Tethered to the tail of a drunken dragon

High but seemingly unstoppable, markets continue to perform strongly despite a series of significant economic and geopolitical shocks. Meanwhile, academic and institutional voices warn that financial vulnerabilities are elevated at a time when policy flexibility is constrained. Not only is there is a record amount of sovereign debt outstanding, especially in the US, but the majority of it is now held by more price-sensitive and mobile investors. Moreover, a significant cohort amongst them are heavily leveraged, rendering them susceptible to market corrections. If conditions were to shift abruptly, the adjustment could be challenging.

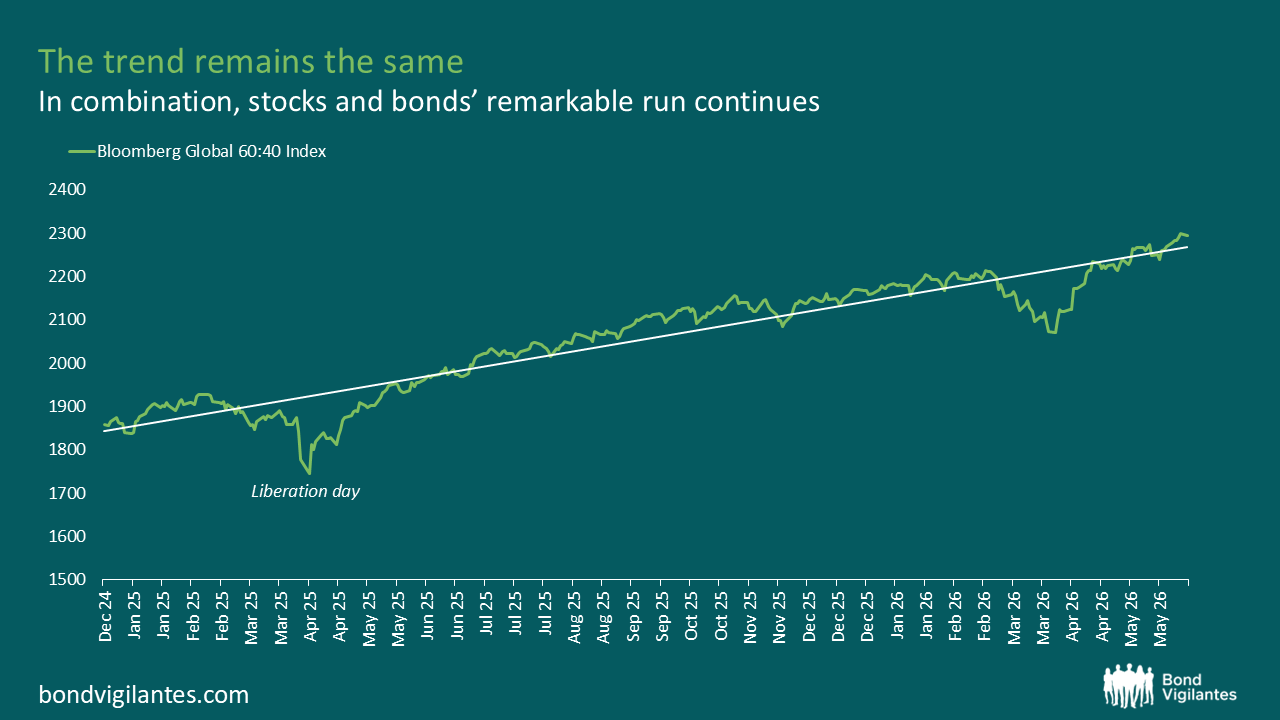

Crisis? What Crisis?

Risk appetite is alive and kicking. Year to date, the S&P 500 is up 10.35% (24% annualised) and Space X has just listed at a valuation of USD 1.77trillion (6% of US GDP), the biggest in history. The riskier asset classes in public fixed income markets, Emerging Markets (EM) and US High Yield (HY), have also seen spreads compress to levels last seen in 2007. So quick are markets to brush aside anything that might muffle the positive mood music, that to judge by market performance alone, would be to understate the range of macroeconomic and geopolitical risks currently in play.

The list is uncomfortably long. Unprecedented levels of advanced economy debt; questions around liquidity and valuation in private markets, the scale of AI-related investment, the biggest ever disruption to energy supply, trade disruption, the breakdown of institutions and elevated geopolitical tensions. Yet, markets rally with every announcement of a deal that may or may not incrementally improve the flow of oil through the Strait of Hormuz.

Source: Bloomberg, BMADM64 Index, last price, data as of 8 June 2026.

Meanwhile, in academia, the disconnect in sentiment with the market remains significant. Of late, a chorus of voices from the academic and regulatory world have issued warnings that converge on a core theme: these risks are unfolding against a backdrop of heightened global imbalances and unprecedented financial fragility. In recent weeks alone, the IMF, the Bank of England (BoE), the G7, the G30, the Centre for Economic and Policy Research (CEPR), the Bank for International Settlements’ (BIS), Gita Gopinath, and Martin Wolf have all sounded the same alarm. There is an unparalleled build-up of risks in the global financial system.

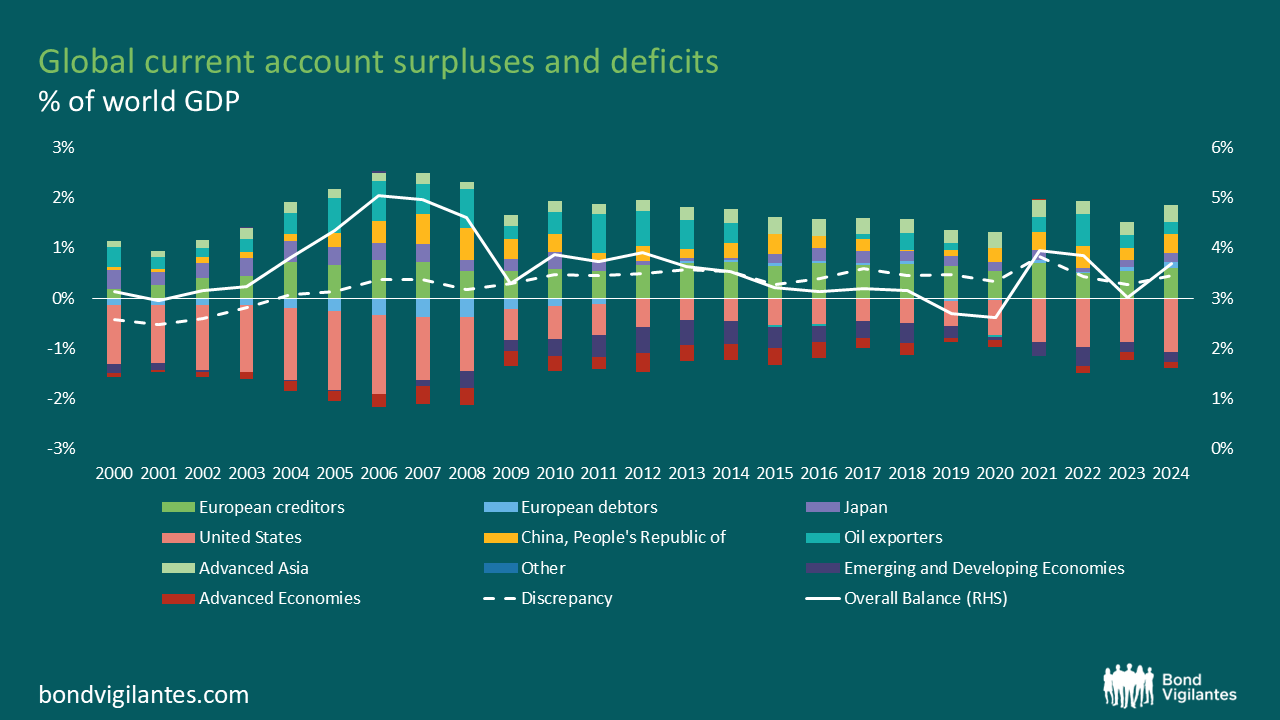

Global Imbalances Redux

The narrative about global imbalances is not new, and the players are familiar: record (nominal) current account deficits in the US (USD1.2 trillion in 2024); record (nominal) current account surpluses in Japan, China1 and the European Union (also a combined USD 1.2 trillion in 2024); the flow of excess savings from the surplus group to the deficit ones; and a resulting build-up of financial risks. We have been here before. The dénouement was a global financial crisis (GFC) in 2007-09, followed by a sovereign debt crisis in Europe shortly thereafter. But haven’t current account deficits corrected in the aftermath? If so, why, 20 years on, are we talking about them again?

Note: Discrepancy is the deviation of the sum of all countries’ balances from zero. Overall balance is the sum of absolute values of current account surpluses and deficits.

Source: CEPR; Bruegel based on IMF (2025c).

Source: CEPR; Bruegel based on IMF (2025c).

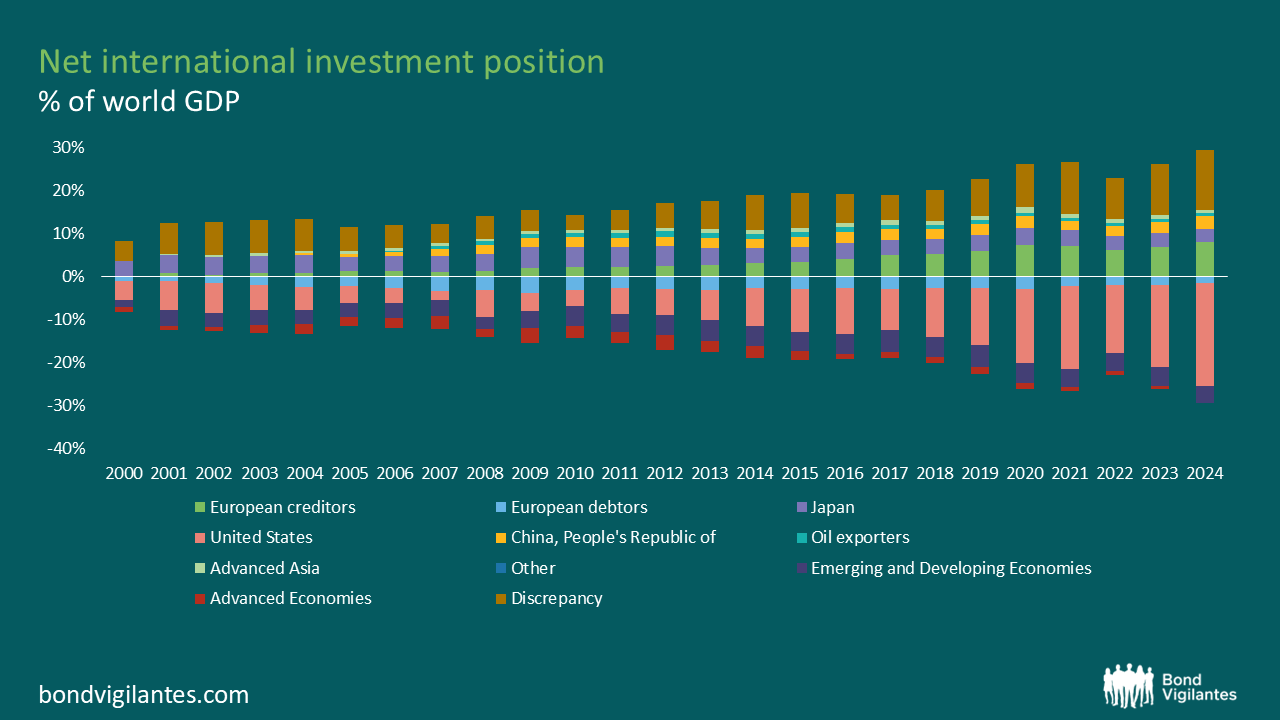

At first glance, it would appear they have. However, as the charts above show, the imbalances remain large, and the same patterns have persisted more or less unchanged. To gauge the cumulative impact of this persistence, one has to examine the “stock” number, or the Net International Investment Position (NIIP)2. The US’ NIIP is now in deficit to the tune of a stunning 90% of US GDP (24% of world GDP) vs. a deficit of 28% of GDP in 2009 (5% of world GDP). Think about that for a minute. The US now owes the rest of the world almost a quarter of the world’s combined GDP!

Sure, this partly reflects sky-high US equity valuations and USD strength3, but it also effectively signals the loss of US “exorbitant privilege” i.e. its ability to earn higher return on its external assets than the cost it pays on its liabilities. In short, the US can no longer finance further current account deficits without increasing its liabilities to the world. This is a sea-change from the GFC.

Source: US Treasury International Capital (TIC) data. Data as of December 2025.

Has King Dollar been de-throned?

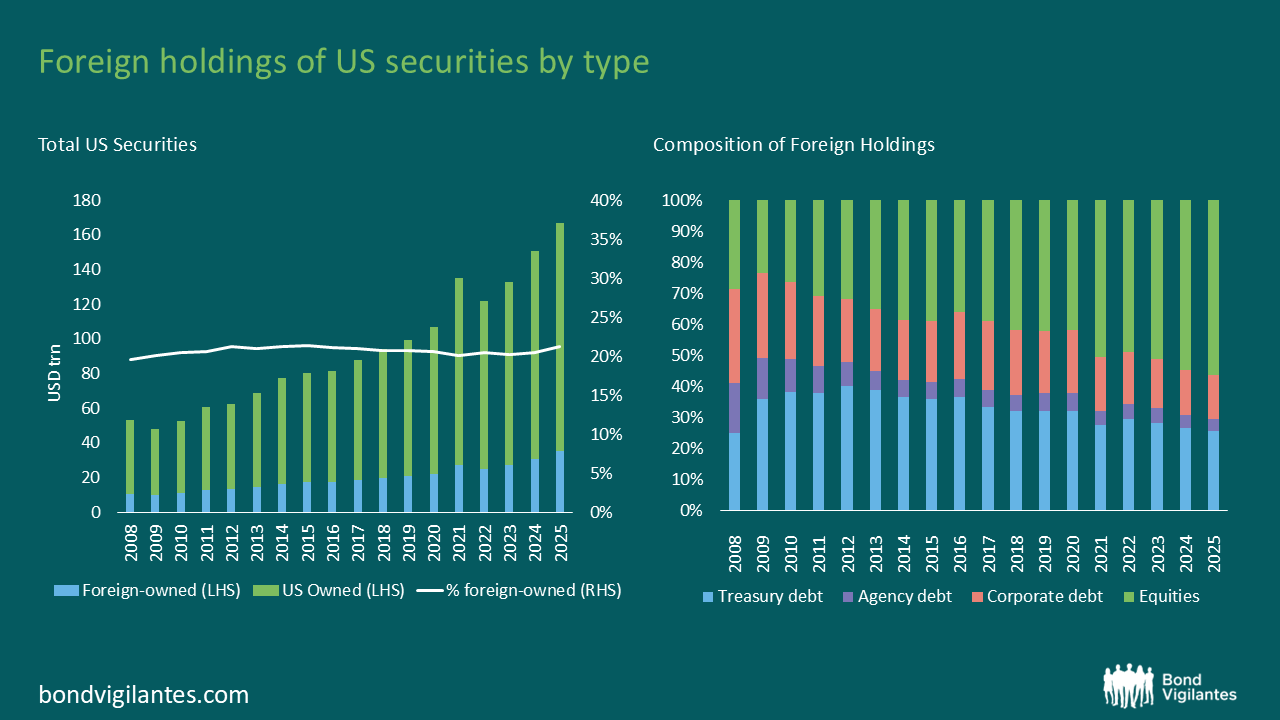

The other significant difference in this redux of global imbalances is who the foreign liabilities are owed to. In the last 12 months, there has been significant debate around the fact that investors are looking to diversify away from the dollar, the so-called “dollar de-basement” trade. A brief look at the annual TIC data report on the foreign holdings of US assets is enough to debunk the myth that the dollar has lost its shine. It hasn’t.

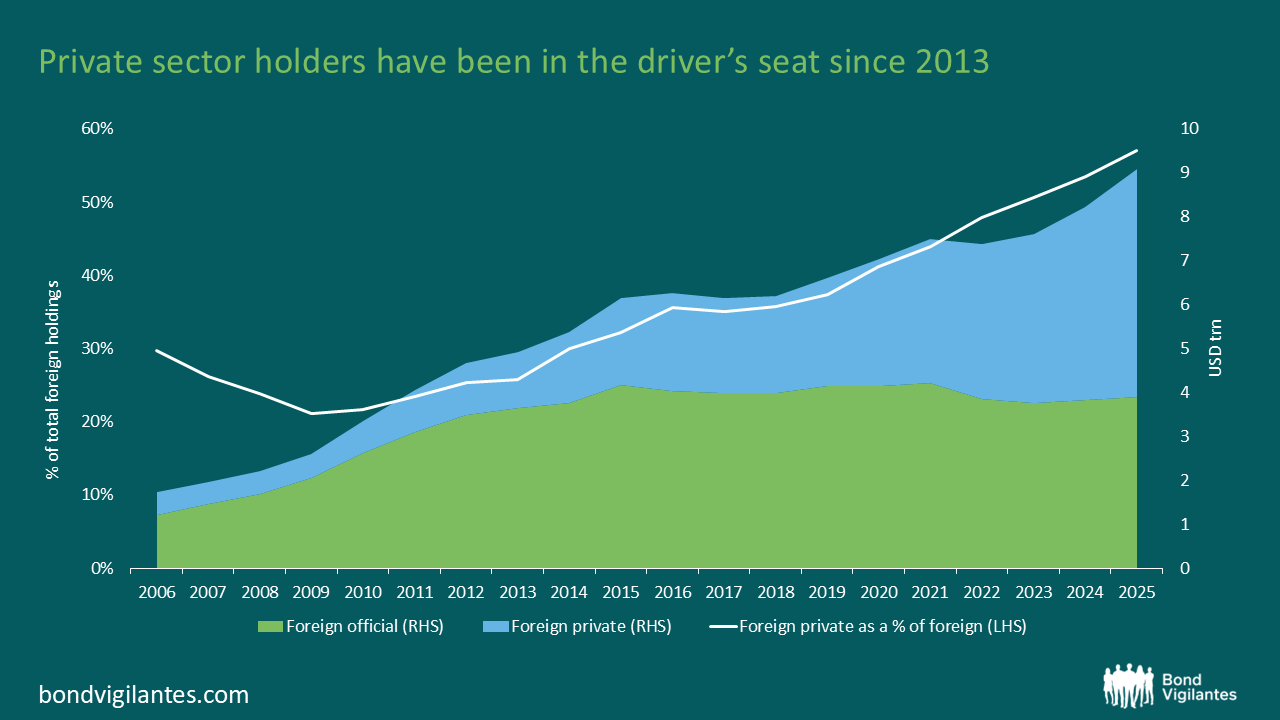

Certainly, “official” or public sector appetite for US assets, particularly US Treasuries, has waned. As a consequence, yes, US Treasuries’ share in official FX reserve holdings has fallen from a peak of 72% in the early 2000s to 56.8% currently. But it has been more than replaced by private sector appetite for US assets. Indeed, foreign private sector players surpassed public sector ones in amount of US Treasuries they own in 2023. In a nutshell, price sensitive, and crucially, highly nimble, private capital has replaced price-insensitive public savings (central banks). This is particularly relevant in the context of the vast sums of US Treasury issuance, its shorter-term structure and higher rollover, and the sharp rise in sovereign bond yields in the post-pandemic world.

Source: BIS (2025); US Treasury International Capital (TIC) data. Data as of December 2025.

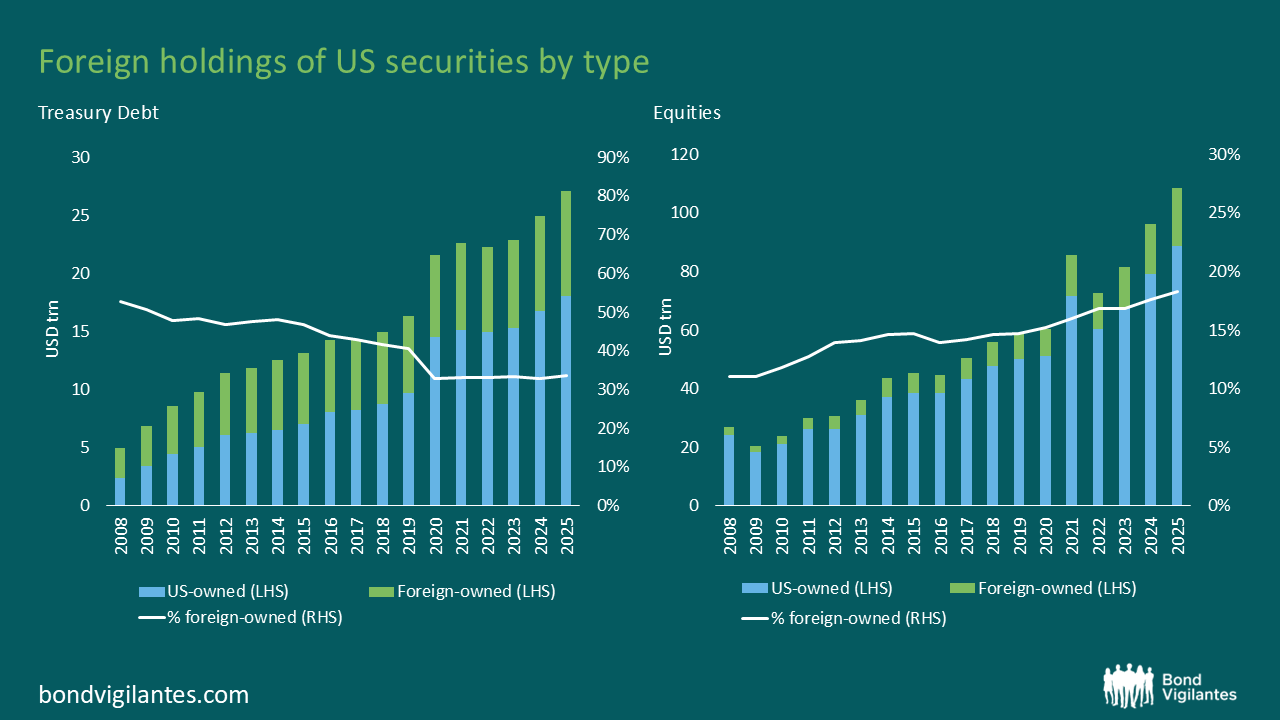

It is nevertheless true that, over time, more Treasury debt has ended up in domestic hands, and that foreigners, as a bloc, have reduced their exposure to US debt assets. However, as per TIC data, this is because foreigners have channelled proportionately more of their savings into US equities, rather than US debt.

Accordingly, the share of equity holdings as a percent of the foreign portfolio of US assets has doubled from 28.8% in 2008 to 56.2% at end June 2025. But throughout this rebalancing since the GFC, the overall share of US assets in foreign hands has remained remarkably stable at circa 20% of the total outstanding. In summary, whichever way you slice it, the TIC data clearly show that the US remains the world’s dominant player in the supply of both safe and risky assets. The world still hankers after dollar assets, just different ones.

Source: US Treasury International Capital (TIC) data. Data as of December 2025.

Shadow Banking of a different sort

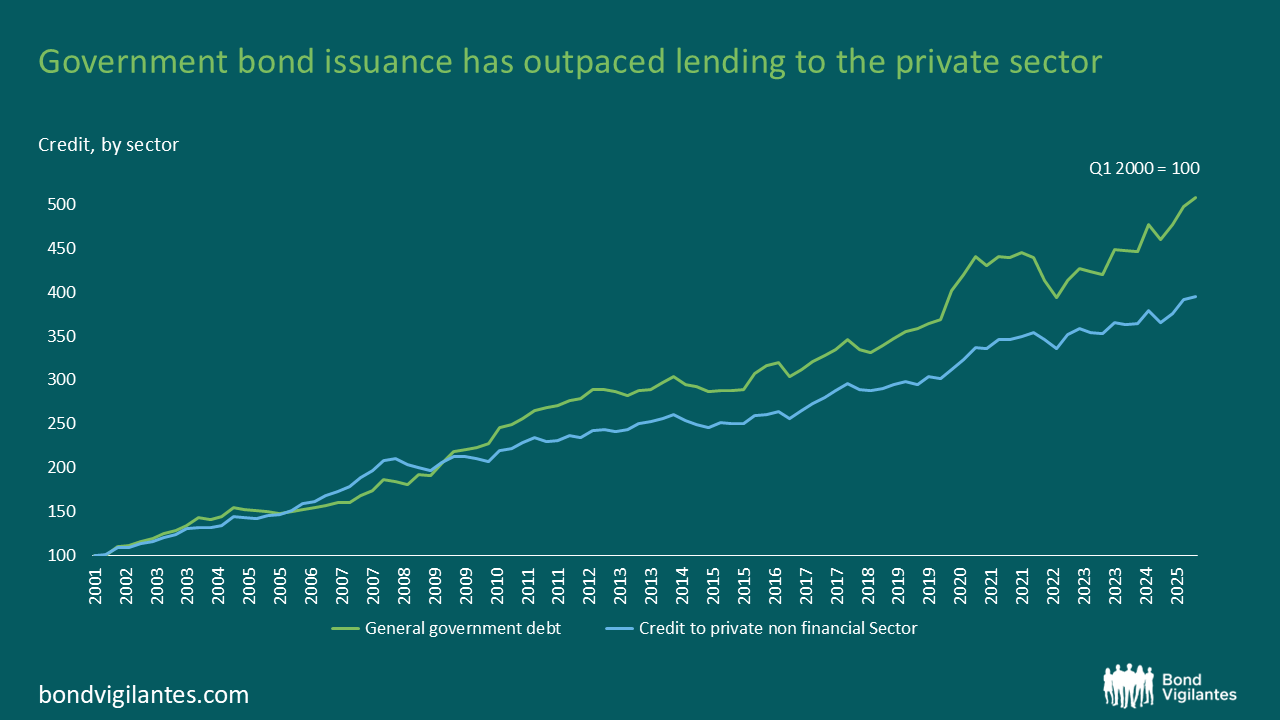

Also notable about the shift of US liabilities, particularly sovereign liabilities, into private hands is the type of private sector investor they have ended up. This is where things get interesting, as they have potential implications for market stability. Because the GFC was a crisis that originated in excess credit growth to the private, non-financial sector, mediated by regulated banks, the post-GFC world has seen financial intermediation shift in two consequential ways.

Firstly, as the private sector busied itself with balance sheet repair, governments took up the demand baton, leading to large and persistent fiscal deficits. Unsurprisingly, lending migrated from the private to the public sector. Secondly, as banking regulation tightened, financial intermediation shifted away from banks and into the less transparent and differently regulated (compared with traditional banks) world of non-bank financial institutions (NBFIs)4. In this grouping, investment funds and hedge funds, the bulk of which are based in the US and Europe, lead the charge.

Source: BIS; Hernández de Cos (2025). Data as of December 2025.

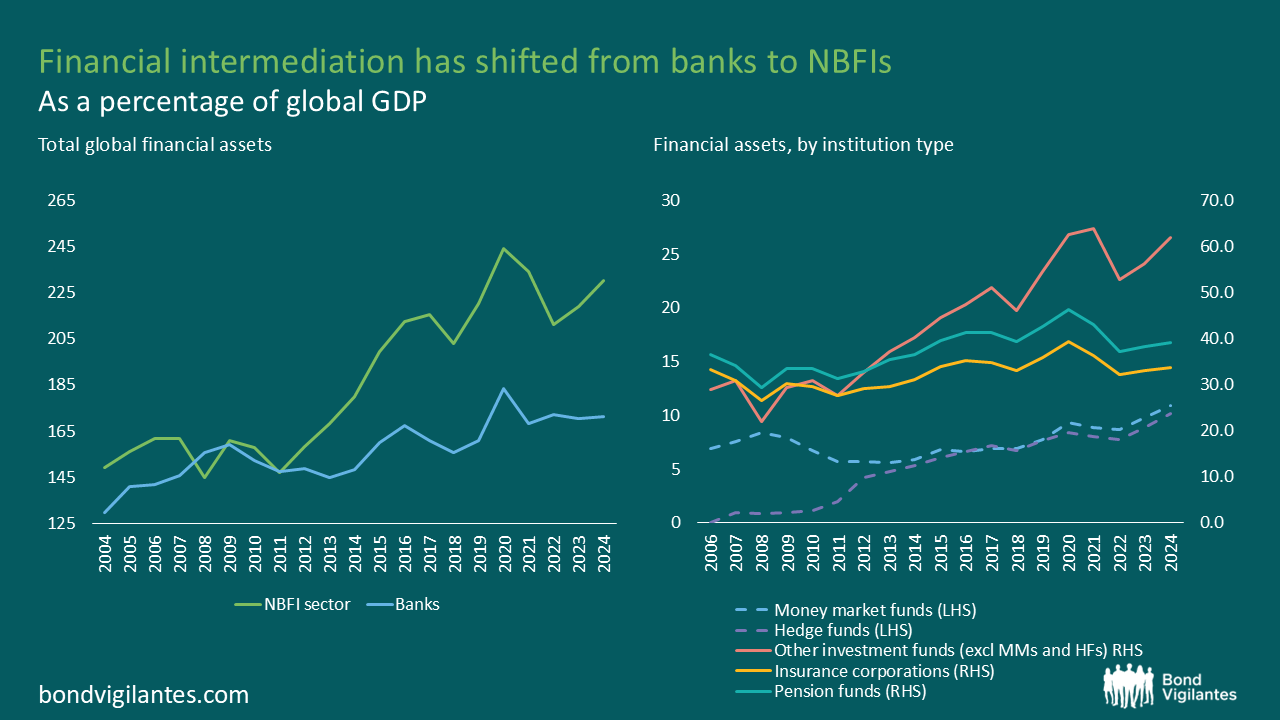

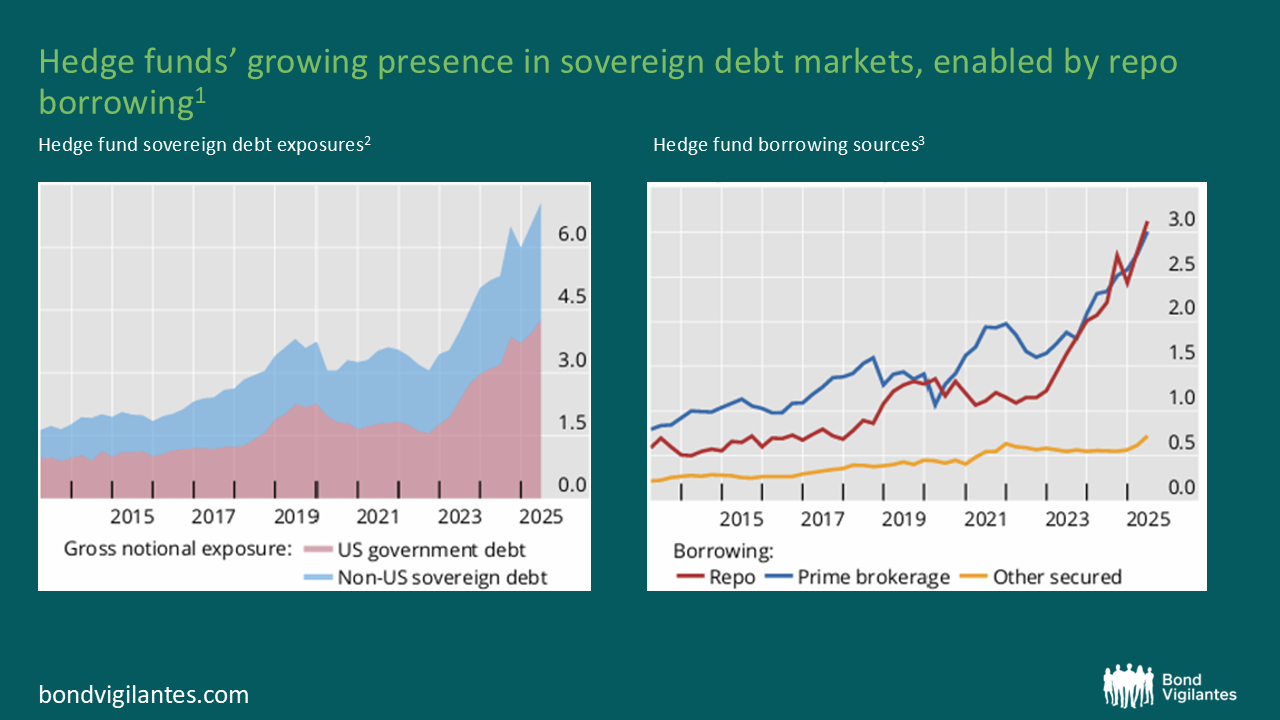

Taken together these two trends mean that in the post-GFC world, NBFIs have become the dominant providers of financing, and now exceed bank funding. According to the G30, at end 2024, NBFI assets totalled USD 260 trillion globally – more than half of total financial intermediation. Of this, private credit assets are estimated at USD 3-3.5 trillion, suggesting that the bulk of NBFI activity is concentrated in publicly traded markets, roughly 65% of which is the sovereign bond market. In other words, portfolio managers in sovereign bonds, particularly developed market (DM) sovereign bonds, have become the linchpin of the global financial system.

HFs = hedge funds; MMFs = money market funds; NBFIs = non-bank financial institutions.

Source: FSB (2024); IMF, BIS. Data as of December 2024.

¹ Covers institutions operating in the United States with reporting requirements to the Securities and Exchange Commission.

² Gross notional exposure is the sum of the absolute value of long and short exposures, including via holdings of cash securities and through derivatives. US data include Treasuries and agency and government-sponsored entities bonds.

³ Leverage sources are divided into repos (largely financing for fixed income securities), prime brokerage (largely financing for equity securities) and other secured borrowing (which largely includes securities lending transactions).

Sources: Uland (2025); Office of Financial Research; BIS. Data as of December 2025

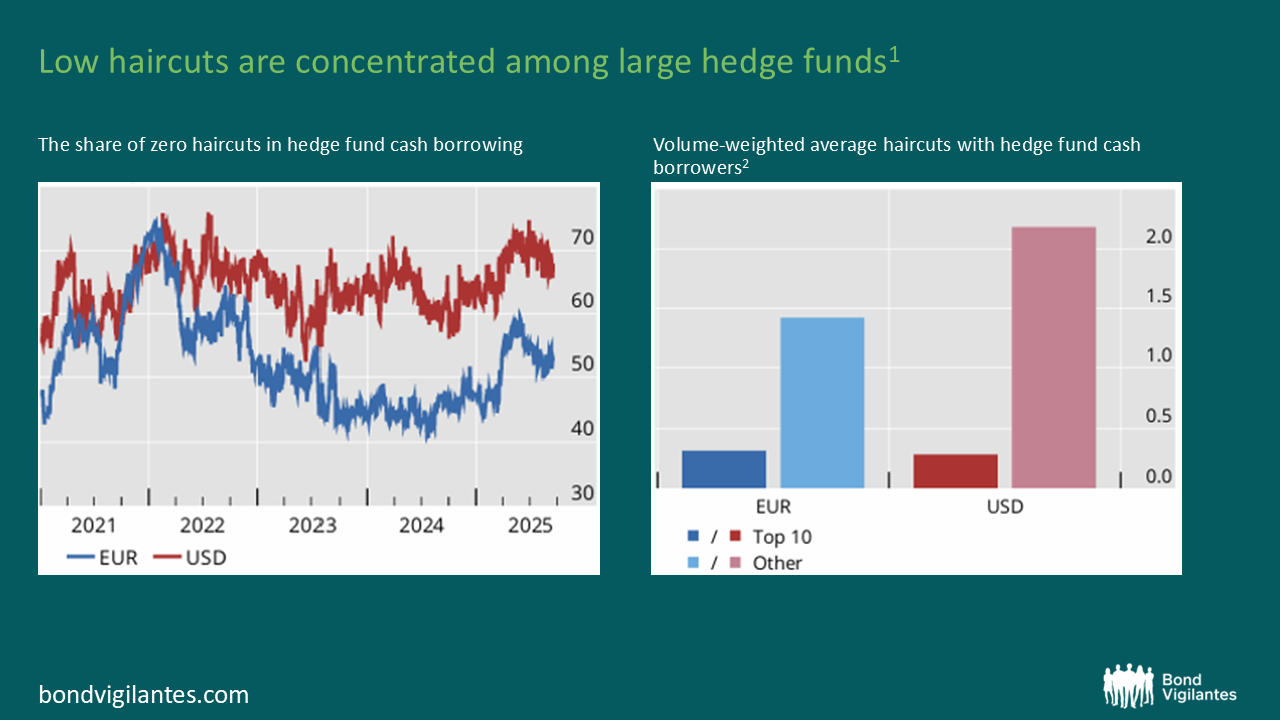

What’s more, not only are NBFIs the marginal buyer in core sovereign bond markets, an important subset of them, namely hedge funds, are heavily reliant on leverage via collateralised funding. According to the BIS, in recent years hedge funds, particularly larger ones, have been able to borrow in repo markets at exceptionally favourable terms. It estimates that approximately 70% of bilateral repos taken out by hedge funds in US dollars and 50% in bilateral repos in euros are offered at zero haircut – that is, without any discount, or haircut to protect the cash lender from market risk. In some cases bilateral haircuts can even be negative, as creditors have other assets and business with the hedge funds.5 The daily repo market in the US has doubled in the last two years alone and is now a staggering USD 13 trillion.

¹ Based on outstanding data. Bilateral transactions with investment funds as cash borrowers, with specific collateral, no net exposure and bilateral segment only.

² The top 10 hedge funds are identified as those with the highest average daily outstanding volumes over the same period in panel A.

Sources: Hermes et al (2025b); The Securities and Financing Transactions Data Store (SFTDS). Data as of December 2025.

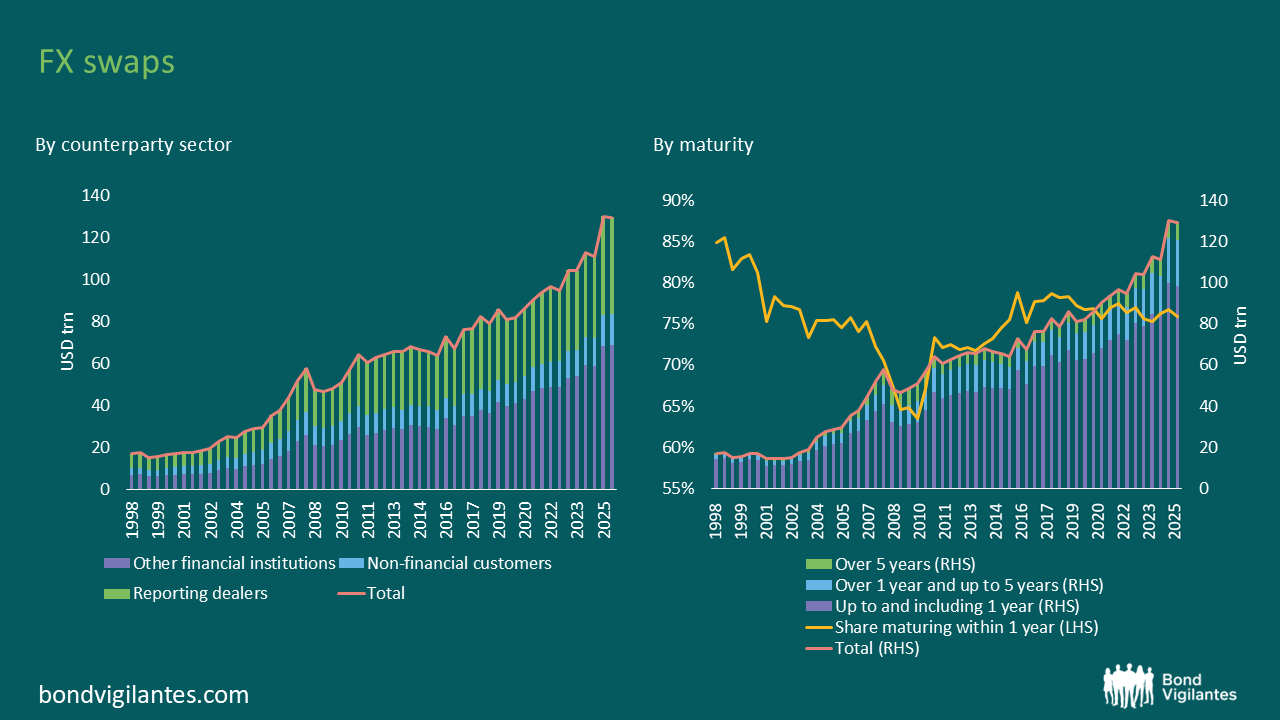

Furthermore, even when DM sovereign bonds are bought by the longer-term investors in the NBFI club (asset managers, pension funds and insurance companies) these entities, who are often based in major world regions/other DMs, hedge the FX risk of their portfolio holdings back into the currency of domicile, particularly via FX swaps. In doing so, they expose themselves to short-term USD funding risks. The BIS posits that, since about 75% of FX-swaps have maturities of less than a year, these investors are effectively transforming FX risk into maturity risk. The FX swaps market has tripled in size since the GFC to USD 130 trillion in June 2025.

¹ Including FX swaps, outright forwards and currency swaps; notional amounts outstanding.

² The share is calculated as a percentage of the data for which maturities are reported.

Source: BIS OTC derivatives statistics. Data as of December 2025.

Banks are not off the hook

Ironically, it is the regulated banking sector that is the key supplier of short-term USD funding in both the repo and the FX swap markets. Hence, it is also where the liquidity risk ultimately sits. FX swaps are off-balance sheet instruments that do not count towards banks’ total assets as per global accounting rules, but both repos and FX swaps are forms of collateralised lending and do count towards the banks’ own risk budget. As a result, stresses in one could quickly migrate to the other, exposing the holders of these FX derivatives to funding squeezes.

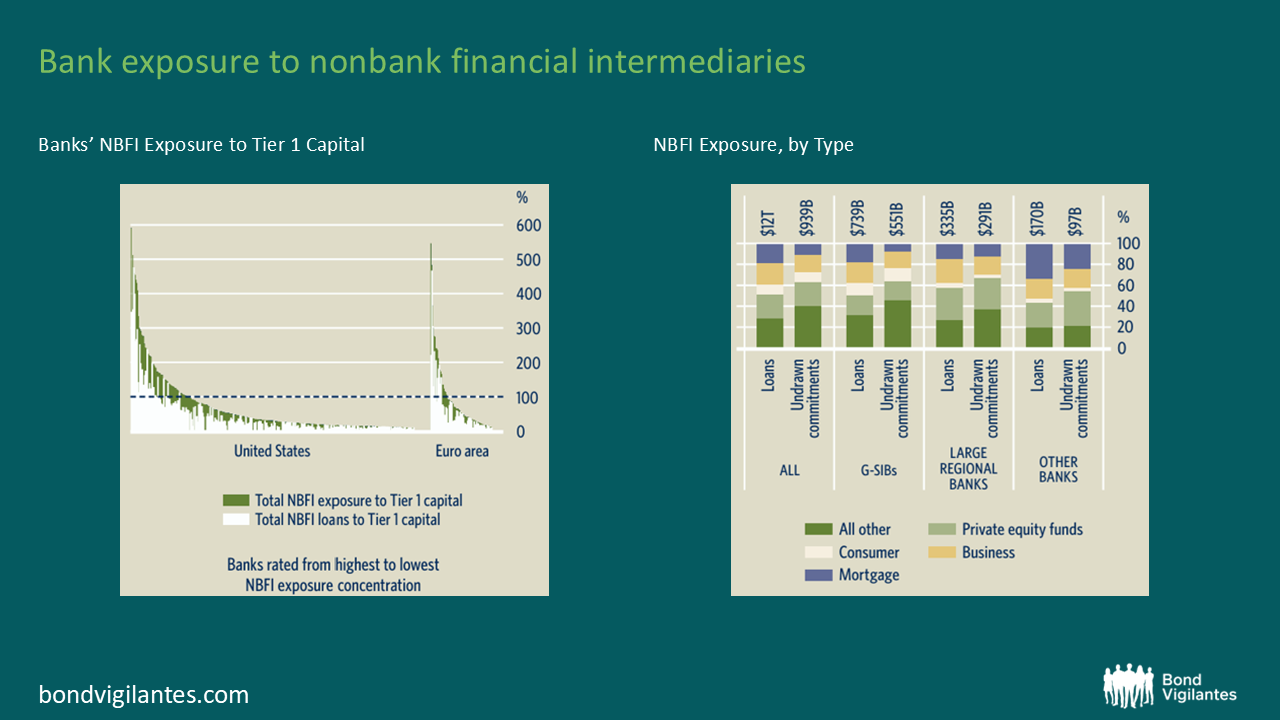

So while risk has ostensibly shifted out of the banking sector and into NBFI hands, in practical terms, the sovereign bank nexus has simply evolved to become a sovereign-bank-NBFI nexus. Indeed, the IMF notes that many US, and some euro area banks have on-balance-sheet exposure to NBFIs that far exceeds their capital. Off-balance sheet links are harder to document but, here too, exposure is high. In Europe and the US together, loans to all NBFIs at end-2024 were on average 9% of bank loan portfolios (USD 2.6 trillion). Total exposures were about USD 4.5 trillion (of which USD 1.9 trillion were undrawn commitments).

Source: IMF 2025, G-30, Data as of December 2025.

Will the real EM please stand up?

All this is to say that, while the global imbalances originate in the savings-investment behaviour of nations, and record amounts of government borrowing, the new financial architecture has the ability to amplify them manifold. The BIS goes so far as to say that risk appetite/perception may have eclipsed monetary policy in its ability to influence financial conditions. However, market-based finance ties financial conditions more closely to market prices of all kinds, which tend to be more volatile than bank lending rates. This potentially renders them more sensitive to a diverse range of shocks, including those originating abroad – a sobering thought at a time when there is an abundance of risks astir.

Simply put, developed market sovereign liabilities are increasingly held by investors that have more changeable funding structures and investment strategies that may be more vulnerable to abrupt repricing. Emerging markets have a long record of being subject to sudden reversals in market sentiment. Now, this is a risk developed markets must contend with too. Certainly the history of EM sovereign crises shows that the burden of adjustment is usually borne by deficit countries, when market discipline bares its teeth. This usually leads to rising borrowing costs, sudden stops in external financing, and, in extremis, default. While not a baseline expectation, it is also no longer inconceivable to think about such a scenario unfolding in core markets. In early May, Jeffrey Gundlach6 made the news for repositioning some of his funds in preparation for a potential restructuring of US debt.

The resilience of the USD’s safe-haven status may also be tested under certain scenarios. In previous episodes of stress, even ones originating in the US, investors flocked to US Treasuries which have thus far been universally accepted as the definition of a “risk-free” asset. This flight to safety allowed for an easing in US interest rates. Although the rest of the world is still long USD assets, this time around it might be different. This time around, there are question marks around the health of the US sovereign balance sheet, its ability to come to the rescue, and the US’s ability to right its own debt burden. In the event of a flight from the USD, markets will find themselves in uncharted territory.

How to tame your dragon

A metaphor doing the rounds at the BoE likens our inclination to look to markets as a gauge of economic health, to “being chained to the tail of a drunken dragon”. Whether the dragon that keels over with inebriation is the sovereign or the market, only time will tell. To be sure, both need a drink of water. Either way, caution is advised when the financial world is at the mercy of bond vigilantes.

______________________

1Brad Setser at the Council on Foreign Relations has long argued that China’s official data significantly understate the true size of its surpluses. He analyses Chinese customs data and other flows to build a fuller picture. China’s Massive Surplus is Everywhere (Yet The IMF Still Has Trouble Seeing It Clearly) | Council on Foreign Relations

2The current account is a flow metric. The International Investment Position (IIP) is a statistical statement that shows at a point in time the value of all financial assets of residents of an economy that are claims on non-residents; and the liabilities of residents of an economy to non-residents. Assets and liabilities include all financial instruments, i.e. debt and equity. The Net IIP is simply the difference between those assets and liabilities.

3The 8.5% correction in the USD since the start of 2025 notwithstanding, it is still historically robust. At current levels, the DXY Index is still slightly above its long-term average.

4NBFIs are a broad church and the Financial Stability Board defines them as all financial institutions other than central banks, banks, or public financial institutions. As such, they include collective investment vehicles (mutual funds, exchange-traded funds), long-term institutional investors such as pension funds, insurance corporations and sovereign wealth funds, as well as hedge funds and funds active in private credit and private equity. The G30 report helpfully categorises NBFIs in terms of 3 broad functions i.e. parallel, for those that offer activities distinct from banks; substitute, those that compete directly with banks; and transformation, those that provide new types of services in part by complementing bank-based services, but also by transforming them.

5To put this in context, a mere 5bp haircut results in leverage of 20x

6Jeffrey Gundlach, founder and CEO of Double-Line Capital, is an American billionaire investor and hedge fund manager widely known on Wall Street as the “Bond King”. He is famous for his bold, data-driven macroeconomic forecasts, including successfully predicting the 2007 housing market crash.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.