Big Beautiful Bonds: why big tech’s borrowing boom is reshaping credit markets

The biggest shift in credit markets over the past six months hasn’t come from banks or industrials, but from Big Tech.

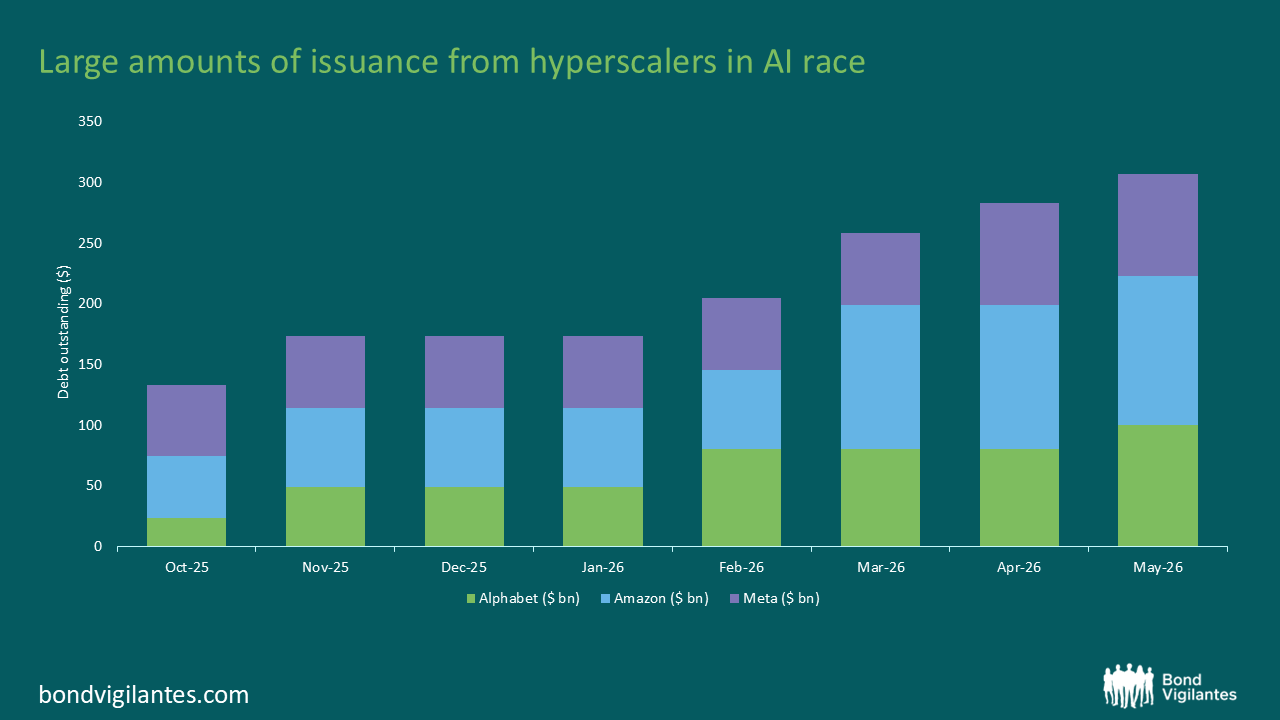

Alphabet, Amazon and Meta have been issuing debt on a scale rarely seen in the sector. Combined, these companies are now among the most significant contributors to global corporate bond supply – a development that is beginning to reshape investment grade credit markets.

Source: Bloomberg, May 2026

This wave of issuance reflects a simple reality: the largest technology companies are entering a capital expenditure cycle that can’t be funded through cash flow alone.

Two forces sit behind this shift.

First, artificial intelligence. The build-out of data centres, semiconductors, networks and supporting infrastructure is extraordinarily capital intensive, even by the standards of the technology sector. As in previous investment cycles in telecoms and media, balance sheets are expanding to fund what is seen as the next phase of structural growth.

Second, US policy. Incentives embedded in the current fiscal framework have materially improved the economics of domestic capital expenditure, effectively accelerating investment. In practice, this acts as a subsidy and corporates are responding accordingly.

Normally, a sharp increase in borrowing would place pressure on credit quality. But in this case, the scale of earnings matters more than the scale of issuance.

With EBITDA across Alphabet, Amazon and Meta running at roughly $150bn to $200bn, even large increases in debt translate into only modest changes in leverage. The impact on debt-to-EBITDA is limited, and these issuers remain well within high investment grade rating thresholds.

The more immediate effect is on market pricing.

Bond markets tend to react to large increases in supply by demanding a higher spread. This dynamic is well established, particularly in sectors experiencing capex-driven issuance cycles. What makes the current episode notable is that it is occurring in some of the highest-quality names in the market.

These companies are becoming a larger part of major bond indices. Their growing weight in benchmarks such as the Bloomberg Global Aggregate Corporate Index reflects both the scale and persistence of issuance.

Source: Bloomberg, May 2026

Yet there are structural constraints on the demand side.

Unlike equity investors, bond portfolios are typically subject to strict diversification limits. Exposure to any single issuer is capped well below levels commonly seen in equities. This means that even highly rated issuers can struggle to find incremental buyers when supply increases sharply.

In the short term, the bond market simply finds it difficult to absorb issuance at this scale.

The result is a notable dislocation. Some of the largest, most profitable companies in the world are issuing debt at spreads that appear attractive relative to the broader investment grade market.

For investors, that creates a clear opportunity.

The combination of strong fundamentals, policy-driven investment and temporary supply pressure is opening a window into high-quality credit at more favourable valuations than might otherwise be expected.

In other words, today’s surge in Big Tech borrowing is not just a story about funding growth – it is also creating a rare entry point for bond investors and an opportunity to invest in Big Beautiful Bonds.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.