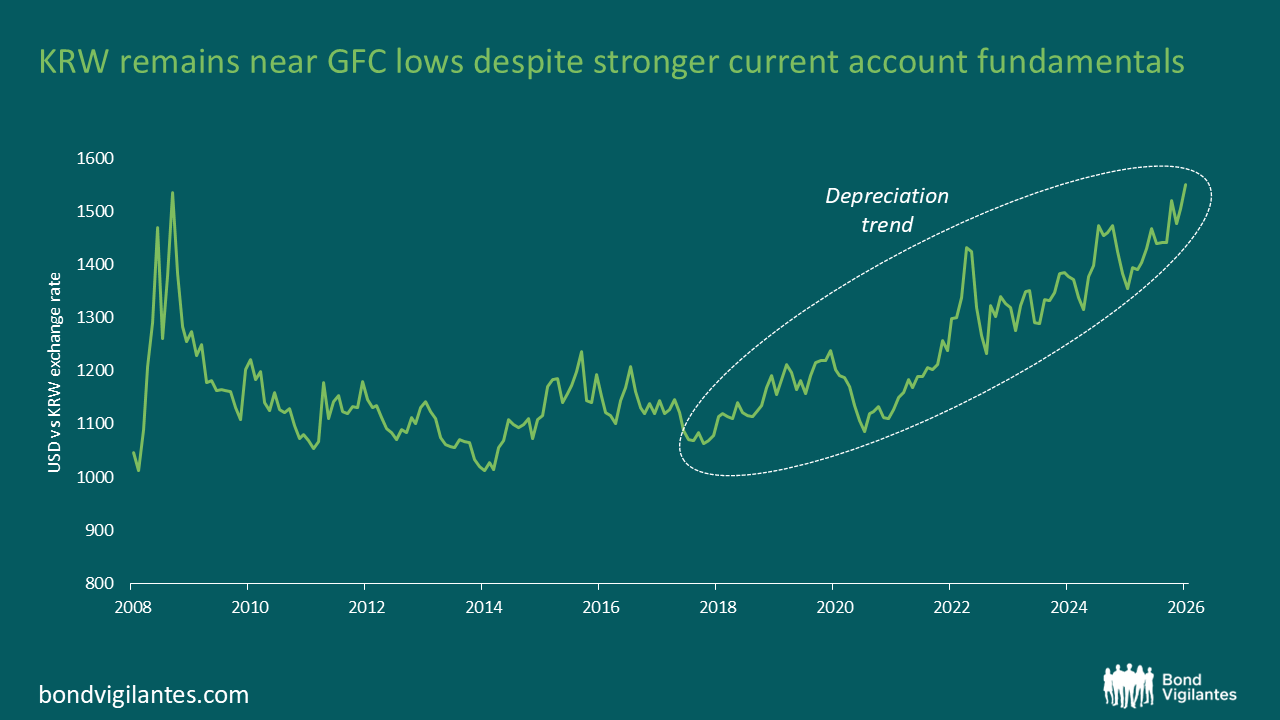

Despite these supportive fundamentals, the KRW has remained one of the weakest currencies across both developed and emerging markets, depreciating 12.6% against the US dollar over the last twelve months, as at end-June 2026. At current levels, the won has returned to lows last seen in 2009 despite a significantly stronger external position today.

The bond market has displayed a similar disconnect. KTBs have been the worst-performing local currency bond market in Asia since mid-2025 despite expectations of improved fiscal health. Since end-June 2025, the iBoxx ALBI Korea Index has declined 10% in local currency terms.

That is the Korea conundrum: the macro story has improved, but market pricing has deteriorated. In our view, the gap is becoming increasingly difficult to justify.

Source: Bloomberg, M&G June, 2026

How did this happen?

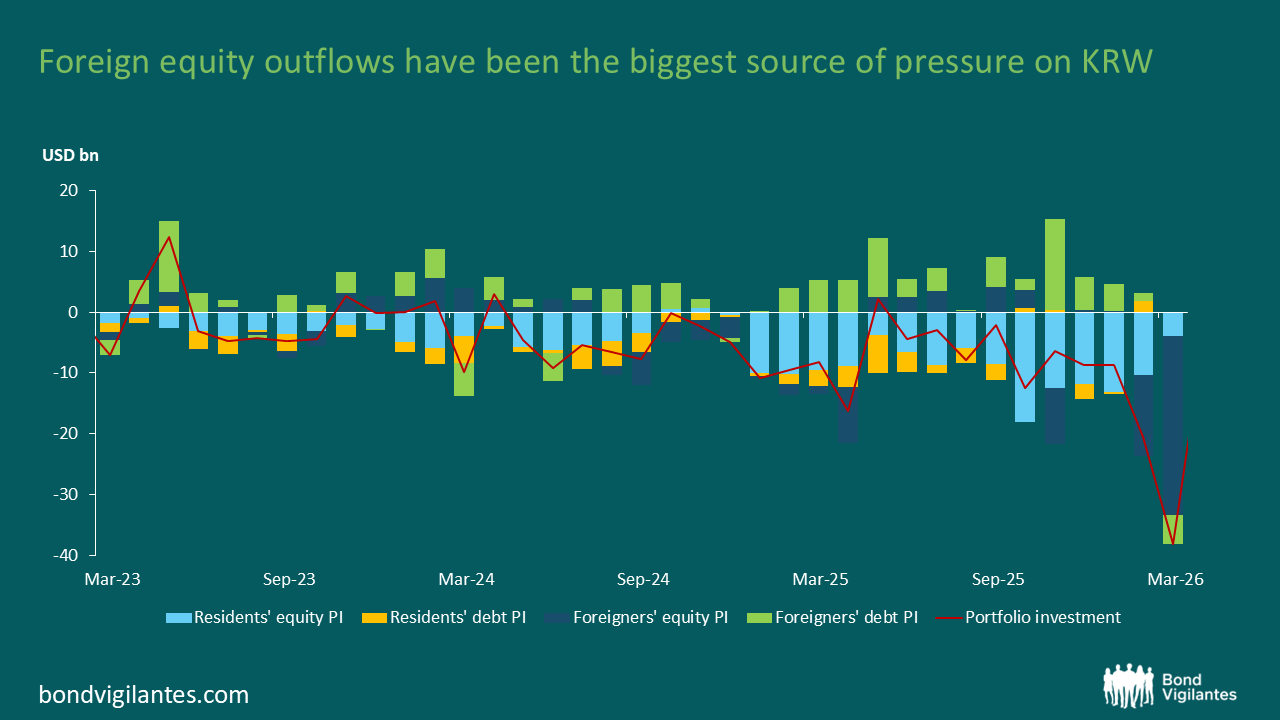

For the KRW, the divergence has largely been driven by capital flows overwhelming macro fundamentals.

The answer lies less in Korea’s macro data than in its capital flows. Semiconductor exports have been strong and Korea’s external surplus has widened. But those positives have been overwhelmed by equity-related outflows, overseas allocation by domestic investors and limited conversion of export receipts back into won.

As domestic equities rallied, Korean institutional and retail investors continued allocating capital overseas. At the same time, foreign investors became significant sellers of Korean equities, driven by profit-taking and portfolio rebalancing. Approximately USD100 billion has flowed out of Korean equities over the last 12 months, with the bulk of the outflows driven by Samsung Electronics and SK Hynix, which together account for half of the KOSPI’s market capitalisation.

Other flow dynamics also weighed on the won. Exporters converted a relatively small proportion of their US dollar receipts into KRW, while net foreign direct investments remained in negative territory. These outflows largely offset the positive impact of Korea’s record current account surplus and continued foreign demand for government bonds.

Source: Haver Analytics, Barclays Research, 2026

The KTB sell-off reflected a different set of drivers. Markets progressively priced out policy easing as household debt accelerated, the housing market recovered and KRW weakness complicated the inflation outlook. Into 2026, inflation concerns—initially triggered by the US-Iran conflict and subsequently reinforced by stronger-than-expected domestic growth—led investors to price a much higher policy rate path.

In other words, both the currency and bond market have weakened for understandable reasons. The question now is whether those reasons are still strong enough to justify the scale of the repricing.

Is the tide starting to turn?

The persistence of this disconnect raises an important question: can the underperformance of the won and domestic bond market continue despite increasingly supportive fundamentals?

Unlike previous episodes of KRW weakness during the Asian Financial Crisis and Global Financial Crisis, Korea is not experiencing a foreign currency funding crisis. US dollar liquidity remains ample, reflected in narrower cross-currency swap spreads, while Korea remains a net external creditor with substantial foreign exchange reserves accumulated over the past two decades.

That distinction matters. The won has been weak, but Korea is not facing the kind of external funding stress that marked earlier crisis periods.

Nevertheless, prolonged KRW weakness could complicate monetary policy by increasing imported inflation and funding costs, while further undermining investor confidence. Recognising these risks, policymakers have stepped up efforts to stabilise the currency through verbal intervention, greater FX hedging flexibility for the National Pension Service, reviews of exporters’ FX conversion practices and increased scrutiny of banks’ FX trading activities.

These measures appear to be gaining traction. Exporters have increased US dollar conversions, with Barclays estimating that the exporter USD sales ratio rose to 18.6% in March—the highest level in almost two years—while importers’ USD demand moderated.

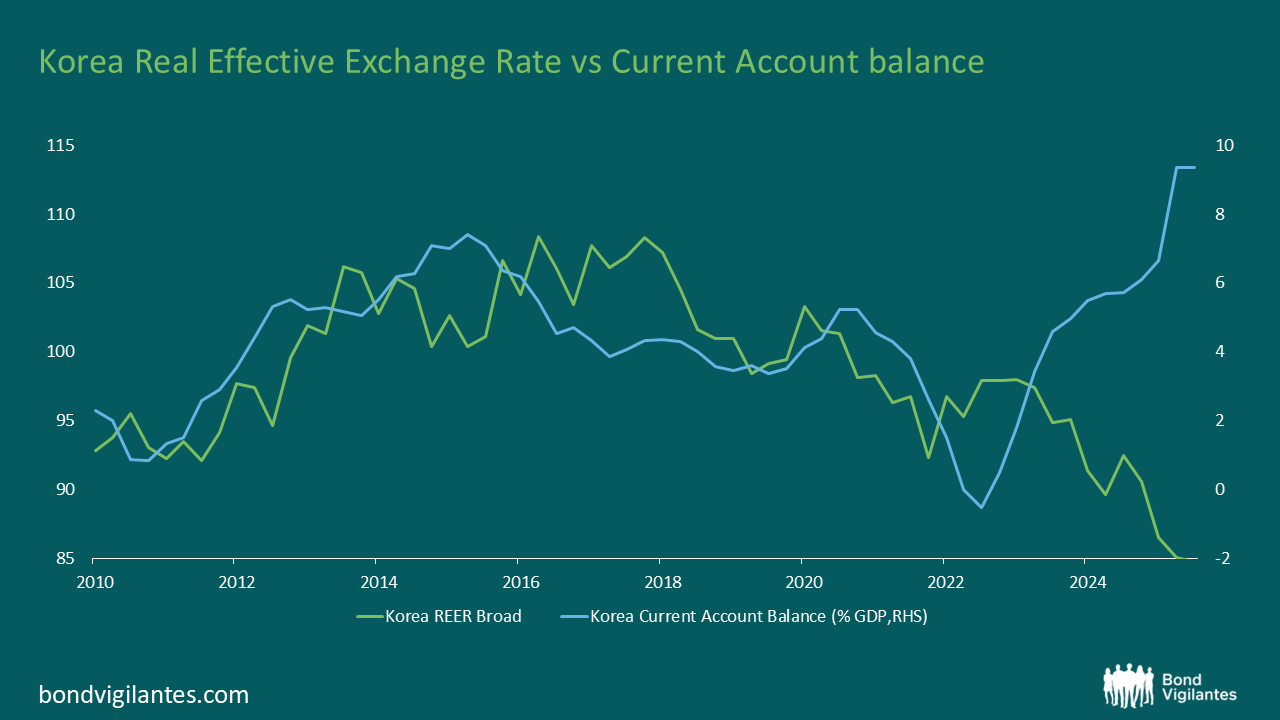

Meanwhile, Korea recorded a current account surplus of approximately USD102.7 billion during January-April 2026, with the Bank of Korea projecting a full-year surplus of around USD250 billion4. Although the historical relationship between Korea’s real effective exchange rate and current account surplus has weakened since 2024, sustained external surpluses, together with policy support, should gradually narrow this disconnect.

Source: Bloomberg, M&G, June 2026

Nearer-term corporate flows may also prove supportive. Markets expect a meaningful portion of proceeds from SK Hynix’s planned US ADR listing to be converted into KRW to finance domestic semiconductor investments. In addition, August corporate tax prepayments should generate seasonal demand for the currency, although the magnitude remains difficult to estimate. Longer term, the government’s recently announced mega investment projects, alongside Samsung and SK Hynix, should provide structural support for the currency.

Why KTBs look over-discounted

A more stable currency backdrop should also support the KTB market.

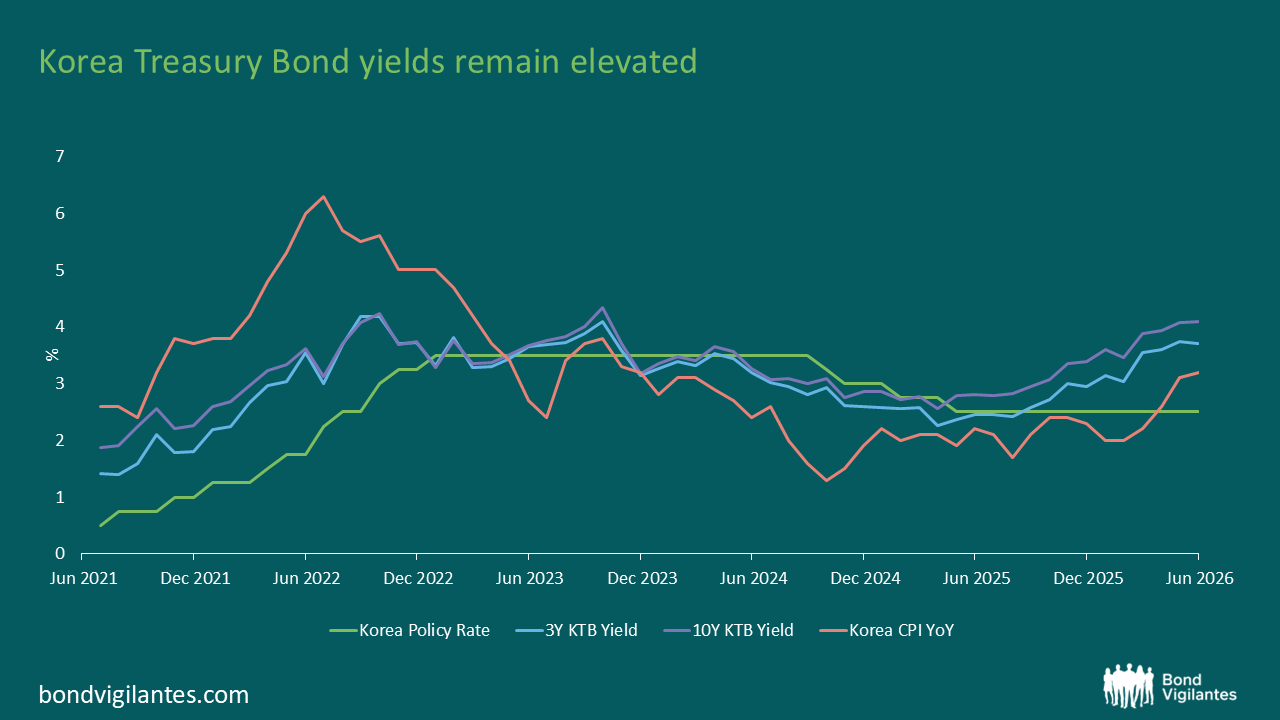

Although inflation risks remain, Korea entered this expansion with relatively subdued price pressures. Even after the recent oil price shock, the Bank of Korea projects headline inflation of 2.7% in 2026—well below the inflation experienced during the 2022 energy crisis. The subsequent decline in oil prices following the US-Iran ceasefire has further strengthened our expectations that inflation could peak around August.

Against this backdrop, we believe the sell-off in KTBs has become excessive. Despite materially lower inflation than in 2022, government bond yields have already returned to levels seen during that period. While producer prices may remain somewhat sticky, both headline and core inflation are expected to peak in August as lower energy prices and favourable base effects feed through.

Current market pricing also appears overly hawkish. We expect the Bank of Korea to deliver three rate hikes during this tightening cycle, whereas markets have priced in four hikes. In addition, KTB inclusion in the FTSE World Government Bond Index is expected to attract approximately USD52 billion of passive inflows over eight months beginning in April 2026, providing an additional source of demand.

Source: Bloomberg, June 2026

While the Bank of Korea’s latest Financial Stability Report highlighted rising household debt and vulnerabilities among SMEs and self-employed borrowers, excessively restrictive financial conditions could themselves become a source of financial instability, limiting the scope for rates to rise as much as markets currently anticipate.

For bond investors, the balance of risks is therefore beginning to look more asymmetric. Inflation and financial stability concerns still matter, but a significant amount of tightening risk is already reflected in KTB pricing.

Where we see value

We believe markets have become overly pessimistic on both the Korean won and Korean rates.

Accordingly, we have become more constructive on both KRW and KTB duration within our Asian local currency bond portfolios. Within the curve, we continue to prefer the belly, while the repricing at the ultra-long end is also creating more selective opportunities.

We acknowledge that near-term headwinds remain, particularly uncertainty surrounding further equity-related outflows. However, we believe the gap between market pricing and macro fundamentals has widened to levels that are difficult to sustain. As capital flow pressures gradually moderate and Korea’s strong external position continues to assert itself, both the won and the domestic bond market should increasingly reprice towards stronger underlying fundamentals.

Korea’s fundamentals and market pricing have moved too far apart. That does not mean the adjustment will be immediate, particularly while equity-related flows remain uncertain. But as capital flow pressures moderate, we believe the won and KTBs should begin to reflect Korea’s stronger underlying fundamentals more clearly.

1Source: Bloomberg, M&G, based on total returns (Including dividends), in respective local currencies between 1 Jan 2025 to 30 June 2026.

2Source: Bloomberg, Economic Forecasts, contributor composites, 3 July 2026.

3Source: CEIC, ADB, IMF, MoSF, HSBC forecasts, June 2026

4Source: Bank of Korea, May 2026

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.