World Cup

The Bond Vigilantes World Cup Model

By Joe Sullivan-Bissett

11 June 2026

Whilst I was listening to Ben Bernanke last night, who announced his decision to reduce the monthly rate of purchases of treasuries and mortgage backed securities by $10 billion per month, it became clear that the time has come to coin a new phrase. With the employment picture improving substantially in the last few months from a very weak point, and with GDP growth moving in a similarly positive direction from a similarly weak point, it is entirely justifiable in my opinion that the Fed continues to provide historically vast quantities of liquidity, albeit at an ever so slightly slower pace. The Fed sees growth returning to between 2.8% and 3.2% for the next couple of years, and it sees unemployment falling to between 5.5 and 5.8% within that horizon. Take a step back, briefly, and you would look at these predictions for the economy and expect the policy rate to be substantially higher than zero. So why did Ben Bernanke spend so long anchoring the market’s expectations for the future path of interest rates, and why is he still creating $75 billion of cash each month?

In the 1970s the more economically developed nations were experiencing an unexpected new phenomenon: low employment and high inflation. This, as we all now know, came to be known as stagflation. Today, the US, and just very recently the UK, is experiencing the opposite: rapidly improving employment and falling inflation. I am going to call this disinfloyment.

Chairman Bernanke said that low inflation is “more than a little concern”. One has to think that it was the improving economic and political picture, as well as perhaps some concern over early bubble formations, that brought about the decision to taper, on the one hand, and the inflation picture that brought about the strengthening forward guidance and lowering and weakening of the unemployment rate ‘knockout’ on the other. Otherwise, given a better broader economic outlook, you would expect a truer normalisation of policy, with the provision of liquidity being stopped and rates being hiked. The concern I think Bernanke has, and the question I would have asked him, would have been “what if zero interest rates, massive liquidity provision, and forward guidance do not manage to generate inflation at or above target? What then Ben?”

If the Fed were to find itself in a position of full employment, acceptable growth, and disinflation, with policy rates and long term interest rates near their extreme floors, and the efficacy of increased liquidity provision being increasingly marginal of benefit, or perhaps worse, then the Fed is alarmingly close to the limits of its powers. Perhaps only helicopter drops would remain a viable tool at this point. It is the awareness of this that I think is framing current Fed action. At 1.5% 10 year treasury yields earlier this year, rapid liquidity provision, and zero interest rates, there was almost nothing the Fed could do to counteract falling inflation; it simply couldn’t add much more stimulus. The utterance of the ‘t’ word in May, and now the first minor reduction in the pace of stimulus last night has seen 10 year yields rise to 3%, and from this point there is scope for data to disappoint to such an extent that yields fall, forward guidance is pushed out further, and QE can be increased so as to stimulate the economy.

So disinfloyment is a state of the economy that policymakers are rightly very scared of, as, depending on the economy’s starting point, it is a state in which economic policy is getting ineffective. But do I actually think that this is a term that we will hear more of in the next couple of years? Probably not.

For disinfloyment to become a problem, the employment picture must continue to improve, and inflation must continue to fall or fail to rise. Whilst I believe the former to be highly likely at this point, I find that latter harder to believe, and the Fed’s projection yesterday was for inflation to return to 1.4% to 1.6% in 2014. Whilst this is clearly still below target, it is less worryingly so than it is today. Bernanke told us yesterday that he presently sees the glide-path for tapering to continue at $10 billion at each meeting, until liquidity provision stops at the end of 2014. I believe that there is a very difficult line for the Fed to tread over the next 12 months. As tapering continues and the markets come to expect the end of the stimulus, long-term yields will rise (as we saw in the Summer) and the economic data risks going in the wrong direction for the tapering to continue. For a gradual rise in rates not to detrimentally affect the recovery, the economy must be growing with such underlying momentum as to shrug off these higher rates: and in this environment, surely inflation would be returning? So: either the Fed finds the recovery to be too fragile to continue tapering, in which case it continues to increase the supply of money each month, thereby risking higher inflation further into the future when the economy improves; or the recovery is sufficiently strong, and inflation (excluding commodities, which the Fed cannot control) is rebounding.

Markets are being staggeringly complacent about inflation at the moment, aided by presently low inflation in the developed world. We would do well to remember that monetary policy since the start of the Great Financial Crash has been designed with one major purpose: to avoid the spiral of deflation witnessed in the 1930s. Deflation, clearly the greater evil of the dichotomy, has been avoided so far. But now developed economies are recovering, liquidity-driven positions are coming back out of commodities and emerging markets, which are pushing down inflation numbers around the world. 2014 will be treading a fine line between these disinflationary forces prevailing, and so monetary policy having to re-start the liquidity machines, and recoveries managing their ways through this transition and finding underlying momentum. Respectively, we either continue to risk higher inflation further in the future through increasing the supply of money, or we start to see it come through sooner than we all presently think: either way, we get inflation. Lest we forget: the Fed will have increased the supply of money by $4.25 trillion at the end of the tapering cycle. When the velocity of money starts rising on top of the increases in money supply, nominal output will start to rise unless the money supply is taken out to an offsetting extent. It is this that I find so unlikely, and it is this that would increase the probability of disinfloyment. In my opinion, we are more likely to get nominal output surprises, and so returning inflation, than anything else in the UK and US. We won’t hear too much, at that stage, about disinlfoyment.

With inflation numbers in the UK moving back towards target and deflationary concerns prevalent in Europe, it is worth asking ourselves whether stubbornly high prices in the UK are a thing of the past. Whilst the possibilities of sterling’s strength continuing into 2014 and of political involvement in the on-going cost of living debate could both put meaningful downside pressure on UK inflation in the short term, I continue to see a greater risk of higher inflation in the longer run.

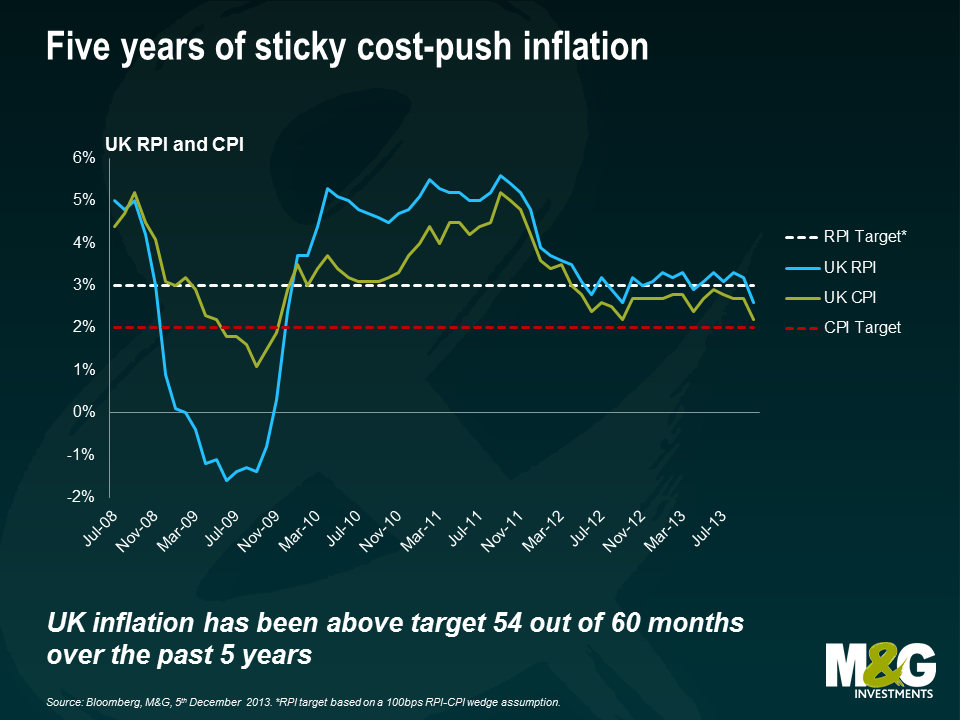

The UK has been somewhat unique amongst developed economies, in that it has experienced a period of remarkably ‘sticky’ inflation despite being embroiled in the deepest recession in living memory. Against an economic backdrop that one might expect to be more often associated with deflation, the Consumer Prices Index (CPI) has remained stubbornly above the Bank of England’s 2% target.

One of the factors behind this apparent inconsistency has been the steady increase in the costs of several key items of household expenditure, together with the recent spike in energy prices which I believe is a trend that is set to continue for many years.

Rising food prices have been another source of inflationary pressure. Although price rises have eased in recent months following this summer’s better crops, I think they will inevitably remain on an upward trend as the global population continues to expand and as global food demands change.

Sterling weakness has also contributed to higher consumer prices. Although sterling has performed strongly in recent months, it should be remembered that the currency has actually lost around 20% against both the euro and the US dollar since 2007. This has meant that the prices of many imported goods, to which the UK consumer remains heavily addicted, have risen quite significantly.

Despite being persistently above target, weak consumer demand has at least helped to keep UK inflation relatively contained in recent years. However, given the surprising strength of the UK’s recovery, I believe we could be about to face a demand shock, to add to the existing pressures coming from higher energy and food costs.

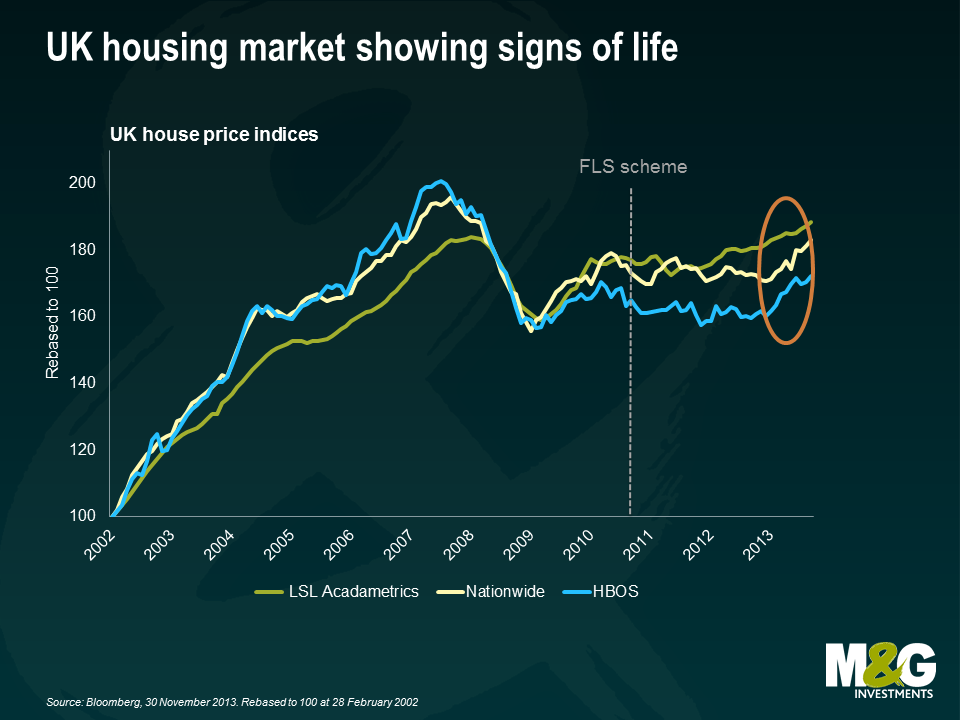

The UK’s economic revival has been more robust than many had anticipated earlier in the year. Third-quarter gross domestic product (GDP) grew at the fastest rate for three years, while October’s purchasing managers’ indices (PMIs) signalled record rates of growth and job creation. Importantly, the all-sector PMI indicated solid growth not just in services – an area where the UK tends to perform well – but also in manufacturing and construction. At the same time, the recent surge in UK house prices is likely to have a further positive impact on consumer confidence, turning this into what I believe will be a sustainable recovery.

Central banks around the world have printed cash to the tune of US$10 trillion since 2007 in a bid to stimulate their ailing economies. This is an unprecedented monetary experiment of which no-one truly understands the long-term consequences. There has been little inflationary impact so far because the money has essentially been hoarded by the banks instead of being lent out to businesses. However, I believe there could be a significant inflationary impact when banks do begin to increase their lending activities. At this point, the transmission mechanism will be on the road to repair, and a rising money velocity will be added to the increased money supply we have borne witness to over the last 5 years. Unless the supply of money is reduced at this point, nominal output will inevitably rise.

Furthermore, I am of the view that new Bank of England governor Mark Carney is more focused than his predecessor was on getting banks to lend. His enthusiasm for schemes such as Funding for Lending (FFL), which provides cheap government loans for banks to lend to businesses, is specifically designed and targeted to fix the transmission mechanism, by encouraging banks to lend and businesses to borrow. The same is true of ‘forward guidance’, whereby the Bank commits to keep interest rates low until certain economic conditions are met.

Perhaps most importantly, I continue to believe the Bank is now primarily motivated by securing growth in the real economy and that policymakers might be prepared to tolerate a period of higher inflation: this is the key tenet to our writings on Central Bank Regime Change in the UK.

With real GDP growth of close to 3% and with inflation above 2% at the moment in the UK, a simple Taylor Rule is going to tell you that rates at 0.5% are too accommodative. But it appears that policymakers are, as we suggest above, happy to risk some temporary overheating to guarantee or sustain this recovery. We believe that this is a factor we are going to have to watch in the coming years, as the market comes to realise that it is much harder to remove easy money policies and tighten interest rates than it was to implement them and cut them.

We witnessed a clear demonstration of this with the infamous non-taper event in September: as the data improved, Bernanke had to consider reducing the rate of monthly bond purchases. However, the combination of improved data and a potential reduction in the rate of purchases saw yields rise; ultimately higher rates saw policymakers state their concerns about what these were doing to the housing market recovery, and so we got the ‘non-taper’. I believe that there are important lessons to be learned from this example, and that policymakers are going to continue to lag the economic recovery to a significant extent.

Despite these risks, index-linked gilts continue to price in only modest levels of UK inflation. UK breakeven rates indicate that the market expects the Retail Prices Index (RPI) – the measure referenced by linkers – to average just 2.7% over the next five years. However, RPI has averaged around 3.7% over the past three years and tends to be somewhat higher than the Consumer Prices Index (CPI). At these levels, I continue to think index-linked gilts appear relatively cheap to conventionals.

Furthermore, this wedge between RPI and CPI could well increase in the coming months due to the inclusion of various housing costs, such as mortgage interest payments, within the calculation of RPI. The Bank of England estimates the long-run wedge to be around 1.3 percentage points, while the Office for Budget Responsibility’s estimates between 1.3 to 1.5 percentage points . If we subtract either of these estimates from the 5-year breakeven rate (2.7%), then index-linked gilts appear to be pricing in very low levels of CPI.

Current inflation levels may seem benign. However, potential demand-side shocks coupled with a build-up in growth momentum and the difficulty of removing the huge wall of money created by QE will pose material risks to inflation in the medium term. Markets have become short-sightedly focused on the near term picture as commodity prices have weakened and inflation expectations have been tamed by the lack of growth. This has created an attractive opportunity for investors willing to take a slightly longer-term view.

A reminder to our readers that the Q4 M&G YouGov Inflation Expectations Survey for the UK, European and Asian economies is due out later this week . The report will be available on the bond vigilantes blog.

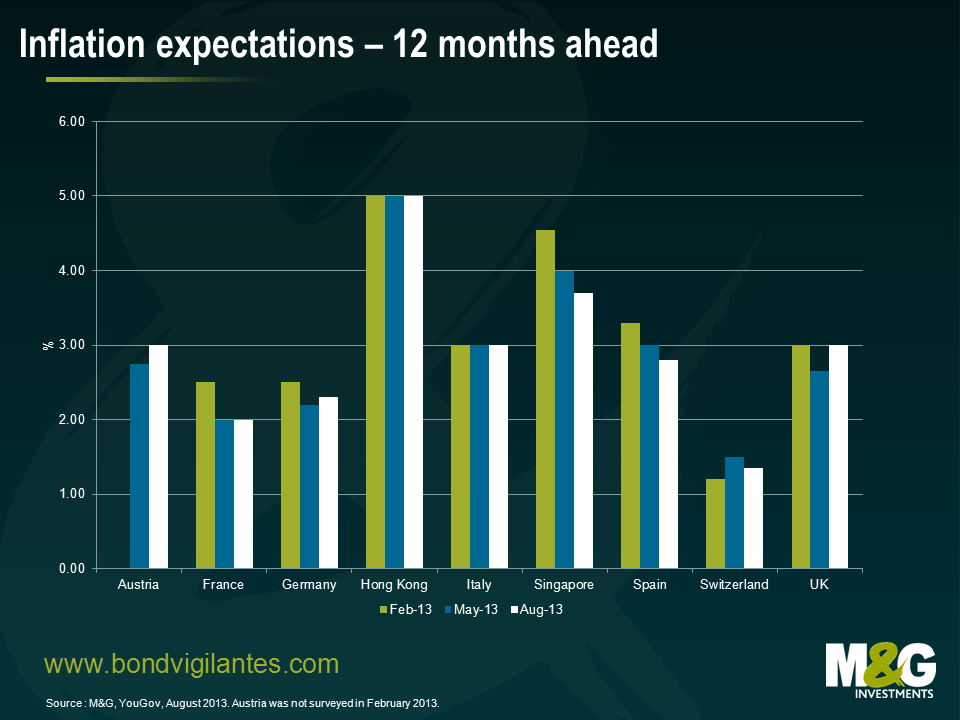

Despite high unemployment rates, excess capacity and a sanguine inflation outlook from the major central banks, it is important to keep an eye on any potential inflation surprises that may be coming down the line. For instance, we only need to look at ultra easy monetary policy; low interest rates and improving economic growth to see that the risk of an unwelcome inflation shock is higher than perhaps at any time over the past five years. The development of forward guidance measures is a clear sign that central banking has evolved substantially from 2008 in the form of Central Bank Regime Change. It appears that there is a growing consensus that inflation targeting is not the magical goal of monetary policy that many had once believed it to be and that full employment and financial stability are equally as important. Given that monetary policy appears firmly focused on securing growth in the real economy – at perhaps the expense of inflation targets – we thought that it would be useful to gauge the short and long-term inflation expectations of consumers across the UK, Europe and Asia. The findings from our August survey, which polled over 8,000 consumers internationally, is available in our latest report here.

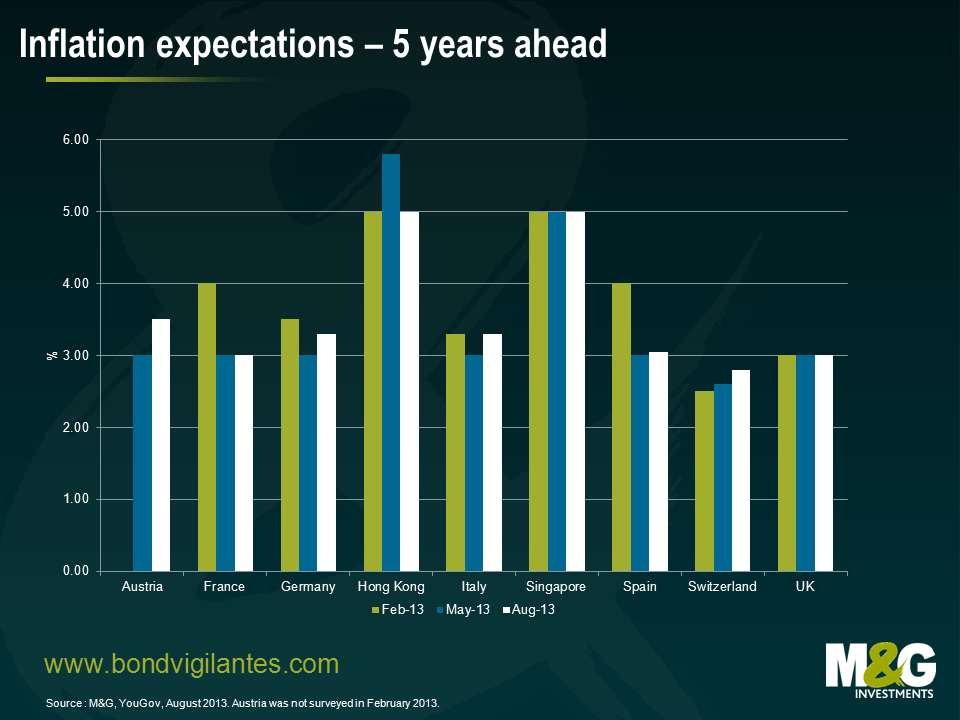

The results suggest consumers continue to lack confidence that inflation will decline below current levels in either the short or medium term. Despite evidence that short-term inflation expectations may be moderating in some countries, most respondents expect inflation to be higher in five years than in one year. Confidence that the European Central Bank will achieve its inflation target over the medium term remains weak, while confidence in the Bank of England has risen.

The survey found that consumers in most countries continue to expect inflation to be elevated in both one and five years’ time. In the UK, inflation is expected to be above the Bank of England’s CPI target of 2.0% on a one- and five-year ahead basis. All EMU countries surveyed expect inflation to be equal to or higher than the European Central Bank’s HICP target of 2.0% on a one- and five-year ahead basis. Long-term expectations for inflation have changed little in the three months since the last survey, with the majority of regions expecting inflation to be higher than current levels in five years. Five countries expect inflation to be 3.0% or higher in one year: Austria, Hong Kong, Italy, Singapore and the UK.

Consumers in Austria, Germany and the UK have reported an increase in one year inflation expectations compared with those of the last survey three months ago. This is of particular relevance for the UK, where the Bank of England has stated three scenarios under which the Bank would re-assess its policy of forward guidance. The first of these “knockouts” refers to a scenario where CPI inflation is, in the Bank’s view, likely to be 2.5% or higher over an 18-month to two-year horizon. Short-term inflation expectations in Singapore and Spain continued their downward trend in the latest survey results, registering their third straight quarter of lower expectations.

Over a five-year horizon, the inflation expectations of consumers in Austria, Germany, Italy, Spain and Switzerland have risen. Whilst inflation expectations in Switzerland remain at the lowest level in our survey at 2.8%, consumers have raised their expectations from 2.5% in February. Long-term inflation expectations in France and the UK remained stable at 3.0%. Meanwhile, consumers in Hong Kong and Singapore have the highest expectations, at 5.0%, although the Hong Kong number shows a decline from 5.8% three months ago.

Listening to the Bank of England Quarterly Inflation Report press conference – the first with Mark Carney steering the ship – a song immediately sprung to mind. The song was written by a former student of the London School of Economics, Sir Michael “Mick” Jagger with his colleague Keith Richards in 1965. There is no better way to analyse the current thinking of the Bank of England than through one of The Rolling Stones best songs, (I Can’t Get No) Satisfaction.

The new BoE Governor began with the positive news that “a recovery appears to be taking hold”. This wasn’t news to the markets, as more recently we have seen a remarkably strong string of economic data. However, the very next word in Mr Carney’s introduction was “But…”. What followed was, in my opinion, the most dovish sounding central bank policy announcement since the darkest days of the financial crisis.

Carney firmly announced his arrival as the global independent (excluding BoJ) central banking community’s uber-dove through the acknowledgement of a broadening economic recovery in the UK, and then making explicit that the BoE remains poised to conduct more, not less, monetary stimulus. Until now, these two conditions were considered by bond markets to be pretty much incompatible.

Carney told us that the BoE will maintain extreme monetary slack (in terms of both the 0.5% base rate and the £375 billion of gilts held) until the unemployment rate has fallen to at least 7%. He went even further than this, stating the MPC is ready to increase asset purchases (QE) until this condition is met. However, there are two conditions under which the BoE would break the new, explicit link between monetary stimulus and unemployment: namely, high inflation and threats to financial stability. Did the new governor have to put these caveats in place because other members of his committee would only agree to the announcement if they were mentioned?

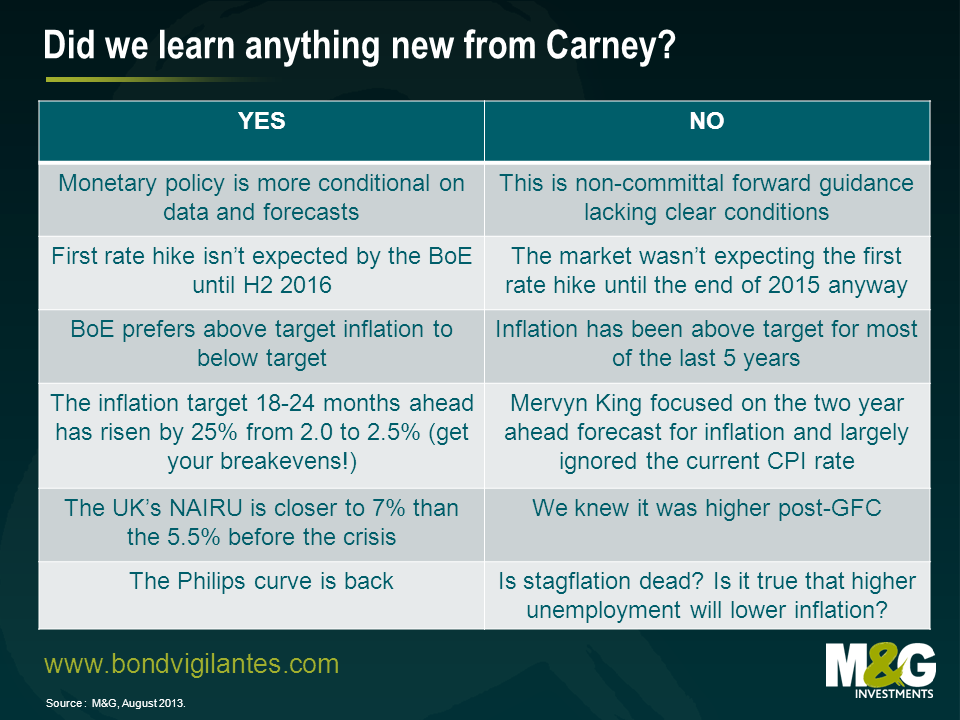

The new framework announcements were broadly in-line with what we were expecting. In that respect, the Governor’s major announcement was not too much of a surprise. The market agreed and there was a relatively muted response. Carney was supposed to fire our imaginations, so the question is – did we learn anything new? The “yes” and “no” arguments are outlined in the below table.

The market suspected Mr Carney would bring in some forward guidance, but I think the most interesting implication of this announcement today is that he felt the need to do something, but did not feel the need to increase asset purchases through QE. Mervyn took on the first part of Friedman’s equation, the supply of money. This was not inflationary as the transmission mechanism was broken, and the cash was hoarded and not released into the real economy. Could Carney be the governor to focus on the second part of the equation, money velocity? Forward guidance is designed to give individuals and companies the confidence to borrow in order to spend or invest. If they do, velocity will return as the transmission mechanism repairs. I believe we are considerably less likely to see an increase in QE under the new governor.

If forward guidance does not have the consequences Carney intends, and my belief that he is more focused on the transmission mechanism than his predecessor, what might Carney do next? At that point, he might increase schemes akin to Funding for Lending, and hand banks cheap funds at the point at which the banks release the loans to borrowers. This way, banks are heavily incentivised to lend at levels that are attractive to individuals and companies.

Carney told us that if and when unemployment reaches 7%, policy will start to tighten. But then he stated that if inflation exceeds 2.5% on the BoE’s shocking 2 year forecast (is this a rise in the inflation target?), or if inflation expectations move beyond some unannounced bound, or if financial stability is under threat, then he might have to break the newly explicit link between unemployment and monetary policy. And then he stated that even if unemployment hits 7%, this will not trigger a policy change, but a discussion around one.

I don’t think we actually got pure forward guidance, but a pretty muddled variant thereof. Bond markets are rightly unsure as to how to react, and have struggled for a satisfying interpretation. All we can really take from the BoE is that they will need to be sufficiently satisfied that the UK economy has reached escape velocity before hiking rates or reversing policy.

Stefan blogged earlier this week about the landmark sovereign bailout occurring in Cyprus, and about some of the interesting issues this raises. Sure enough, the parliament did not approve the package in the form talked about at the weekend. The reason? The taxes were felt too painful for the poor and too lenient for the more wealthy. This harks back to a blog I wrote about a couple of years ago, and goes to reiterate the issues we discussed then. However, for now I wanted to highlight some of the issues that this raises more specifically for the European banking system at large.

Firstly, depositors were presumed to be guaranteed by governments up to at least €100,000 in Europe. Last weekend, that notion was dealt a brutal blow by the Cypriot situation. However, it feels to us as though the main reason for the parliamentary delays is that deposit guarantees could and should remain in place – or at least to a greater extent than was implied in the original bailout package. This package stated that those people with deposits of less than €100,000 would pay a 6.75% tax, whilst those with more than this amount would be taxed 9.9%. The politicians that have delayed the approval of the rescue package want to see greater amounts of the burden borne by the wealthier (those with more than €100,000, and perhaps an even higher rate borne by those with greater amounts than, say, €500,000 in deposits), and so lesser amounts of the burden borne by those with small amounts of deposits.

My guess is that this is the key issue here. If the tax rates are not changed, then I would expect to see some significant moves in Spanish, Italian and other peripheral deposit flows and movements. As a risk, this must not be underestimated by the Troika. Why not maintain the deposit guarantee and generate the amount raised by the taxes, through taxing more on those with more than €100,000, more still on those with more than €250,000, and more still on those with more than €500,000?

Secondly, subordinated debt bail-in is a key part of the package, and without it one senses the Troika will not part with the bailout funds needed. We have expected weaker banks in weaker regions to have to use this as a necessary tool to break the sovereign-bank link for some time now. It is now official, and being used. I would expect more of these to come.

Thirdly and finally, sovereign bailouts of banking systems where the sovereign is already in an over-levered position will no longer be tolerated. It is time to break the sovereign-bank feedback loop (as we previously wrote about here). This has to be through bail-in and burden-sharing. However, the most unpalatable part of the proposed package to us (and I guess to many riotous Cypriots) is this: up until 2007 it was believed that senior bank bondholders ranked pari passu with depositors in the event of a bank failure. And now in 2013 we learn quite vividly that in actual fact in Cyprus depositors are likely to be subordinated to a bunch of wholesale and institutional (ie banks and insurance companies) investors?

The capital stack has been turned on its head in this regard. No one used to buy senior unsecured bank debt because they thought that depositors would take losses before them. Rather, it was because the markets believed 100% in the government guarantee of depositors. The pari passu relationship of depositors and bondholders supported high valuations on senior bank bonds. Thus to be pari passu with depositors, senior bank bonds need to take the same losses as depositors are. In my opinion, this part of the proposed deal is the most disgraceful.

So, I find myself wondering how on earth a deposit tax found its way into the package. The answer to me seems to be quite simple: contagion, or the avoidance thereof. We all know that in Europe and the UK in the future (as in the US already), senior bank bonds will be bail-in-able or writedownable if a bank fails or gets into difficulty. We were originally told that the date for senior bank bond bail-in in Europe would be 2018, although there has recently been much talk about bringing this forward to the beginning of 2015. It has long struck me that this should be the favoured route out of the bank-sovereign interconnectedness problem in Europe: continue to promote and enable senior issuance in Europe by banks, and then implement a higher level piece of legislation that at some date in the future makes all debt in the Eurozone and UK writedownable.

No matter how small Cyprus is relative to the rest of the Eurozone, if the Troika had forced senior bank bondholders to accept losses before 2018 – or is it 2015? – senior bank debt spreads would have suffered significantly across Europe. Given that this is the most attractive funding market for banks at the moment, as it is still cheap to issue from a bank’s perspective, and as sovereigns do not want to have to (or cannot, in the Cyprus case) step in to take on more liabilities on behalf of their banks, the Troika has ripped up the rule book and done the insane.

I think parliamentarians in Cyprus should force a rethink on the sovereign-bank feedback loop, as well as forcing a more palatable (ie Robin Hood) sharing of the burden between smaller and larger depositors. After all, can anyone truly imagine the French, German or any core European government accepting losses for their depositors whilst a bunch of international senior bank bondholders get made whole? Our view is that depositors should be protected (at least to the guaranteed amount) over and above all wholesale creditors, whether senior or subordinated. This is the first step to break the sovereign-bank loop. The second step, only to be used in cases where there is not enough senior and subordinated debt to prevent the sovereign, and so tax-payers, from having to bail out the failed institutions, is to look at forcing losses on depositors, but with preserving the preceding guaranteed amounts of deposits. The final, most radical, and rarest, step is to have to renege on that deposit guarantee amount, so as to avoid tax-payer bailouts and increased probability of sovereign default.

Depositors across Europe are already watching Cyprus carefully. My guess is that many are starting to check the amounts they keep with any one institution or in any region. Subordinated bondholders are already aware of the risks if those banks get into difficulty, but senior bondholders in my opinion are not. These investors must ask whether the Cyprus package is likely to be copied in future cases. And they must also start to wonder if they still have until 2018 before senior bonds can be bailed in, or if it is significantly sooner.

Today has seen the release of the decision by the National Statistician about what to do with the Retail Prices Index. We were told of the consultation in September last year, and were presented with 4 options, ranging from 1) to do nothing, to 4) to make RPI as much like CPI as possible.

Our view was always that the consultation arose as a result of the desire to correct an error made in the clothing component of RPI in January 2010 see blog. This change had seen the ‘wedge’ between RPI and CPI anomalously and erroneously increase by close to 1% following its implementation. We therefore believed that it was perfectly appropriate for the National Statistician to correct this error, and so we were expecting to see Option 2 materialise, which most closely targeted correcting this source of the wedge.

UK linkers had noticeably underperformed other markets since the announcement of the consultation. The market had initially started to price in a 30 to 50 basis point reduction in the wedge of RPI over CPI in expectation of Option 2’s intention to rectify the error. However, as Judgement Day approached nervousness increased in the linker market as people started to worry that the more severe options could be implemented.

Were Option 4 to have been recommended today, the wedge of RPI over CPI would have been reduced by approximately 100 basis points. This would have been a severe and brutal change for the index linked bond market. All else remaining equal, this change would have seen breakevens on index-linked bonds fall by approximately 70 basis points (allowing for 30 basis points of underperformance already priced in). To put it another way, this would have see the price of the longest index-linked gilt, the UKTi 0.375% 2062s, fall from 107.7 to about 85, a fall of 21%. Today, things really could have got nasty!

But the decision today has been Option 1. No change. Whilst highlighting that “the RPI does not meet international standards” and recommending that a new index be published, Jil Matheson “also noted that there is significant value to users in maintaining the continuity of the existing RPI’s long time series without major change, so that it may continue to be used for long-term indexation and for index-linked gilts and bonds in accordance with user expectations”. For the release, go to this link.

All the lobbying that we – and some others – have been doing behind the scenes has been worth it. In the Financial Times today, Chris Giles (who was on the Consumer Prices Advisory Committee) stated that the ONS rejected the committee’s advice in the face of ‘overwhelming opposition to changes in the calculation of the RPI’. The market has recently opened, and is removing the expected reduction of 30 basis points or so from Option 2. Breakeven inflation rates at the moment are up by 37 basis points at the 10 year part of the curve and by 22 basis points at the long end. The 2062 index-linked gilt is up by 12 points in price terms, and the whole linker market is rallying in the relief that no change is being made…

…for now! We will soon see the creation of a new RPI index, called RPIJ. This effectively makes RPI equal to CPI through making the older RPI index more modern by removing arithmetic mean and replacing it with geometric mean. This will be run in parallel with the old, untouched index. But it suggests that this debate is not over forever. We could again see recommendations to move from RPI to RPIJ, but more likely, we will soon start to debate moving the index-linked corporate bond market from RPI linkage to CPI linkage. The creation of RPIJ does seem a little irrelevant, where a new index has been created that few people will care about given that inflation linked bonds will continue to be linked to RPI and the government is clearly dedicated to linking other forms of government compensation to CPI.

Ultimately, though, even if we had seen a brutal reduction in RPI today, I still think that the strong case could be made to want to own UK index-linked bonds over the medium and long term. And changing the calculation to option 4 could have saved the Treasury a whopping £3bn per year, so while the decision to make no change has been great for inflation linked bond holders, it’s not so great for the UK’s coffers. Finally, the strong opposition to the RPI changes gives you a good idea of how hard it will be to implement austerity measures, and if we aren’t going to get out of this debt crisis through austerity, then the likelihood of us getting out of it with the help of inflation has just increased a bit!

Given the success that central banks have had in targeting inflation over the last decade or so, the recent increase in their powers, and the broadening of their remit to include economic growth, has been largely welcomed by the markets. But have we put too much faith in central banks abilities? And, with record levels of peacetime government deficits and the clear political incentive to tolerate higher levels of inflation, have we come to overestimate their commitment to reining in prices?

In this note, which is part of our quarterly Panoramic series, we argue that we are seeing potential upside risks to inflation as central banks continue to preside over the biggest coordinated global monetary stimulus that we’ve seen in recent history. In our view, the expansion of central banks’ balance sheets signals an unspoken shift in these institutions’ remits that could have important consequences for future inflation rates. It is a phenomenon we have coined “central bank regime change”.

The Bank of England and European Central Bank seem no longer to be primarily focused on delivering price stability. Their new mandate now covers supporting domestic banking systems, offsetting the effects of government austerity measures, bolstering trade and implementing the conditions needed to generate jobs and economic growth.

With central banks’ macroeconomic responsibilities straying ever further into what was previously the state’s domain, their independence is looking increasingly fragile. The hijacking of monetary policy by politicians cannot be ruled out, especially if it enables them to inflate their way out of their growing debt burden. If we get to this stage, inflationary pressures will rise, although central banks’ credibility will be tarnished and policy responses rendered ineffective.

In our view, there are potentially plenty of reasons to expect the current period of low inflation to come to an end. Central banks are still thinking of new ways to ignite growth and they appear to be increasingly tolerant of above-target inflation. But are they moving ever closer to a major policy error that could ruin their inflation-targeting credibility? And should we all start thinking about inflation again?

There has at almost all times been a ‘wedge’ between RPI and CPI, given different calculation methodologies (arithmetic mean vs geometric mean, respectively), different items within each, and different weights of these different items. The long term difference has on average seen RPI at 0.5% to 0.8% more than CPI. Recent changes, though, saw the wedge widen in 2007 to more than 2%, and to almost 2% again in early 2010.

What are these changes? RPI is a much older index, originally conceived in the early 20th century to track the effect of price moves on workers during The Great War, using less up to date and less relevant averaging calculations and, arguably in some cases, weightings and items. CPI was not developed until much later, in 1996.

Since the coalition’s formation we know that the government has been attempting to change certain future liabilities’ (eg public sector pensions and benefits) indexing from RPI to CPI. Why? Simply, because this wedge of RPI over CPI means over the long term it is more expensive for the government to pay RPI than CPI. And given the long duration of these liabilities, the present value and so budgetary impact today of such changes are extremely powerful in terms of delivering on austerity. From a rather different perspective, that’s why there has been so much resistance to these changes on the part of public sector workers, amongst others.

The ONS is the body that is responsible for the classification, collection and measurement of these compensation indices – no mean task I hasten to add. We have heard much in research notes and certain press articles in recent weeks about the ONS undertaking a project to eradicate the wedge entirely! What would this mean for us as investors? It would be less attractive to own UK linkers, as inflation as defined by RPI would be structurally lower than it has been. The breakeven rate (the rate between nominal gilt yields and index-linked gilt yields) would fall, meaning that index-linked bonds would underperform nominal bonds. This would be especially so at the long end, where the price or present value impact would be felt most.

I can think of 5 strong arguments against such an assault on the wedge:

1.To eradicate the wedge altogether would be tantamount to an event of default, especially if this is specifically to eradicate the structural difference between the two indices! We bought these securities on the basis that we would be paid RPI, which we know changes in terms of items and weightings on an annual basis, but according to changes in spending habits rather than Government policy. That’s fine! But the index is based on an arithmetic mean and always has been, and so will (almost always!) be higher than an index calculated according to a geometrically calculated mean. To change this, willingly and knowingly, with the purpose of reducing future outgoings of index-linked borrowing cashflows feels very similar to the altering of the War Loan’s coupon from 5% to 3.5% in 1932, or to the Greek PSI exercise of coercive write-downs, neither of which, arguably, were ‘defaults’.

2. The Statistics and Registration Service Act that covers changes to RPI states that any changes to the index must be carried out in consultation with the Bank of England as to whether the changes are fundamental and materially detrimental to holders. If the BoE decides that both of these conditions are met, then the changes to RPI cannot go ahead without prior approval of the Chancellor. Well, given the changes Mr Osborne has been trying to make elsewhere in his search for austerity, might he simply approve the changes in the index? Well this would not be without significant risks, electorally, and it would have a fundamentally and materially detrimental impact on the ability of the DMO to borrow through the linker market, which we will touch on in a moment. But perhaps it would be open to legal challenge? Consideration of this last issue involves looking into the contractual protections embedded within the old-style 8 month index-linked gilt prospectuses. It turns out that these documents state that if both the conditions of a change to the index above are met in the opinion of the BoE, HMT will inform bond holders of this, and offer them the right to redeem their stock. So the next issue for holders is: at what price can I put my bonds? The prospectuses state that “the amount of principal due on repayment and of any interest which has accrued will be calculated on the basis of the index ratio applicable to the month in which repayment takes place”. Thus, in current markets, with substantial negative real yields, the protection provided in these old style bonds is not sufficient to compensate holders fully, as it only pays accrued inflation. As a result of this, holders are going to be very sensitive to any chatter about substantial changes to the index. And this will have pretty major consequences. For instance, looking at the 4.125% gilt linker of 2030, the current price of the bond (given by current accrued RPI relative to RPI at the date of issue, along with future assumed inflation of 3% per year, positive real coupons, and negative real yields) is 316.5. To take this bond and assume we put the bond in the event of a change to the RPI, we multiply par (100) by the index today (242.5) over the base RPI at issue (135.1) to arrive at a price of 179.5. A holder would be set to lose 137 points, or 43% of the bond’s current value!

3. It would also serve to ruin the RPI linker market, at least for a long while. The uncertainty from recent headlines cannot be helping sentiment among the linker buyer base at the moment, and this has been an extremely important source of funding for our high levels of borrowing in the UK in recent years. It would be unwise to annoy these buyers, as it will only serve to increase the costs of issuance (through demanding higher real yields), irrespective of the final outcome of the ONS’ project to lower the paid level of inflation. Indeed, this begs the question as to whether to make the change to linkers from the perspective of our financing position would be to shoot ourselves in the foot?

4. The ONS states on its website under its ‘Vision and Values’ that: “Our mission is to improve understanding of life in the United Kingdom and enable informed decisions through trusted, relevant, and independent statistics and analysis” (my emphasis added). To target the structural and total eradication of the RPI-CPI wedge would in my opinion clearly be an impeachment of its independence, and would see huge criticism about the political motivations of such a change in the index. This could perhaps lead to legal challenge.

5. Could this not be interpreted as an attempt to specifically and deliberately conceal high levels of headline inflation, Argentina style? Or, if not, to artificially and deliberately manage UK inflation down? It is not just pensions and benefits that are linked to inflation, but wages and commercial contracts, which all have significant impacts on the economy’s overall level of inflation. To change the major index underlying all these contracts from RPI to CPI (the logical equivalent of making RPI CPI) would be to manage inflation down, at a time when so many are concerned about stubborn inflation in recent years, as well as the effects of super-accommodative monetary policy on future inflation. What would this tell us about our politicians’ and policymakers’ inflation targeting attitudes and indeed capabilities?

As a result of these arguments, I personally find it difficult to believe that this is the intention of the ONS or of its project to examine the wedge. I believe instead that the review is targeted at removing some of the anomalous sources of the wedge, which resulted, in no insignificant part, from a change in measurement that took place in 2010 that particularly impacted the wedge between RPI’s clothing price level and CPI’s clothing price level.

Indeed, the clothing and footwear components of RPI and CPI alone represented 60% of the total wedge between the two indices! This kind of change would be justifiable in my opinion. Anything else would at best be ill-advised, and at worst would be mismanagement on a major scale.

We have written on numerous occasions about the hitherto inseparable links between sovereigns and banks, and we have also written about the benefits of writing down bonds to create capital (see The New Era for Bank Bonds: Send In The Clowns? and Equitisation of bank capital bonds) . In 2007 the global markets woke up to the fact that the US subprime market was blowing up, and in 2008 realised that due to financial engineering and securitisation, both of which were preposterously known at the time as ‘risk dissemination and minimisation’, banks the world over had major solvency issues as vast quantities of investments plummeted in value. This, in turn, led to a liquidity crisis as the investment markets shunned investment in banks and the interbank market froze over.

The crisis we are in today is the same crisis we were in 5 years ago. Sovereigns had to step in to guarantee their banking systems, so as to enable debt to be rolled over and confidence to return. In the short term the most important thing was to provide liquidity, which we saw through government guaranteed debt issuance and secured funding directly with central banks in the UK, US and more recently Europe. Next, sovereigns had to buy huge volumes of illiquid assets from their banks (US), or provide direct capital injections to support their solvency (US and UK), as the perception dawned that the liquidity crisis was caused by a solvency crisis.

All this time, the inevitable link between sovereigns and banks was becoming more and more deeply intertwined. And whilst it may feel that the Great Recession has metamorphosed from a banking crisis to a sovereign one, it hasn’t really: sovereigns took on increased liabilities to protect their banking systems and now find themselves in the ‘limelight’. It’s the same crisis, with a different focus.

Many European banks, though, remain substantially undercapitalised. Hence, the system is still overwhelmingly dependent on central banks to provide them with liquidity at an affordable cost. All the time the sovereigns providing liquidity are becoming more and more tied to the health or otherwise of their banks and the assets they are taking from them as collateral.

Has the time come for this cycle to end? Might the severance of this link bring the beginning of the end of the sovereign crisis? Many European banks are still on 24 hour life support, saddled by enormous levels of liabilities that are cutting off new lending and suffocating new investment through the multi-year crisis in confidence in lending to and investing in banks.

So how will this occur? Well my sense is that there’s abundant liquidity at the moment after all the LTROs, inter-central bank funding lines, secured lending facilities and covered bond new issuance. The problem is far more one of solvency and capital adequacy in Europe, where the very worst of the banking crisis continues today. For sovereigns to provide their national banks with the recapitalisations they need, via wholesale nationalisations, would only see a worsening of the sovereign debt crisis, as the funds would have to come from somewhere. So this approach doesn’t really work. And is it really desirable from the perspective of the taxpayer?

The solution? We need new capital, in substantial scale, and fast. The time may have come to sever a significant part of the link between a sovereign and its banks. Unsecured bank bonds in peripheral Europe where the sovereigns are struggling under high borrowing costs, and so where the cost of providing guarantees and funds to their banks are painful, should now be written down in certain cases. Both subordinated debt and senior unsecured bonds would see defaults, in some cases even to zero. This would generate huge amounts of capital (which writing down only subordinated debt would not achieve on its own), and does not involve the troubled sovereign having to borrow more from the markets or seeing debt / GDP levels spiralling. Yes this is painful for investors and to risk-taking savers who are exposed to bank bonds in their pensions and so who suffer losses there. But the write downs are taken. Capital is generated. Deleveraging of the system occurs quickly and substantially (at last!). And the severance of this part of the sovereign-bank link (deposit guarantees must remain in place) means that the banks might just stop dragging the sovereigns down with them.

Policymakers and politicians must be aware (and I’m assuming they are already) of the benefits of this first step towards cleansing the system. If this doesn’t work, then nationalisation is the last resort, and the taxpayer must step in one last time. But this situation of creeping nationalisation where taxpayers provide 24 hour life support in European banks through emergency policy response after emergency policy response, at the expense of much higher tax and lower quality of life across all citizens for a very long time feels wrong, at least before the risk-takers have suffered. Could now be the time for bank bondholders to see defaults, where they are needed? There are countries where these dramatic measures aren’t needed, as well as individual banks where they won’t be needed within troubled systems. The process will be painful for bearers of risk (investors and savers), but it might, more importantly, provide the capital the system so needs to start restoring confidence in the banks, and the sovereigns would benefit from cutting the tie with the non-deposit banking system. So policymakers have to work out whether society overall would be better off with this new approach than the current one. They may very well conclude that the present situation of taxpayers being subordinate to bank bond holders, rather than vice versa, is a morally repugnant system.

Some of us are damned if we change tack and take this approach. All of us are damned if we don’t.

Over the last few weeks we have witnessed a meaningful bounce in inflation breakevens in the UK, Europe and the US. When breakevens are rising, it is a signal that the fixed income market is anticipating higher inflation than has been priced in. It also means that index linked bonds are outperforming conventional bonds. In the UK, the linker gilt of 2016 has outperformed the conventional gilt by 45 to 50 basis points in yield terms since the start of this year.

Why have the bond markets started to price in higher levels of inflation?

Perhaps there is an element of geo-political risk affecting the oil price, which feeds into the inflation baskets in a plethora of forms? Yes, but I don’t think oil is the major culprit here, although in the US, where oil is taxed far less than in the UK or Europe, inflation is far more sensitive to changes in the oil price. See Jim’s blog here.

Perhaps rising breakevens owe to fears around money creation? In Europe, at the end of 2011 the interbank market was completely disfunctional, and we were entering a deflationary spiral. But the long term repurchase operations (LTRO) have added somewhere in the region of €1 trillion euros to banks over the last few months, the interbank market has been showing signs of being slightly less disfunctional, and the risks of deflation feel for the moment substantially reduced. In the UK, the mechanism of quantitative easing boosted the prices of conventional gilts more than index linked gilts, as the Bank of England did not purchase linkers directly. This artificially suppressed the relationship between the conventional gilt and the linker (the breakeven), at exactly the moment when money creation ought, in my opinion, to have seen higher inflation risk premia priced in. The strong performance of index linked gilts in the UK either owes to a fear that improved economic data means we are closer to the end of QE than the beginning, so the artificial source of demand for gilts is not going to be in the market for much longer (a relative call), or owes to the market’s deciding that we are not going into a disinflationary or deflationary economy, and are more likely to see on target inflation or higher.

It is worth thinking about the levels of 5 year breakevens in the chart, a relative valuation measure. In the UK the bond market is expecting inflation to average 2.8% a year for the next five years. Remember though that this is RPI inflation, which historically has averaged 0.8% more than CPI. If we assume this historical relationship holds, then this 5 year breakeven implies CPI will be bang on the Bank’s target of 2%. So on this basis the breakeven does not make inflation protection look expensive at all. Considering the 5 year breakeven in Europe, which is currently 1.6%, this is still pricing in inflation being below the 1.8% (ish) target on average for the next 5 years. With aggressive money creation (at last!), surely the risks are skewed to the upside? In fact, only the US market is pricing in inflation to be above target for the next 5 years. I think that this is the correct side of the inflation target for linkers to be valued at, and I believe there is a good chance the UK and European markets start to move towards this US dynamic.

Why? Firstly because of the ultra low interest rates and ultra accommodative monetary stance at the ECB, BoE and Fed. And also because of the large scale money creation we have seen in all three markets and have discussed briefly above. But most importantly to me is the fact that at this moment in time, the three central banks in question all have a clear and visible inflationary bias. They would rather have inflation than deflation (rightly). But now they are showing a propensity to favour above-target inflation over below-target inflation. This is tantamount to a (temporary or permanent, we do not yet know) change in the inflation targets. And this must, in my opinion, see higher inflation risk premia. How do we show this clear inflationary bias? Inflation is significantly above target in all three economies, and yet policy is not only not being tightened, the taps are still very much on!

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.